Sydney’s Secret First-Home Hack: Just Inherit a Gold Mine (Or Marry Rich)

In Sydney, where the median house price surpassed $1.5 million in 2024 (CoreLogic), nearly half of first-home buyers rely on financial support from their parents—colloquially dubbed the “bank of mum and dad.” This informal institution has become Australia’s ninth-largest lender, with contributions exceeding $35 billion annually, according to Digital Finance Analytics. For those without such familial backing, the path to homeownership narrows considerably. A 2021 report by the National Housing Finance and Investment Corporation revealed that in Sydney, only 25% of properties were accessible to the top 20% of earners, leaving the majority priced out entirely.

Dr. Nicola Powell, Chief of Research at Domain, notes that “intergenerational wealth is no longer a luxury—it’s a prerequisite.” This dynamic has entrenched inequality, as younger Australians without inherited capital face insurmountable barriers. With housing supply constrained and demand bolstered by record migration, Sydney’s property market increasingly rewards those born into privilege, sidelining traditional notions of merit.

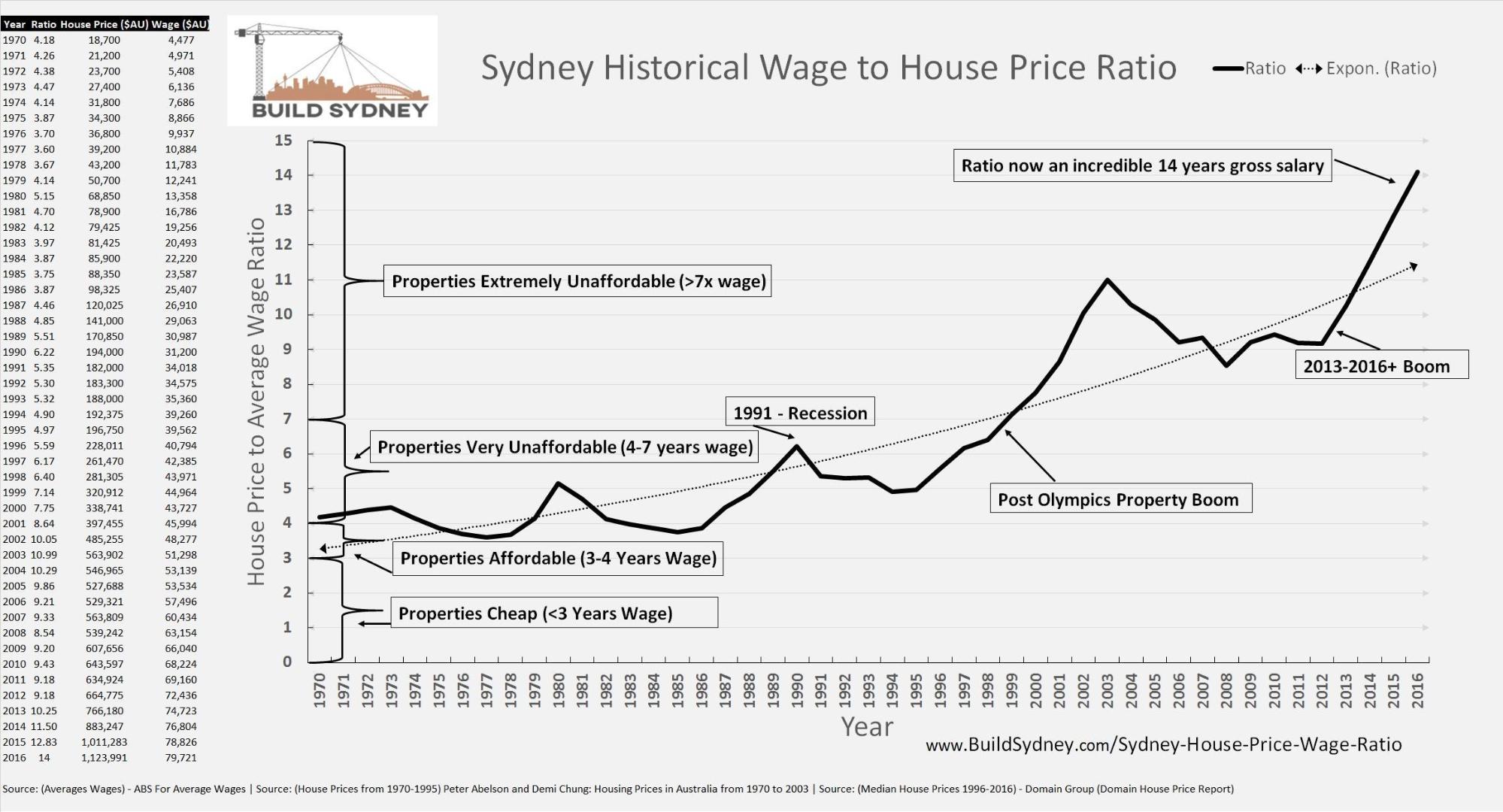

Image source: buildsydney.com

Current Property Prices and Trends

Sydney’s property market is increasingly defined by the interplay of constrained supply and surging demand, with nuanced factors shaping its trajectory. One critical yet underexplored dynamic is the role of infrastructure projects in driving localized price surges. For instance, the Sydney Metro expansion has significantly elevated property values in suburbs like Castle Hill and Cherrybrook, where accessibility improvements have transformed these areas into high-demand zones. This phenomenon underscores how infrastructure investments can amplify disparities between well-connected and peripheral suburbs.

A comparative analysis reveals that while rezoning initiatives in Melbourne have similarly boosted property values, Sydney’s market exhibits a sharper response due to its chronic housing undersupply. This disparity highlights the importance of contextual factors, such as population density and migration trends, in determining the effectiveness of such interventions.

However, these developments are not without limitations. Properties in newly connected areas often experience speculative price inflation, which can outpace genuine demand. This creates challenges for first-home buyers, who may find themselves priced out despite increased housing stock.

“Infrastructure projects are a double-edged sword—they enhance connectivity but can exacerbate affordability issues if not paired with broader housing policies.”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

