RBA’s Rate Cut: Impact on Homebuyers and Housing Market Dynamics

On February 4, 2025, the Reserve Bank of Australia (RBA) reduced the cash rate by 25 basis points to 4.10%, marking its first rate cut in over four years. For many, this move signaled relief—lower mortgage repayments, increased borrowing capacity, and a potential lifeline for first-time buyers. Yet, within days, auction clearance rates in Sydney and Melbourne surged past 74%, and property listings began to attract unprecedented competition.

This paradox lies at the heart of Australia’s housing market dynamics: while rate cuts make borrowing cheaper, they also fuel demand, driving up prices faster than incomes can keep pace. In Brisbane, where median house prices have already climbed steadily, buyers now face the dual challenge of affordability and heightened competition.

The RBA’s decision, intended to stimulate economic activity, has instead exposed the fragile balance between monetary policy and housing accessibility, leaving many Australians questioning whether relief is truly within reach.

Image source: sbs.com.au

Understanding the Role of the RBA in Monetary Policy

The Reserve Bank of Australia (RBA) plays a pivotal role in shaping monetary policy, particularly through its influence on interest rates. The recent rate cut to 4.10% highlights the dual-edged nature of such interventions. While the reduction aims to stimulate economic activity, its impact on housing affordability reveals deeper systemic challenges.

A critical aspect is the interplay between monetary policy and housing demand. For instance, the rate cut has spurred increased borrowing capacity, as evidenced by auction clearance rates in Sydney and Melbourne surpassing 74%. However, this surge in demand has outpaced income growth, exacerbating affordability issues. In Brisbane, where median house prices have steadily risen, first-time buyers face intensified competition, underscoring the unintended consequences of rate adjustments.

Real-world implications are evident in the behavior of property developers like Stockland, which reported heightened interest in new housing projects post-rate cut. Yet, this demand surge risks inflating prices further, creating a feedback loop detrimental to long-term affordability.

To address these challenges, the RBA could adopt scenario analyses integrating fiscal policy as a complementary tool. By aligning monetary and fiscal strategies, policymakers can mitigate housing market volatility while ensuring broader economic stability.

The Paradox of Rate Cuts and Housing Affordability

The RBA’s rate cut to 4.10% has amplified a paradox: while lower rates reduce borrowing costs, they simultaneously intensify housing demand, driving prices higher and eroding affordability. This dynamic is particularly evident in Sydney and Melbourne, where auction clearance rates surged past 74% following the cut, reflecting heightened buyer competition.

