Home Warranty vs. Home Insurance: What are the Differences?

If you own a home or are planning to purchase one, understanding the difference between a homeowners appliance warranty and home insurance is essential. These two types of protection both help secure your investment and provide peace of mind for unexpected issues. Yet, they serve distinct purposes in covering different aspects of homeownership. A home warranty focuses on protecting essential appliances and systems, such as your HVAC, refrigerator, or plumbing. When these critical items break down due to normal wear and tear, a home warranty covers the repair or replacement, saving you the stress and cost of sudden repairs. In contrast, home insurance covers structural damage to your home caused by unforeseen events, like fires, storms, or theft. It’s designed to protect your entire property from natural disasters or unexpected incidents, ensuring your home and belongings are secure from major financial loss. Understanding these distinctions can help you decide if having both types of protection is necessary. While home insurance is often required by mortgage lenders, a homeowners appliance warranty is optional yet beneficial, providing coverage that home insurance typically doesn’t include. Ultimately, having both a homeowners appliance warranty and home insurance can offer a more comprehensive safety net, securing your finances and keeping your home comfortable and functioning smoothly year-round. What Is a Home Warranty? A home warranty is a service contract that helps pay for repairs and replacements of covered household appliances and home systems. In exchange for a monthly or annual fee, you get a flat rate on service calls. If an appliance or system covered by your plan breaks down, your home warranty company sends out a technician to diagnose and fix the problem—and you pay just the service call fee. Of course, these plans have coverage limits: A contract may cover up to, say, $1,500 per year for each eligible appliance, with an annual claim limit of $15,000. If you receive a home warranty as part of a real estate transaction, the coverage usually starts as soon as you close on the home. However, if you buy a warranty for a house you already own, you may have to wait 15 to 30 days before the coverage takes effect. What Does a Home Warranty Cover? Home warranties cover appliances and systems in both new and pre-owned homes. Most home warranty companies offer three types of plans: 1.Appliance Plans (e.g., washer/dryer, dishwasher, and refrigerator) 2.System Plans (e.g., HVAC, plumbing, and electrical systems) 3.Combination Plan (everything included in the appliance and system plans) Most companies let you add coverage (for an extra fee) for specific items that are excluded from the standard plans. Common “add-ons” include pools, spas, septic systems, wells, lawn sprinkler systems, and additional appliances (e.g., a second dishwasher or air conditioner). How Much Does a Home Warranty Cost? Home warranty costs are based on two fees: 1. A monthly or annual fee. This is what you pay to access the discounted service calls. Depending on where you live and the plan you buy, you might pay anywhere from $350 to more than $1,100 per year. 2. A service fee. This is the amount you pay each time you request repairs for a covered appliance or system. Most companies offer several service fee “levels,” which might range from about $55 to $150 per service call. In general, the lower the service fee, the higher your monthly or annual fee will be, and vice versa. What Is Homeowners Insurance? Home insurance (aka homeowners insurance) is a type of property insurance that protects against losses and damages caused by covered perils. According to the Insurance Information Institute (III), a standard homeowners insurance policy includes four essential types of coverage: 1. Coverage for the structure of the home: This pays to repair or rebuild the house if it’s damaged or destroyed by a covered peril. Most policies cover other structures on the property, too, such as garages, tool sheds, decks, and gazebos. 2. Coverage for personal belongings: This covers your furniture, clothes, sports equipment, and other personal belongings if they are stolen or destroyed by a covered peril. If you have expensive items, you may need a special personal property endorsement or a floater to ensure you’re adequately protected. 3. Liability protection: Liability coverage protects against lawsuits for injuries and property damage that policyholders, their family members, and their pets cause to other people. 4. Additional living expenses: This pays for hotels, meals, and other living expenses if your house is uninhabitable due to a covered peril. What Does Homeowners Insurance Cover? The most popular home insurance policy is the HO-3, which covers your home, belongings, and liability. According to the III, HO-3 policies provide broad coverage and protect against 16 disasters and perils: 1. Fire or lightning 2. Windstorm or hail 3. Explosion 4. Riot or civil commotion 5. Damage caused by aircraft 6. Damage caused by vehicles 7. Smoke 8. Vandalism or malicious mischief 9. Theft 10. Volcanic eruption 11. Falling object 12. Weight of ice, snow, or sleet 13. Accidental discharge or overflow of water or steam from a plumbing, heating air conditioning, or automatic fire-protective sprinkler system, or from a household appliance 14. Sudden and accidental tearing apart, cracking, burning, or bulging of a steam or hot water heating system, an air conditioner, or an automatic fire-protective system 15. Freezing of a plumbing, HVAC, or automatic fire-protective sprinkler system, or of a household appliance 16. Sudden and accidental damage from an artificially generated electrical current Homeowners insurance also covers your personal liability for injuries to other people (those who don’t live with you) and their property while they are on your property. The most common liability claims involve dog bites, home accidents, falling trees, intoxicated guests, and injured domestic workers. Standard home insurance policies don’t cover damage or losses caused by floods (whether natural or human-related) and earthquakes. Depending on where you live, it may be a good idea to add—or buy a separate policy for—flood or earthquake coverage. Ask your insurance agent