The implications are clear: while infrastructure can unlock value, its benefits must be balanced with equitable housing strategies to ensure inclusivity.

Historical Context of Housing Affordability

In the late 20th century, Sydney’s housing market operated under markedly different dynamics, where affordability was bolstered by policies promoting expansive development. During this period, local councils frequently relaxed zoning restrictions, enabling a steady supply of new housing. This approach, combined with lower price-to-income ratios, allowed first-home buyers to enter the market with relative ease. However, the landscape began to shift dramatically in the early 2000s, as urban densification policies and stricter planning regulations curtailed new developments.

A critical factor in this transformation was the introduction of more stringent mortgage lending standards, which, while aimed at reducing financial risk, inadvertently raised barriers for younger buyers. Comparative data from the 1980s and 2010s highlights a stark contrast: the average deposit required for a first home increased from approximately 20% of annual income to over 100%, reflecting the compounding effects of stagnant wage growth and escalating property prices.

“The interplay of restrictive zoning and rising demand has entrenched inequality, making homeownership a distant dream for many,” explains Professor Judy Yates, a leading housing economist.

This historical trajectory underscores how policy decisions, once seen as prudent, have contributed to today’s affordability crisis, revealing the long-term consequences of prioritizing market stability over accessibility.

The Role of Intergenerational Wealth

Intergenerational wealth operates as a pivotal force in Sydney’s housing market, not merely as a financial advantage but as a structural determinant of access. Research from the Australian Housing and Urban Research Institute (AHURI) reveals that recipients of parental transfers are twice as likely to transition into homeownership compared to their peers without such support. This disparity underscores how familial wealth functions as a de facto gatekeeper, bypassing traditional credit constraints that have tightened since the early 2000s.

The mechanics of these transfers extend beyond simple cash gifts. Bequests and inter vivos transfers—financial contributions made during a parent’s lifetime—often enable recipients to secure larger deposits, reducing their loan-to-value ratios and granting access to more favorable mortgage terms. For instance, a 2017 AHURI study found that first-home buyers receiving intergenerational assistance paid, on average, 20% more for properties than those without such support, reflecting their enhanced purchasing power.