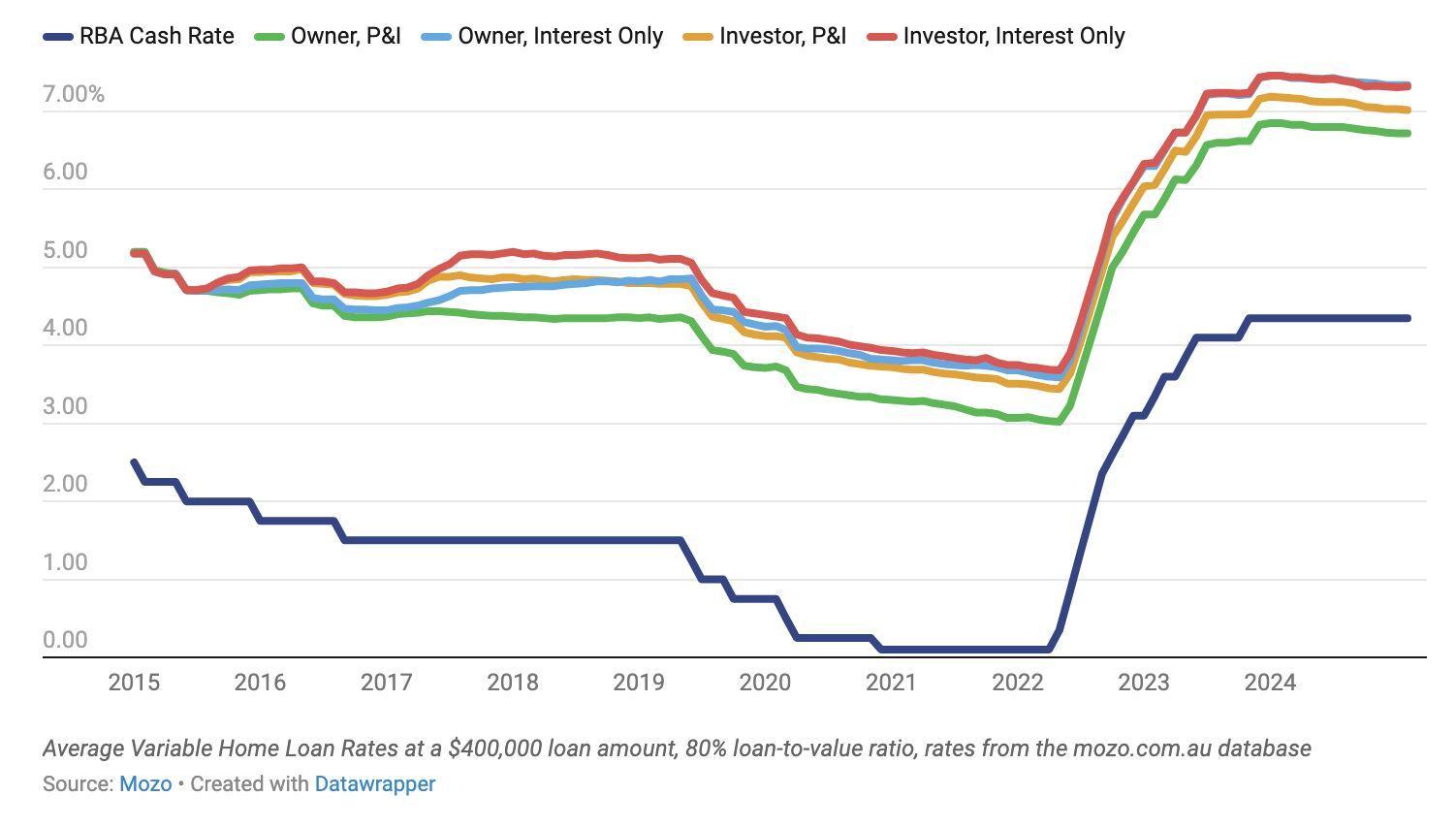

A key driver of this paradox is the feedback loop between borrowing capacity and market psychology. For example, the big four banks—ANZ, CommBank, NAB, and Westpac—swiftly adjusted mortgage rates, with reductions ranging from 5.84% to 6.19% by early March 2025. This increased the average borrowing capacity by approximately $13,000, enabling more buyers to enter the market. However, as demand outpaces supply, price growth negates these gains, particularly in high-demand areas like Brisbane.

Historical data underscores this trend. During the 2019 rate cut cycle, similar demand surges led to a 7.2% annual increase in national property prices. Current conditions mirror this trajectory, exacerbated by supply-side constraints such as labor shortages and rising construction costs.

To mitigate this paradox, policymakers could explore targeted fiscal measures, such as subsidies for new developments or incentives for affordable housing projects. Aligning monetary policy with supply-side interventions may stabilize prices while preserving accessibility for first-time buyers.