I Analyzed Land Value Across NSW—Here’s What Every Property Investor Should Know

I Analyzed Land Value Across NSW—Here’s What Every Property Investor Should Know Land value NSW has become the focal point for property investors seeking high returns and future stability. With a dynamic market in New South Wales, understanding what drives land value the difference between a smart investment and a missed opportunity can be. Every investor needs insights into these trends to capitalize on growth hotspots across the state. Location remains a powerful force behind land value in NSW. Coastal cities and rapidly growing suburbs have seen notable jumps in value, while lesser-known regions are now emerging as hidden gems. Identifying these areas early could unlock major gains, helping investors maximize their portfolio’s potential in ways that high-demand city centers might not. Infrastructure is another game-changer in land value NSW. Planned transport links, schools, and business districts have a profound impact on property prices, drawing new interest and driving up land values. By staying informed on these developments, you can position yourself for success, investing in areas poised for long-term growth. But there’s more to it—tax implications in NSW affect how profitable your investment truly is. With land tax obligations varying across property types and locations, knowing the tax landscape can prevent costly surprises. Savvy investors account for these factors, using tax insights to refine their strategies and retain more of their gains. I hope this sparks a new vision for you—imagine looking back, grateful you seized the opportunity in land value NSW today. What Factors Drive Land Value in New South Wales? Land value NSW is a powerful metric that can either elevate or hinder an investment’s potential. Understanding what influences this value is key for investors wanting to make impactful decisions. The landscape of land value in NSW isn’t static; it’s shaped by a dynamic set of factors that reveal which areas may become tomorrow’s high-growth hotspots. Location remains a critical driver of land value in NSW, with properties near thriving urban centers or scenic coastal towns often commanding higher prices. Proximity to amenities, job opportunities, and desirable lifestyles make these areas sought-after, pushing land values upward. For investors, location is often the starting point in assessing a property’s growth potential. But it’s not just location—government and infrastructure projects significantly boost land value NSW. New highways, transport links, and public amenities can transform a quiet suburb into a bustling investment hub almost overnight. As these developments progress, land values follow suit, making these areas ideal targets for early investors aiming to maximize returns. Imagine looking back years from now, realizing that spotting these factors early on was your secret advantage. Recognizing land value drivers is like having a roadmap to navigate the property market’s twists and turns. It’s not about chance; it’s about choosing strategically, backed by insights into growth trends and location dynamics. Economic health, including employment rates and local business growth, also plays a role in driving land value in NSW. Thriving regions attract both residents and investors, sparking competition and steadily increasing land prices. By following these factors, investors can position themselves for growth in areas with sustainable, long-term demand. How Rising Demand and Development Affect Land Prices In the vibrant world of property investment, understanding how rising demand influences land value NSW is crucial. As more people flock to urban centers and suburban areas alike, the competition for land intensifies, driving prices upward. This surge in demand isn’t just a fleeting trend; it’s a fundamental shift that shapes the landscape of real estate investment. Development plays an equally pivotal role in determining land value. New infrastructure projects, such as roads, schools, and public transportation, not only enhance accessibility but also increase the desirability of surrounding areas. As these developments unfold, land prices often soar, presenting golden opportunities for savvy investors who can spot these growth indicators early. The interplay between rising demand and development creates a ripple effect that can elevate land values significantly. Areas once considered remote can suddenly become hotspots for residential and commercial investment. As communities evolve and expand, those who recognize the signs of impending growth can secure their stake in future prosperity. Imagine being part of this transformative journey, where understanding the dynamics of land value can unlock lucrative investment opportunities. By staying attuned to local developments and market trends, investors position themselves at the forefront of this exciting landscape, ready to capitalize on the inevitable rise in land prices. As we witness the dance of demand and development in land value NSW, one thing becomes clear: the future of property investment is bright. Armed with the right knowledge and foresight, investors can navigate these changes with confidence, making informed decisions that pave the way for substantial returns in the ever-evolving real estate market. Tax Implications of NSW Land Ownership – Avoiding Common Pitfalls Owning land in New South Wales is an exciting venture, but it comes with its fair share of tax implications that every investor should understand. Navigating the complexities of land value NSW can be daunting, yet it’s crucial for maximizing your returns. Missteps in tax planning can lead to costly consequences, making knowledge of potential pitfalls essential for every property owner. One of the most significant traps is misunderstanding land tax assessments. Investors often underestimate how quickly land value can increase, leading to unexpected tax liabilities. Being aware of current rates and how they’re calculated helps you prepare and avoid nasty surprises come tax time. Ignorance is not bliss in the world of property taxes, especially in a rapidly changing market. Imagine the relief of having a solid grasp of the tax implications that come with your land ownership! By understanding these nuances, you can navigate the potential pitfalls with confidence and ensure your investment thrives without unnecessary financial setbacks. Knowledge truly is power when it comes to safeguarding your investment in land value. Another common pitfall arises from failing to account for capital gains tax when selling property. Many owners are unaware that a rise in land value upon sale can lead to