This dynamic exacerbates wealth inequality. As economist Thomas Piketty notes, inherited wealth increasingly dictates economic outcomes in low-growth environments. In Sydney, this trend manifests in a bifurcated market: one where intergenerational aid accelerates wealth accumulation for some, while others face prolonged renting cycles, unable to compete. The implications are profound, entrenching socio-economic divides and challenging the notion of housing as a universally attainable asset.

Image source: linkedin.com

Mechanisms of Wealth Transfer

One critical yet underexplored mechanism of wealth transfer in Sydney’s housing market is the strategic use of inter vivos contributions to optimize financial outcomes for both parents and recipients. Unlike lump-sum gifts, these transfers are often structured incrementally, allowing parents to provide ongoing support without triggering significant tax liabilities. This approach not only facilitates the accumulation of deposits but also enables younger buyers to secure more favorable loan-to-value ratios, effectively reducing borrowing costs over time.

A comparative analysis reveals that while outright bequests offer immediate purchasing power, incremental transfers provide greater flexibility in navigating market fluctuations. For instance, parents may adjust contributions based on property price trends or interest rate changes, ensuring their support aligns with optimal market conditions. However, this strategy is not without limitations; smaller, phased transfers may delay homeownership timelines, particularly in rapidly appreciating suburbs.

“Incremental financial support acts as a dynamic tool, adapting to market conditions while minimizing tax exposure,”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

The nuanced timing and structuring of these transfers highlight their dual role: they not only alleviate liquidity constraints but also serve as a strategic instrument for wealth preservation. This underscores the broader implications of intergenerational support in perpetuating economic divides.

Impact on First-Time Buyers

The ability of intergenerational wealth to accelerate first-time homeownership hinges on its capacity to mitigate credit constraints, a critical barrier in Sydney’s high-cost market. By enabling larger deposits, inter vivos transfers and bequests reduce loan-to-value ratios, granting recipients access to more favorable mortgage terms. This financial leverage not only expedites market entry but also positions beneficiaries to compete effectively in a landscape dominated by rising property values.

A comparative analysis reveals that recipients of intergenerational transfers often purchase higher-value properties than their self-funded peers, as evidenced by AHURI’s findings that such buyers allocate significantly larger sums to down payments. However, this advantage is not uniformly distributed. Families with limited wealth may provide smaller, phased contributions, which, while helpful, often fail to match the pace of property price inflation, delaying homeownership.

Contextual factors further complicate this dynamic. For instance, the timing of transfers relative to market cycles can amplify or diminish their impact. Transfers during periods of rapid price growth may merely offset rising costs, whereas those aligned with market corrections can yield substantial purchasing power.

“Intergenerational transfers are not just financial tools; they are mechanisms that reshape access and opportunity in housing markets,”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

This nuanced interplay underscores the dual role of such wealth: alleviating immediate financial barriers while perpetuating systemic inequities.

Financial Strategies for First-Time Buyers

Navigating Sydney’s property market requires first-time buyers to adopt multifaceted financial strategies that extend beyond traditional savings. A 2024 Helia Insurance study revealed that 15% of first-home buyers utilized family assistance, often through co-ownership agreements, to bridge affordability gaps. However, innovative approaches like rentvesting—purchasing in affordable regions while renting closer to work—are gaining traction. This strategy not only builds equity but also mitigates lifestyle compromises.

Economic policy uncertainty, as highlighted by Griffith University, amplifies price volatility, deterring buyers during unstable periods. To counter this, leveraging fixed-price contracts and pairing grants like the HomeBuilder Grant with the First Home Owner Grant can stabilize costs. Additionally, data-driven tools identifying emerging growth areas, such as Perth, offer opportunities for strategic investments.

These methods underscore the importance of adaptability. By combining traditional savings with innovative tactics, buyers can navigate Sydney’s high-cost market while positioning themselves for long-term financial resilience.

Image source: resources.homeownershipmatters.realtor

Traditional vs. Alternative Financing Options

In Sydney’s volatile housing market, traditional financing methods, such as fixed-rate mortgages, often lack the adaptability required to address fluctuating property prices and rising living costs. Alternative financing options, particularly co-ownership agreements and rentvesting, offer a more dynamic approach by aligning financial strategies with market realities.