Mechanics of Rate Cuts and Borrowing Capacity

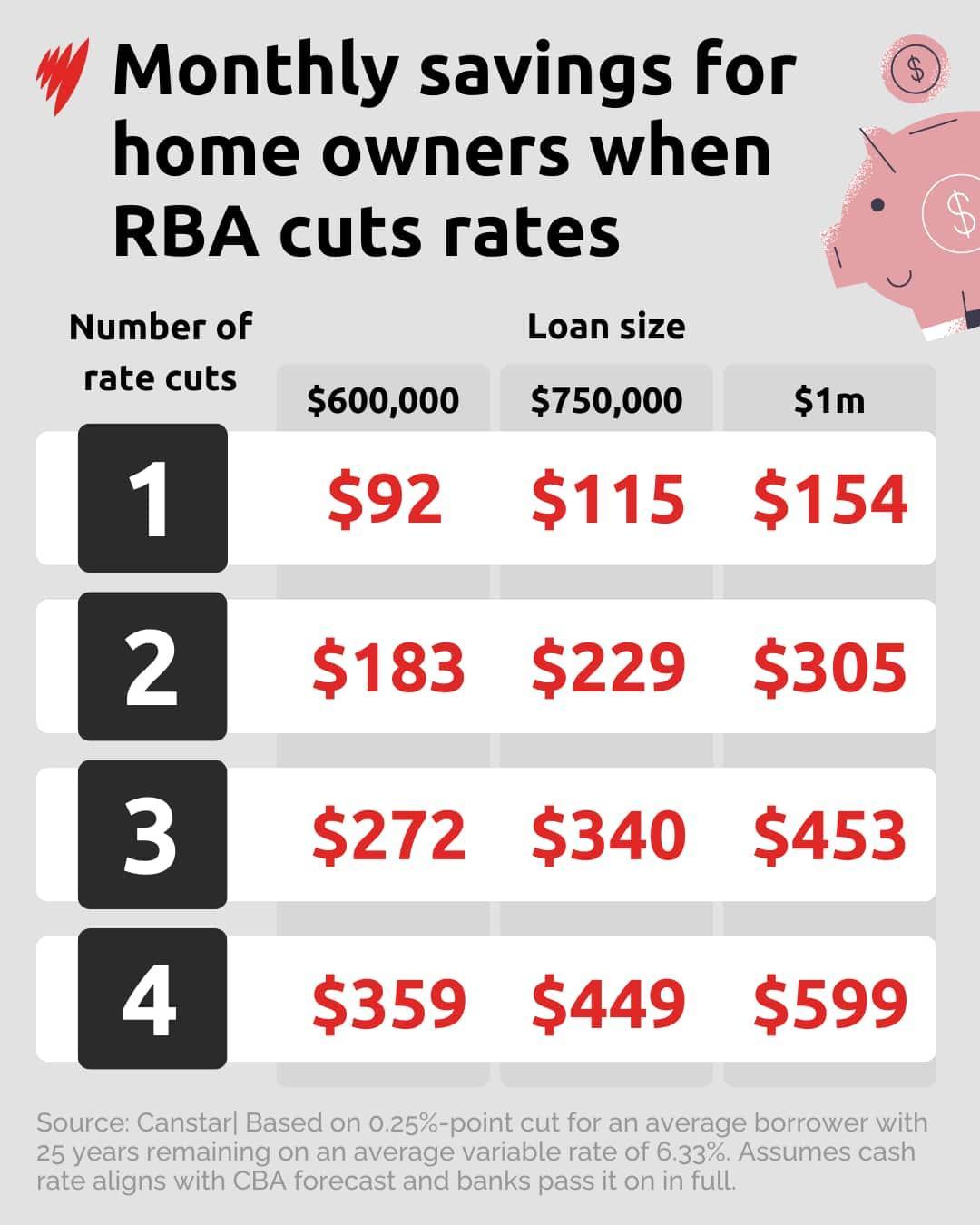

Rate cuts directly influence borrowing capacity by reducing interest rates, which lowers monthly repayment obligations and increases the amount lenders are willing to approve. Following the RBA’s February 2025 rate cut to 4.10%, major banks, including ANZ and Westpac, adjusted their serviceability buffers, enabling borrowers to qualify for loans up to 2-3% higher than before. For instance, a household previously approved for a $600,000 loan could now access an additional $12,000 to $18,000, depending on the lender.

This mechanism, however, creates a ripple effect. While increased borrowing capacity empowers buyers, it also intensifies competition, particularly in high-demand markets like Sydney and Brisbane. This demand surge often outpaces supply, driving property prices higher and negating affordability gains.

A common misconception is that rate cuts uniformly benefit all buyers. In reality, first-home buyers face disproportionate challenges as investor activity resurges. Experts like Sally Tindall of Canstar emphasize the importance of proactive financial planning, such as reducing personal debt, to maximize borrowing potential.

Policymakers must address supply-side constraints, such as labor shortages, to ensure rate cuts translate into sustainable affordability rather than fueling speculative price growth.

Image source: linkedin.com

How Rate Cuts Increase Borrowing Power

Rate cuts enhance borrowing power by reducing interest rates, which directly lowers monthly repayment obligations and increases the maximum loan amount lenders are willing to approve. For example, after the RBA’s February 2025 rate cut to 4.10%, major banks like NAB and Westpac adjusted their serviceability buffers, allowing borrowers to qualify for loans up to 3% higher. This translates to an additional $15,000 to $20,000 in borrowing capacity for a typical $700,000 loan.