Is It the Right Time to Buy Property in 2024? Top Insights You Can’t Afford to Miss

Is It the Right Time to Buy Property in 2024? The Australian property market is evolving rapidly, and many potential buyers are wondering, “is it the right time to buy property?” With changing economic conditions, fluctuating interest rates, and the demand for housing still strong, making an informed decision is critical. Whether you are an experienced investor or a first-time homebuyer, understanding market trends will allow you to capitalize on the opportunities 2024 presents. This year, interest rates are one of the key factors impacting property prices, and knowing how to navigate them can mean the difference between a smart investment and a costly mistake. When considering is it the right time to buy property, potential buyers must also take a close look at current auction trends, housing supply, and government policies. In 2024, low housing inventory in key areas like Melbourne and Sydney is driving up competition at auctions, leading to price surges in certain suburbs. However, this doesn’t mean all areas are out of reach—by monitoring regions with less demand and capitalizing on long-term growth opportunities, you could still secure a fantastic investment property. Ultimately, the question of is it the right time to buy property comes down to your financial position, goals, and market knowledge. While some are holding off in hopes that property prices will cool, others are leveraging current interest rates to lock in favorable home loan terms. If you’re looking for long-term gains, focusing on emerging suburbs with solid growth potential may provide the best returns over time. So, understanding where and how to buy in 2024 will empower you to make confident and well-timed investment choices. Is It the Right Time to Buy Property in Australia? Factors You Need to Consider When asking, “is it right time to buy property?” in Australia, there are several key factors to evaluate before making any investment. The property market is influenced by numerous variables, such as interest rates, market demand, and economic stability. In 2024, rising interest rates and a competitive housing market have left many potential buyers wondering if it’s worth waiting for conditions to improve. However, the timing of your purchase depends on how well these factors align with your personal financial goals and the type of property you’re looking for. One important consideration is how is it right time to buy property based on regional performance. Cities like Melbourne and Sydney continue to experience strong demand, pushing property prices higher, while more affordable regions in other parts of Australia may present better investment opportunities. Additionally, government incentives for first-time homebuyers or property investors might make it an attractive time for certain demographics to enter the market, despite economic uncertainty. Another major factor influencing is it right time to buy property is the forecast for future market growth. While interest rates may be higher in the short term, some regions show long-term growth potential that could make buying now a lucrative decision. Understanding the local property market and staying informed about economic trends will help you make a confident decision. Whether you’re investing for rental income or long-term appreciation, evaluating these factors carefully can guide you toward making the right move in Australia’s dynamic property landscape. Interest Rates in Australia: How They Impact Your Property Purchase Decision Understanding interest rates Australia is crucial when deciding whether to purchase property in 2024. With the Reserve Bank of Australia (RBA) adjusting rates to combat inflation, higher interest rates can directly influence borrowing costs for home loans, which in turn affects property affordability. As interest rates rise, monthly mortgage repayments increase, making it more expensive to finance a property. This can discourage some buyers, but for savvy investors, it also presents opportunities to negotiate better deals or take advantage of lower property demand. In 2024, interest rates Australia are expected to continue fluctuating, with potential for further hikes