Co-ownership, for instance, allows multiple buyers to pool resources, reducing individual financial burdens while increasing purchasing power. This model is particularly effective in high-demand suburbs, where single-income buyers are often priced out. However, it requires robust legal frameworks to manage shared responsibilities and potential disputes. A 2024 Helia Insurance study revealed that 15% of first-home buyers in Sydney utilized co-ownership, with many citing it as a critical enabler of market entry.

Rentvesting, on the other hand, decouples lifestyle from investment by enabling buyers to purchase properties in affordable areas while renting in preferred locations. This strategy not only builds equity but also leverages tax benefits like negative gearing. However, it demands meticulous planning to identify properties with strong growth potential and manage additional costs, such as maintenance and property management fees.

“Alternative financing models like co-ownership and rentvesting redefine accessibility, offering tailored solutions to navigate Sydney’s high-cost market.”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

These approaches highlight the importance of flexibility and strategic planning in overcoming the limitations of traditional financing.

Case Studies of Successful Home Purchases

A notable example of strategic first-home purchasing in Sydney involves a young professional who leveraged a phased inter vivos transfer from her parents. By receiving incremental contributions over three years, she was able to consistently adjust her deposit savings to align with market fluctuations. This approach not only reduced her loan-to-value ratio but also positioned her to secure a property in a rapidly appreciating suburb without overextending financially. The flexibility of phased transfers proved critical in mitigating the risks associated with sudden market shifts.

In another case, a group of siblings utilized a co-ownership model to enter Sydney’s competitive housing market. By pooling resources and combining their borrowing capacities, they acquired a multi-unit property in a growth corridor. This arrangement allowed them to share both equity and ongoing costs, while also benefiting from tax advantages tied to investment properties. The success of this model hinged on a robust legal agreement that clearly defined ownership stakes and responsibilities.

“Innovative financing strategies like phased transfers and co-ownership are reshaping access to Sydney’s housing market,”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

These cases highlight how tailored financial strategies, underpinned by intergenerational support, can overcome systemic barriers to homeownership.