However, this increase is not uniform across all demographics. Investors, buoyed by lower rates, often outcompete first-home buyers, particularly in high-demand markets like Sydney. Historical data from the 2019 rate cut cycle revealed a 7.2% annual rise in property prices, driven by similar borrowing power dynamics. This trend is now resurfacing, with CoreLogic reporting a 0.3% national home value increase in February 2025, despite affordability challenges.

A lesser-known factor is the role of lender-specific policies. Some institutions, such as ANZ, have eased income verification requirements, enabling borrowers with variable income streams to access higher loans. Yet, this leniency may tighten as competition intensifies, underscoring the importance of financial planning.

Looking ahead, aligning rate cuts with targeted fiscal policies—such as subsidies for affordable housing—could mitigate speculative price growth while preserving accessibility for first-time buyers. This dual approach ensures borrowing power translates into sustainable market stability.

Impact on Housing Demand and Property Prices

The RBA’s February 2025 rate cut to 4.10% has intensified housing demand, particularly in metropolitan areas like Sydney and Melbourne, where auction clearance rates surged past 74%. This demand spike is driven by increased borrowing capacity and heightened buyer confidence, creating a competitive market environment. For instance, Stockland, a leading property developer, reported a 15% rise in inquiries for new housing projects within weeks of the rate cut, underscoring the immediate impact on buyer activity.

A critical factor amplifying price growth is the supply-demand imbalance. With new housing construction 20% below pre-pandemic levels and population growth projected to add 1 million migrants over three years, supply constraints are exacerbating price pressures. Historical parallels, such as the 2019 rate cut cycle, reveal a 7.2% annual property price increase under similar conditions, suggesting a repeat trajectory.

Emerging trends highlight the role of investor activity. Lower rates have reignited interest from investors, who often outbid first-home buyers. This dynamic is evident in Brisbane, where median house prices have risen steadily, further straining affordability.

To counteract speculative price growth, policymakers could implement targeted measures, such as incentivizing affordable housing developments or introducing stricter investor lending criteria. These strategies, combined with rate cuts, could stabilize demand while ensuring long-term market accessibility for diverse buyer segments.

Effects on Different Buyer Segments

The RBA’s rate cut to 4.10% has created distinct outcomes for various buyer segments, revealing both opportunities and challenges. First-home buyers, for instance, benefit from increased borrowing capacity, with banks like NAB and Westpac adjusting serviceability buffers to allow loans up to 3% higher. However, this advantage is often offset by heightened competition from investors, who leverage lower rates to outbid them in high-demand markets like Sydney and Brisbane.

Investors, buoyed by reduced borrowing costs, are re-entering the market aggressively. CoreLogic data shows a 0.3% national home value increase in February 2025, driven partly by investor activity. This resurgence has reignited concerns about affordability, as speculative buying inflates prices faster than income growth.

Unexpectedly, downsizers are also impacted. While lower rates improve liquidity for buyers of their properties, rising prices in lifestyle markets like the Gold Coast complicate their ability to secure affordable replacements.

“The rate cut is a double-edged sword—while it boosts confidence, it exacerbates affordability challenges,” notes Eleanor Creagh, Senior Economist at REA Group.

Policymakers must address these disparities by aligning monetary policy with targeted fiscal measures, such as subsidies for affordable housing, to ensure equitable market access.

Image source: azurafinancial.com.au

Challenges for First-Time Homebuyers

First-time homebuyers face a unique set of challenges exacerbated by the RBA’s rate cut to 4.10%. While increased borrowing capacity offers a theoretical advantage, the reality is far more complex. Investor activity, reignited by lower rates, has intensified competition in high-demand markets like Sydney and Brisbane. CoreLogic data from February 2025 reveals a 0.3% national home value increase, with investor-driven demand outpacing supply, leaving first-time buyers struggling to secure properties.

A critical barrier is the supply-side constraint. With new housing construction 20% below pre-pandemic levels, limited inventory disproportionately impacts entry-level buyers. For example, Stockland reported a 15% rise in inquiries for new developments post-rate cut, yet delays in approvals and labor shortages have restricted actual availability.