depending on economic conditions. This uncertainty can create a sense of urgency for buyers who want to lock in lower rates before they rise further. However, it’s important to weigh the benefits of securing a property now against the potential for higher repayments over time. Fixed-rate loans may provide stability, while variable-rate loans could see increased costs if interest rates climb. The impact of interest rates Australia doesn’t just affect the immediate affordability of a property—it also influences long-term investment returns. Higher borrowing costs can eat into rental yields and reduce overall profitability for property investors. However, for those planning to hold onto properties for the long term, buying in a rising interest rate environment can still make sense, especially in areas poised for future growth. By staying informed about rate trends and adjusting your financial strategy accordingly, you can make a confident property purchase decision despite market volatility. Home Loan Interest Rates in 2024: What Buyers Need to Know In 2024, home loan interest rates are a critical factor for anyone looking to buy property in Australia. As interest rates continue to rise, they directly influence the cost of borrowing, making it more expensive to finance a home. With variable rates on the rise, buyers are faced with higher monthly repayments, potentially limiting their borrowing power. It’s essential to closely monitor how these home loan interest rates evolve throughout the year to make informed decisions about securing a loan. The key question for buyers is whether to lock in a fixed rate or opt for a variable one. Fixed home loan interest rates provide stability, allowing buyers to plan their finances without the risk of future rate hikes. However, variable rates, though initially lower in some cases, could become more expensive if the Reserve Bank of Australia increases rates again. Buyers need to weigh the pros and cons of both options based on their financial situation and risk tolerance. In addition to the rising cost of borrowing, home loan interest rates also affect long-term affordability and property values. Higher rates tend to cool demand in the property market, as fewer buyers can afford large mortgages, which can

NAB cuts fixed rates official interest rates decrease next year

NAB Cuts Fixed Rates as Official Interest Rates Set to Decrease Next Year Big four bank NAB has cut its fixed rates for customers by up to 0.65 percentage points, as lenders anticipate a cash rate cut next year. The bank has chopped its owner-occupier principal and fixed interest rates by up to 0.5 percentage points, and investor and owner-occupier interest-only fixed rates by up to 0.65 percentage points, according to rate tracking by Canstar. It follows Macquarie Bank’s move last week to slash a range of fixed rates by up to 0.4 percentage points to 5.39 per cent — and could be a sign more rate cuts are to come. Homeowners are anxiously awaiting the Reserve Bank of Australia (RBA) to drop interest rates from the 13-year high of 4.35 per cent. Central banks in the United States, Canada and New Zealand are among those that have reduced interest rates, but the RBA maintains Australia is in a different boat. The minutes from its September meeting confirmed there was no explicit discussion of the case to hike interest rates. Read our blog on: Interest Rates ANZ head of Australian economics Adam Boyton said the minutes represented a “clear step down in the RBA board’s hawkishness”. “This leaves the door open to a shift to neutral by the end of this year and then easing in early 2025,” he said. NAB’s owner-occupied loans have fallen between 0.55 and 0.1 percentage points. The most significant change was for the bank’s two-year fixed loan, which dropped from 6.59 per cent to 6.04 per cent. The bank’s lowest three-year fixed rate of 5.89 per cent is now in line with Commonwealth Bank and Westpac, while ANZ’s offers above 6 per cent. More than 37 lenders have dropped at least one fixed rate over the last month, according to Canstar research. Australian Bureau of Statistics lending data shows just two per cent of new and refinanced loans in August opted for a fixed rate. Read Full Article at: 7 News Australia