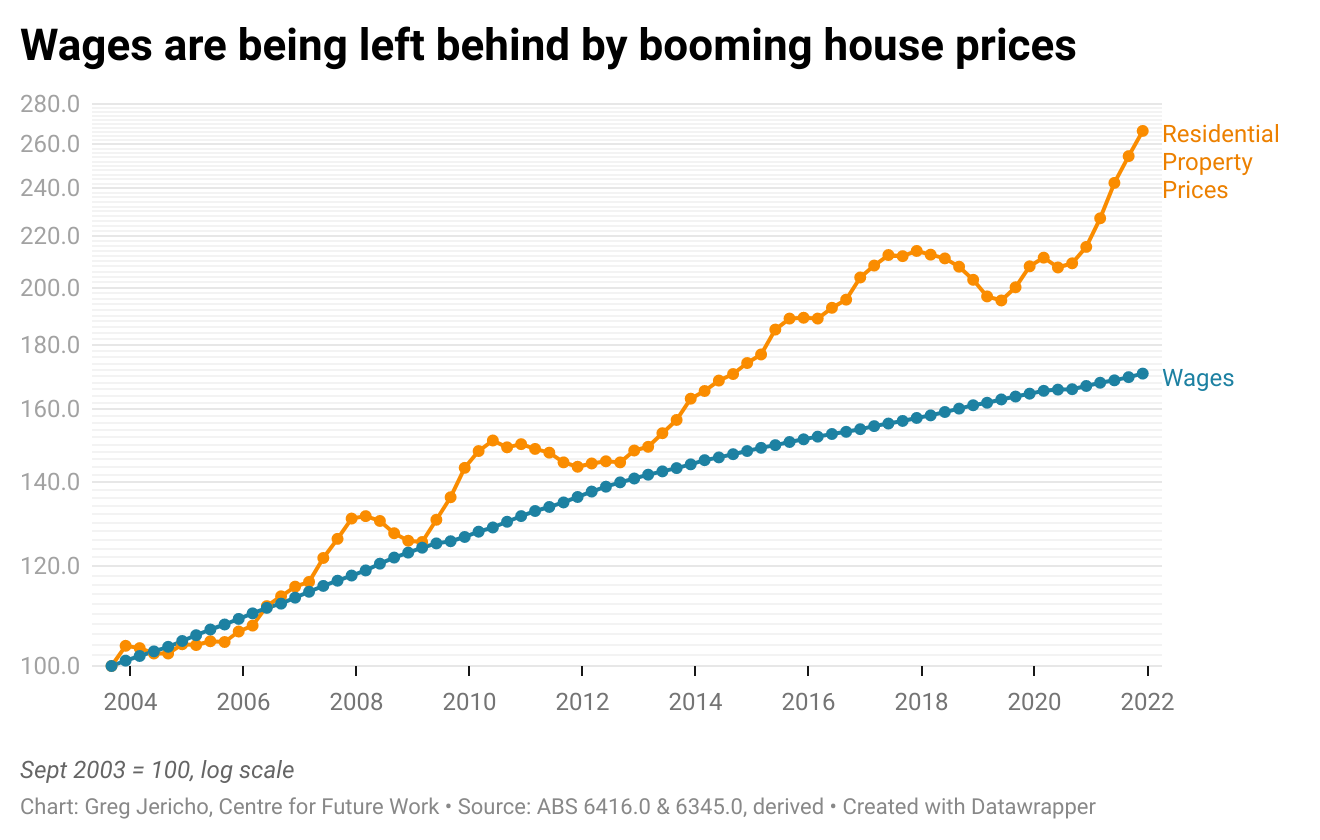

Socioeconomic Implications of Wealth Inequality

Wealth inequality in Sydney’s housing market extends beyond financial disparity, embedding structural barriers that perpetuate social stratification. According to the 2021-22 NSW Intergenerational Report, the median wealth of homeowners in 2018 was $1.4 million, compared to just $78,000 for non-homeowners. This stark gap illustrates how homeownership functions as a primary vehicle for wealth accumulation, disproportionately benefiting those with inherited capital.

Intergenerational transfers exacerbate this divide by accelerating property acquisition for wealthier families, as highlighted by AHURI’s findings that recipients of such transfers are twice as likely to become homeowners. This dynamic creates a feedback loop: rising property values inflate parental equity, enabling larger transfers, while renters face escalating costs without comparable wealth-building opportunities.

The implications are profound. Housing inequality not only limits social mobility but also distorts broader economic stability, as wealth becomes increasingly concentrated among property owners.

Image source: futurework.org.au

Long-Term Effects on Social Mobility

In Sydney’s housing market, intergenerational wealth transfers have entrenched a structural advantage that significantly impacts long-term social mobility. The mechanism is clear: inherited capital not only facilitates immediate homeownership but also accelerates wealth accumulation through compounding property value appreciation. This dynamic creates a self-reinforcing cycle where those without access to such transfers face systemic barriers to upward mobility.

A critical factor is the timing and scale of these transfers. Research from the Australian Housing and Urban Research Institute (AHURI) highlights that recipients of intergenerational wealth are twice as likely to secure homeownership, often earlier in life. This early entry allows them to benefit from extended periods of equity growth, while their peers without such support remain renters, unable to build comparable wealth. The disparity is further exacerbated by Sydney’s high property appreciation rates, which disproportionately reward those already in the market.

However, this advantage is not uniform. Families with limited wealth may provide smaller, phased contributions, which often fail to keep pace with rising property prices. This creates a nuanced hierarchy even among those receiving support, with wealthier families perpetuating greater advantages.

“Inherited wealth in housing markets like Sydney’s doesn’t just transfer assets—it transfers opportunity,”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

Addressing these disparities requires policies that go beyond affordability, targeting the structural inequities that perpetuate generational privilege.

Policy Debates and Potential Solutions

A critical yet underexplored policy lever in addressing wealth inequality in Sydney’s housing market is the implementation of a progressive inheritance tax specifically targeting intergenerational property transfers. This approach directly addresses the disproportionate advantage conferred by inherited wealth, which accelerates homeownership for some while sidelining others. By taxing property transfers based on their value and timing, such a system could redistribute opportunities without undermining market stability.