Additionally, psychological factors play a role. The fear of missing out (FOMO) often drives first-time buyers to overextend financially, exacerbating long-term affordability issues. Historical parallels from the 2019 rate cut cycle show similar patterns, where heightened competition negated the benefits of increased borrowing power.

To address these challenges, policymakers could implement targeted subsidies for first-home buyers or incentivize developers to prioritize affordable housing. Aligning fiscal measures with monetary policy would ensure that rate cuts translate into sustainable opportunities rather than fleeting advantages.

Investor Influence on Market Dynamics

The RBA’s rate cut to 4.10% has reignited investor activity, significantly shaping market dynamics. Investors, leveraging reduced borrowing costs, are re-entering high-demand markets like Sydney and Brisbane, often outbidding first-home buyers. CoreLogic data from February 2025 highlights a 0.3% national home value increase, with investor-driven demand amplifying price pressures.

A notable case is Stockland, which reported a 15% surge in inquiries for new housing projects post-rate cut. However, this investor interest has created a feedback loop: heightened demand inflates property values, further sidelining first-home buyers. Historical parallels from the 2019 rate cut cycle revealed a 7.2% annual property price increase, driven largely by speculative investor activity.

Emerging trends also show investors capitalizing on tight rental markets. With vacancy rates at historic lows and rents rising, investors are prioritizing properties with strong cash flow potential. This strategy, while profitable, exacerbates affordability challenges for renters and buyers alike.

To mitigate these effects, policymakers could introduce stricter investor lending criteria or implement targeted taxes on speculative purchases. Additionally, incentivizing affordable housing developments could balance investor-driven demand with broader market accessibility. These measures would ensure sustainable growth while preserving opportunities for diverse buyer segments.

Broader Economic Implications and Market Trends

The RBA’s rate cut to 4.10% has far-reaching economic implications, intertwining housing market trends with broader financial dynamics. While lower rates stimulate borrowing and consumer spending, they risk reigniting inflation if demand outpaces supply. For instance, government bond yields fell by 20 basis points since mid-January 2025, reflecting market expectations of further easing, yet this could pressure the Australian dollar, which recently strengthened to 0.6341 against the U.S. dollar.

A critical misconception is that rate cuts uniformly benefit all sectors. In reality, supply-side constraints, such as labor shortages and rising construction costs, limit housing availability, intensifying price pressures. Historical parallels from the 2019 rate cut cycle revealed similar inflationary risks, with property prices rising 7.2% annually.