Fixed rates drop amidst predictions

Fixed rates drop amidst predictions Variable and fixed home loan rates saw both increases and cuts this week, with fixed rates outperforming variable, and a potential cash rate cut anticipated by February, Canstar reported. Home loan rate changes Aussie Home Loans raised interest rates on two variable owner-occupier and investor loans by 0.05%, while five other lenders reduced rates across 50 variable loans for both owner-occupiers and investors. Meanwhile, twelve lenders slashed fixed rates on 322 loans, with an average decrease of 0.24%. Fixed rates outperform variable options Abal Banking continues to offer the lowest variable rate at 5.75%, although a surge in rate cuts means that 112 fixed rates now sit below this, a significant increase from last week’s 64. “There was yet another downpour of fixed rate cuts this week,” said Sally Tindall (pictured above), Canstar’s data insights director. Major institutions like Bendigo Bank and Teachers Mutual Group are among those offering reduced rates. Read Full Article here at: Broker News

Werribee

Get to own a House and Land Package in Werribee for only $646,030! The advantages of residing in Werribee include several positive aspects, such as the abundance of parks and recreation facilities available. Werribee boasts several parks, including the Werribee River Park and the Werribee Open Range Zoo, which offer ample opportunities for families to enjoy the great outdoors. Land Size: 263 sqm House Size: 168.89 sqm 4 Bedrooms 1 Living Room 2 Bathrooms 2 Car for Garage Land Settlement: February 2025 𝗪𝗵𝘆 𝗖𝗵𝗼𝗼𝘀𝗲 Werribee Safe and Family-Orientated Community Reasonable and Affordable Housing Prices Surrounded by a Broad Range of Educational Institutions Walking Distance to Shopping Centres and Train Stations Numbers of Major Attractions to Visit Easy and Full Accessible to All Amenities Client’s review: “great place”Werribee South is very peaceful. Not alot of people live here, it’s away from the traffic and chaos of the world. You can’t beat this place for peace and quiet. It is so close to the city and should have a different name as it is so different to Werribee, its not funny. The only thing missing is shops which the marina will bring. The marina will also bring more people to this great place which is not a good thing but the marina won’t be that big as to spoil the “serenity” as one great man once said. We also provide a rental guarantee with a minimum of 1 year and a maximum of 3 years. 𝗙𝗼𝗿 𝗺𝗼𝗿𝗲 𝗱𝗲𝘁𝗮𝗶𝗹𝘀, 𝗷𝘂𝘀𝘁 𝗰𝗮𝗹𝗹 𝘂𝘀: 1300 074 675 or send us a message on Whatsapp +61 488 859 637 For more updates, follow us on social media:Facebook: Simply WealthInstagram: @simplywealthgroupWebsite: simplywealthgroup.com.auTwitter: @SimplyWealthGrp

Truganina

Get to own a House and Land Package in Truganina for only $656,744! Welcome to Truganina, a charming suburb that beautifully balances convenience with tranquility. Located in the heart of Melbourne’s expanding west, Truganina offers a serene escape from the city’s hustle and bustle, while still providing easy access to urban amenities. With its welcoming community, lush green spaces, and well-planned infrastructure, it’s an ideal place for those seeking a peaceful retreat without compromising on modern conveniences. Land Size: 281 sqm House Size: 157.25 sqm 4 Bedrooms 1 Living Room 2 Bathrooms 2 Car for Garage Land Settlement: Titled 𝗪𝗵𝘆 𝗖𝗵𝗼𝗼𝘀𝗲 Truganina Safe and Family-Orientated Community Reasonable and Affordable Housing Prices Surrounded by a Broad Range of Educational Institutions Walking Distance to Shopping Centres and Train Stations Numbers of Major Attractions to Visit Easy and Full Accessible to All Amenities We also provide a rental guarantee with a minimum of 1 year and a maximum of 3 years. 𝗙𝗼𝗿 𝗺𝗼𝗿𝗲 𝗱𝗲𝘁𝗮𝗶𝗹𝘀, 𝗷𝘂𝘀𝘁 𝗰𝗮𝗹𝗹 𝘂𝘀: 1300 074 675 or send us a message on Whatsapp +61 488 859 637 For more updates, follow us on social media:Facebook: Simply WealthInstagram: @simplywealthgroupWebsite: simplywealthgroup.com.auTwitter: @SimplyWealthGrp