The effectiveness of this measure hinges on its design. Comparative studies from OECD nations reveal that inheritance taxes with exemptions for primary residences and phased rates based on asset value minimize economic distortions while promoting equity. However, Australia’s current tax framework, which heavily favors property ownership through capital gains tax exemptions, creates significant resistance to such reforms.

Contextual factors, such as Sydney’s chronic housing undersupply and speculative investment culture, further complicate implementation. Without complementary policies—such as subsidies for affordable housing developments or incentives for first-time buyers—inheritance taxes alone may fail to bridge the gap.

“Inheritance taxation, when paired with targeted housing policies, can recalibrate market dynamics to prioritize accessibility over privilege,”

— Dr. Nicola Powell, Chief of Research and Economics, Domain

This nuanced approach underscores the need for integrated solutions that balance fiscal equity with practical market considerations.

FAQ

What role does intergenerational wealth play in Sydney’s housing market for first-home buyers?

Intergenerational wealth significantly shapes Sydney’s housing market by acting as a gateway for first-home buyers to overcome financial barriers. Parental contributions, often termed the “Bank of Mum and Dad,” provide critical support through bequests or inter vivos transfers, enabling larger deposits and access to favorable mortgage terms. This dynamic amplifies wealth inequality, as those without familial assistance face prolonged renting cycles. Research highlights that recipients of such transfers are twice as likely to secure homeownership, underscoring the structural advantage of inherited capital. This trend entrenches socio-economic divides, making property ownership increasingly dependent on generational privilege rather than individual financial merit.

How does the ‘Bank of Mum and Dad’ compare to traditional mortgage lenders in Sydney?

The ‘Bank of Mum and Dad’ surpasses traditional mortgage lenders in flexibility and accessibility for Sydney’s first-home buyers. Unlike banks, parental contributions often come with no interest, lenient repayment terms, or as outright gifts, reducing financial strain. This informal institution, now among Australia’s top lenders, provides over $34 billion annually, bridging gaps left by stringent lending criteria. However, it deepens wealth inequality, as only families with substantial assets can offer such support. Traditional lenders, constrained by regulatory frameworks, cannot match this personalized assistance, making the ‘Bank of Mum and Dad’ a pivotal yet exclusive force in Sydney’s property market.

What are the socioeconomic implications of relying on inheritance or family wealth for homeownership in Sydney?

Relying on inheritance or family wealth for homeownership in Sydney entrenches socio-economic divides, creating a bifurcated market of property owners and perpetual renters. Wealthy families leverage intergenerational transfers to secure homeownership, accelerating wealth accumulation through rising property values. Conversely, those without such support face prolonged renting cycles, unable to compete in a high-cost market. This dynamic perpetuates inequality, as housing wealth becomes a primary vehicle for intergenerational privilege. Over time, this reliance distorts social mobility, concentrating economic power among property-owning families while sidelining others, challenging the notion of equitable access to Sydney’s housing market.

Are there alternative strategies for first-home buyers in Sydney who lack access to family financial support?

First-home buyers in Sydney without family financial support can explore innovative strategies like rentvesting, where they purchase affordable properties in regional areas while renting closer to work. Co-ownership agreements with friends or partners also pool resources to increase purchasing power. Leveraging government schemes, such as the First Home Owner Grant or stamp duty concessions, can reduce upfront costs. Fixed-price contracts mitigate cost overruns, while shared equity models lower entry barriers by splitting ownership with institutions. These approaches, combined with meticulous financial planning and data-driven tools to identify growth areas, offer viable pathways to navigate Sydney’s high-cost housing market independently.

How do government policies influence the growing reliance on inherited wealth in Sydney’s property market?

Government policies in Sydney’s property market, such as capital gains tax exemptions on primary residences and the absence of inheritance taxes, incentivize wealth accumulation through property ownership. These frameworks disproportionately benefit existing homeowners, enabling larger intergenerational transfers. Meanwhile, demand-side measures like first-home buyer grants often inflate property prices, further sidelining those without inherited wealth. The lack of robust supply-side interventions exacerbates housing scarcity, driving up costs and deepening reliance on familial support. This policy environment perpetuates systemic inequality, as inherited wealth increasingly dictates access to homeownership, entrenching socio-economic divides and limiting opportunities for upward mobility in Sydney’s housing market.