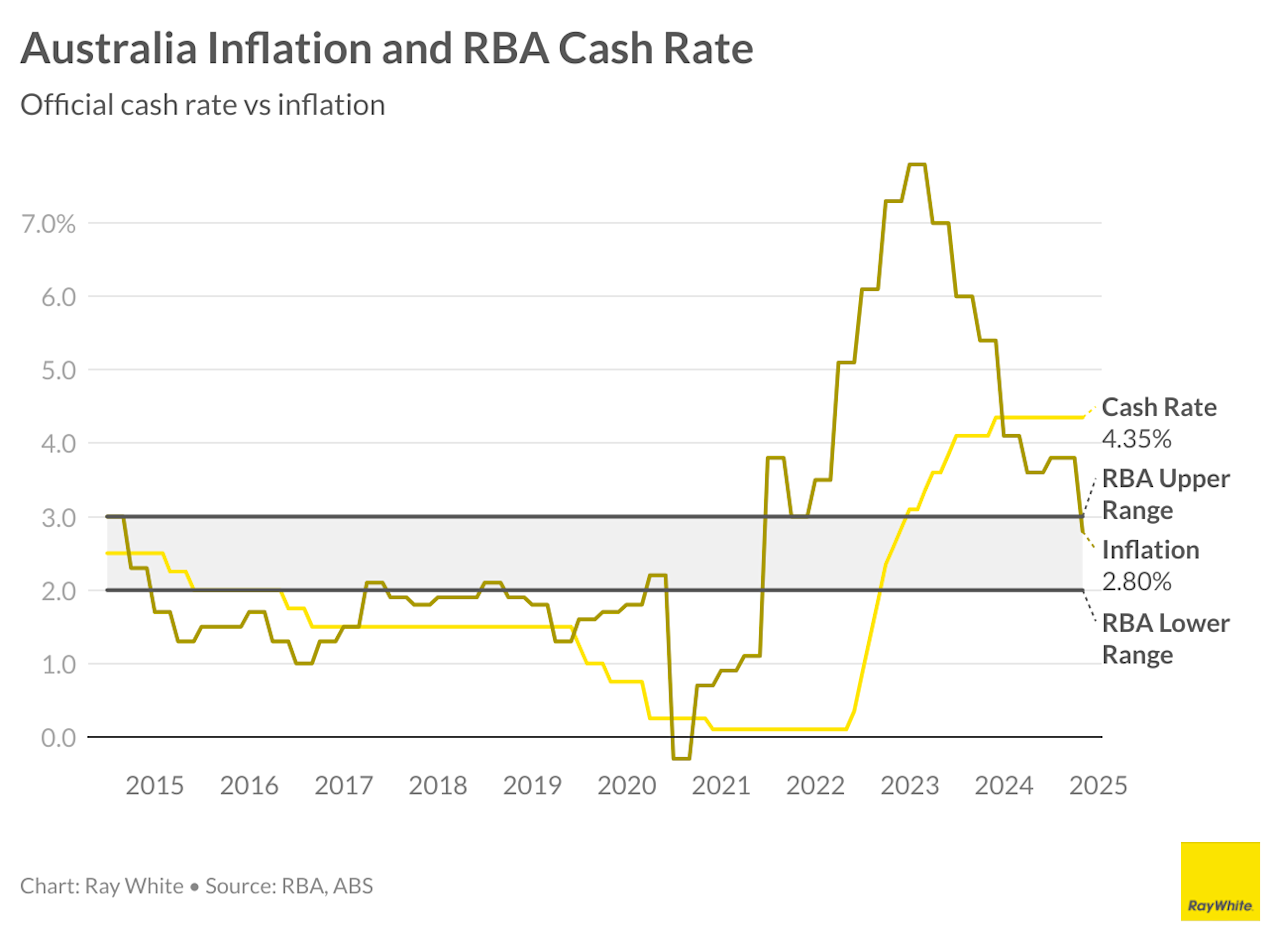

“Sustainably returning inflation to target remains the RBA’s highest priority,” emphasized Governor Michele Bullock, underscoring the delicate balance between growth and stability.

Policymakers must align monetary easing with fiscal measures, such as subsidies for affordable housing, to mitigate speculative growth while fostering equitable market access. This dual approach ensures long-term economic resilience amidst shifting market dynamics.

Image source: au.finance.yahoo.com

Historical Context and Current Market Conditions

The RBA’s February 2025 rate cut to 4.10% mirrors patterns observed during the 2019 easing cycle, where reduced borrowing costs spurred a 7.2% annual rise in property prices. However, today’s market introduces unique complexities, including supply-side constraints and shifting demographic pressures. For instance, new housing construction remains 20% below pre-pandemic levels, while Australia’s population is projected to grow by 1 million migrants over three years, intensifying demand.

A notable case study is Stockland, which reported a 15% surge in inquiries for new housing projects following the rate cut. Yet, labor shortages and elevated construction costs have delayed project completions, limiting the immediate impact on supply. This bottleneck underscores the interplay between monetary policy and structural inefficiencies.

Emerging trends also highlight the role of investor activity. CoreLogic data from February 2025 shows a 0.3% national home value increase, driven by speculative purchases in high-demand markets like Sydney. Investors, buoyed by tight rental markets and rising yields, are outpacing first-home buyers, exacerbating affordability challenges.

To navigate these dynamics, policymakers could adopt scenario analyses integrating fiscal incentives for affordable housing and stricter investor lending criteria. Aligning monetary policy with targeted interventions ensures sustainable growth while mitigating speculative risks. This approach balances short-term market stimulation with long-term economic stability.

Future Projections and Emerging Trends

The trajectory of Australia’s housing market post-RBA rate cut suggests a nuanced interplay of demand, supply, and policy interventions. Analysts anticipate further rate cuts in 2025, potentially lowering the cash rate to 3.60%, as projected by Capital Economics. This easing cycle could amplify borrowing capacity, but its impact will hinge on mitigating supply-side constraints.