Wyndham Vale

Get to own a House and Land Package in Wyndham Vale for only $646,161! Wyndham Vale is a rapidly growing suburb located in the southwestern part of Melbourne, Victoria. Known for its family-friendly atmosphere and abundant green spaces, it offers residents a tranquil lifestyle with easy access to urban amenities. The suburb features modern housing developments, excellent schools, and convenient transport links, making it an attractive destination for young families and professionals. With its blend of suburban comfort and proximity to the city, Wyndham Vale continues to thrive as a vibrant and welcoming community. Land Size: 263 sqm House Size: 157.25 sqm 4 Bedrooms 1 Living Room 2 Bathrooms 2 Car for Garage Land Settlement: Titled 𝗪𝗵𝘆 𝗖𝗵𝗼𝗼𝘀𝗲 Wyndham Vale Safe and Family-Orientated Community Reasonable and Affordable Housing Prices Surrounded by a Broad Range of Educational Institutions Walking Distance to Shopping Centres and Train Stations Numbers of Major Attractions to Visit Easy and Full Accessible to All Amenities We also provide a rental guarantee with a minimum of 1 year and a maximum of 3 years. 𝗙𝗼𝗿 𝗺𝗼𝗿𝗲 𝗱𝗲𝘁𝗮𝗶𝗹𝘀, 𝗷𝘂𝘀𝘁 𝗰𝗮𝗹𝗹 𝘂𝘀: 1300 074 675 or send us a message on Whatsapp +61 488 859 637 For more updates, follow us on social media:Facebook: Simply WealthInstagram: @simplywealthgroupWebsite: simplywealthgroup.com.auTwitter: @SimplyWealthGrp

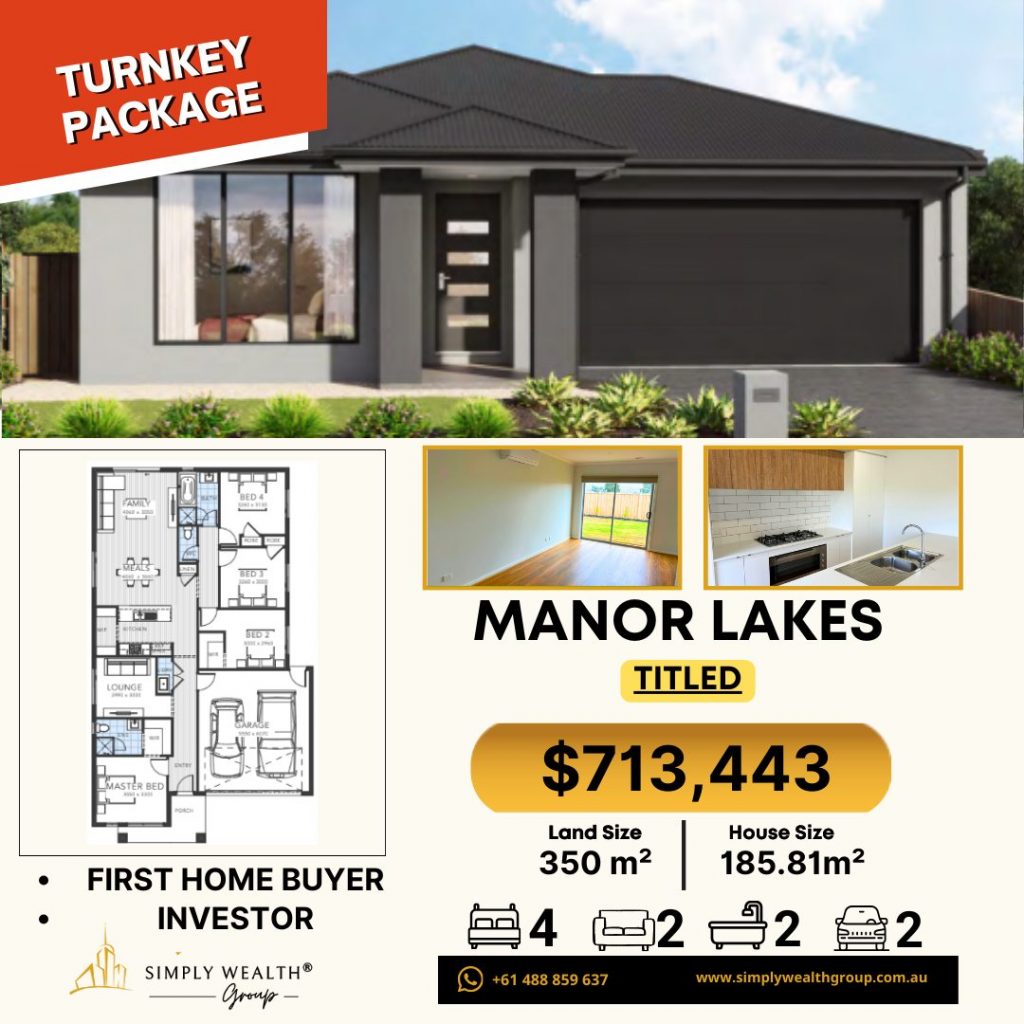

Manor Lakes

Get to own a House and Land Package in Manor Lakes for only $713,443! Manor Lakes, a charming suburb in Melbourne’s west, perfectly blends modern living with natural beauty. Famous for its expansive lakes and lush parks, this community provides a serene environment for residents. The suburb features well-maintained walking trails, scenic picnic spots, and family-friendly recreational areas, making it a paradise for nature enthusiasts. With its thoughtful urban planning, Manor Lakes seamlessly integrates contemporary amenities with the tranquility of its natural surroundings, offering a peaceful and attractive lifestyle. Land Size: 350 sqm House Size: 185.81 sqm 4 Bedrooms 2 Living Room 2 Bathrooms 2 Car for Garage Land Settlement: Titled 𝗪𝗵𝘆 𝗖𝗵𝗼𝗼𝘀𝗲 Manor Lakes Safe and Family-Orientated Community Reasonable and Affordable Housing Prices Surrounded by a Broad Range of Educational Institutions Walking Distance to Shopping Centres and Train Stations Numbers of Major Attractions to Visit Easy and Full Accessible to All Amenities We also provide a rental guarantee with a minimum of 1 year and a maximum of 3 years. 𝗙𝗼𝗿 𝗺𝗼𝗿𝗲 𝗱𝗲𝘁𝗮𝗶𝗹𝘀, 𝗷𝘂𝘀𝘁 𝗰𝗮𝗹𝗹 𝘂𝘀: 1300 074 675 or send us a message on Whatsapp +61 488 859 637 For more updates, follow us on social media:Facebook: Simply WealthInstagram: @simplywealthgroupWebsite: simplywealthgroup.com.auTwitter: @SimplyWealthGrp