A critical emerging trend is the shift in market psychology. As rates decline, the transition from “Fear of Buying Early” (FOBE) to “Fear of Missing Out” (FOMO) is accelerating buyer activity. For instance, Stockland has already reported a 15% rise in inquiries for new housing projects, yet construction bottlenecks persist due to labor shortages and material costs. This imbalance risks inflating prices further, particularly in high-demand urban centers like Sydney and Melbourne.

To address these challenges, policymakers could implement a Housing Affordability Index (HAI), integrating metrics such as borrowing capacity, construction timelines, and population growth. This index would provide real-time insights into market accessibility, guiding fiscal measures like subsidies for affordable housing or tax incentives for developers.

“Sustainably returning inflation to target remains the RBA’s highest priority,” noted Governor Michele Bullock, emphasizing the need for balanced growth.

Looking ahead, aligning monetary policy with targeted fiscal strategies—such as incentivizing regional developments—could stabilize demand while fostering equitable market access, ensuring long-term economic resilience.

FAQ

How does the RBA’s rate cut influence borrowing capacity for homebuyers in 2025?

The RBA’s rate cut to 4.10% directly enhances borrowing capacity by reducing interest rates, which lowers monthly repayment obligations and increases the maximum loan amount lenders approve. Major banks, including NAB and Westpac, adjusted serviceability buffers, enabling borrowers to qualify for loans up to 3% higher. For instance, a $700,000 loan could now allow an additional $15,000 to $20,000 in borrowing power. However, this increase is tempered by supply-side constraints, such as labor shortages and rising construction costs, which drive property prices higher. Aligning fiscal policies with monetary easing is essential to ensure sustainable affordability for homebuyers.

What are the short-term and long-term effects of the RBA’s rate cut on housing affordability?

In the short term, the RBA’s rate cut to 4.10% reduces borrowing costs, temporarily improving housing affordability by increasing buyer capacity. However, heightened demand, driven by investor activity and market competition, quickly inflates property prices, negating affordability gains. Long-term effects are shaped by persistent supply-side constraints, including labor shortages and rising construction costs, which exacerbate price pressures. Historical trends, such as the 2019 rate cut cycle, reveal similar patterns of speculative growth. To achieve sustainable affordability, policymakers must integrate fiscal measures like subsidies for affordable housing and stricter investor regulations alongside monetary policy adjustments.

How do supply-side constraints, such as labor shortages, interact with the RBA’s monetary policy changes?

Supply-side constraints, including labor shortages and rising construction costs, limit the effectiveness of the RBA’s monetary policy changes by restricting housing supply growth. While the rate cut to 4.10% boosts borrowing capacity and fuels demand, these structural bottlenecks exacerbate affordability challenges as property prices rise faster than supply can adjust. For instance, new housing construction remains 20% below pre-pandemic levels, intensifying competition in high-demand markets like Sydney and Brisbane. Addressing these constraints through targeted fiscal policies, such as subsidies for builders and streamlined approval processes, is critical to aligning monetary easing with sustainable housing market dynamics.

What strategies can first-time homebuyers adopt to navigate the competitive market post-rate cut?

First-time homebuyers can enhance their market position by securing pre-approval to lock in competitive rates before demand surges. Reducing personal debt and improving credit scores are essential to maximize borrowing capacity under adjusted serviceability buffers. Leveraging government incentives, such as the First Home Guarantee, can lower deposit requirements and avoid Lenders Mortgage Insurance costs. Buyers should also focus on emerging suburbs or regional areas where competition is less intense. Proactive financial planning, including budgeting for potential price increases, ensures readiness in a dynamic market. Aligning these strategies with expert advice helps navigate affordability challenges post-rate cut effectively.

How does investor activity impact property prices and market dynamics following the RBA’s decision?

Investor activity, reignited by the RBA’s rate cut to 4.10%, intensifies property price growth and reshapes market dynamics. Lower borrowing costs enable investors to outbid first-time buyers, particularly in high-demand areas like Sydney and Brisbane. CoreLogic data from February 2025 shows a 0.3% national home value increase, driven by speculative purchases. Additionally, tight rental markets with historically low vacancy rates and rising rents attract investors seeking strong cash flow returns. This creates a feedback loop, inflating prices and sidelining entry-level buyers. Policymakers can mitigate these effects through stricter investor lending criteria and incentives for affordable housing developments.