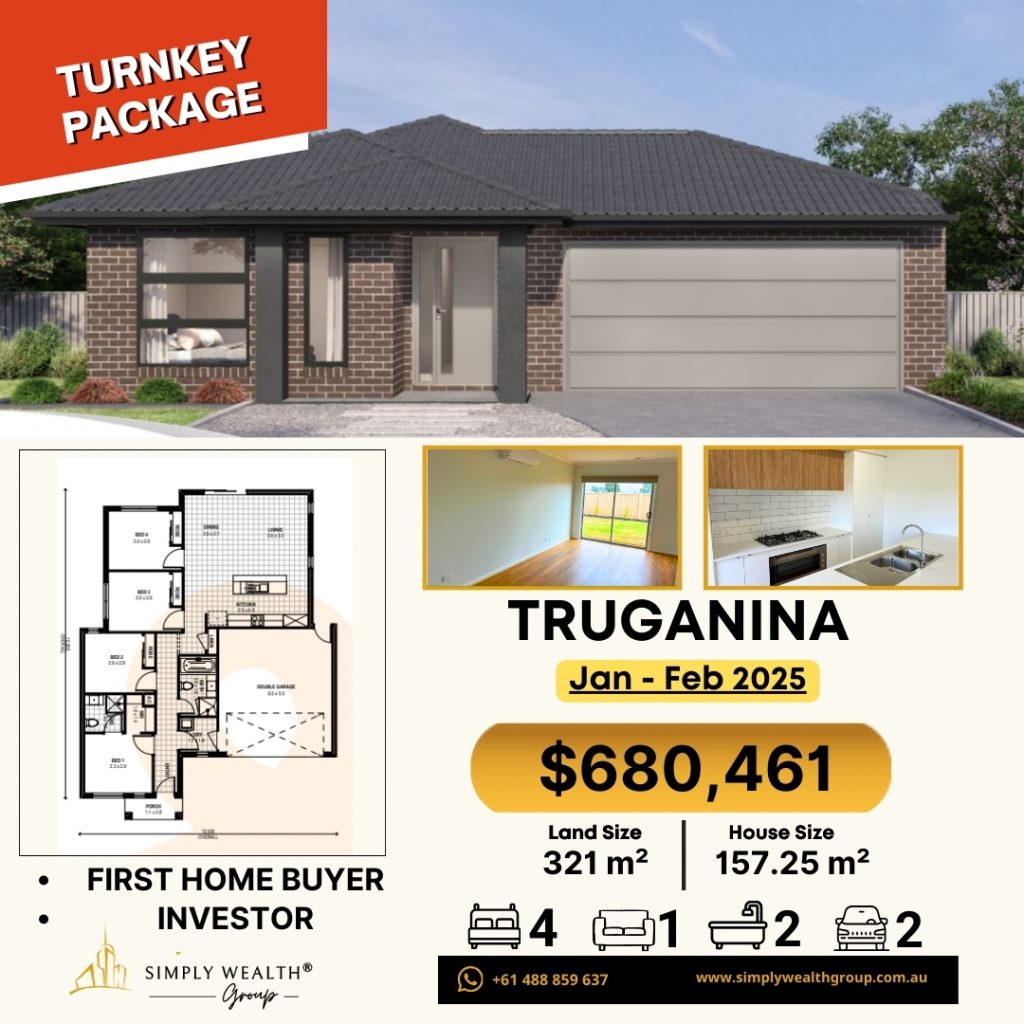

Truganina

Get to own a House and Land Package in Truganina for only $680,461! Nestled in the heart of Melbourne’s western suburbs, Truganina offers a serene and picturesque escape from the hustle and bustle of city life. With its lush green parks, tranquil walking trails, and welcoming community, Truganina is a hidden gem that combines modern living with natural beauty. Discover the peace and charm that make this suburb an ideal place to call home. Land Size: 321sqm House Size: 157.25sqm 4 Bedrooms 1 Living Room 2 Bathrooms 2 Car for Garage Land Settlement: Jan-Feb 2025 𝗪𝗵𝘆 𝗖𝗵𝗼𝗼𝘀𝗲 Truganina Safe and Family-Orientated Community Reasonable and Affordable Housing Prices Surrounded by a Broad Range of Educational Institutions Walking Distance to Shopping Centres and Train Stations Numbers of Major Attractions to Visit Easy and Full Accessible to All Amenities We also provide a rental guarantee with a minimum of 1 year and a maximum of 3 years. 𝗙𝗼𝗿 𝗺𝗼𝗿𝗲 𝗱𝗲𝘁𝗮𝗶𝗹𝘀, 𝗷𝘂𝘀𝘁 𝗰𝗮𝗹𝗹 𝘂𝘀: 1300 074 675 or send us a message on Whatsapp +61 488 859 637 For more updates, follow us on social media:Facebook: Simply WealthInstagram: @simplywealthgroupWebsite: simplywealthgroup.com.auTwitter: @SimplyWealthGrp