RBA Rate Cuts: Because Waiting for Godot Was Too Mainstream

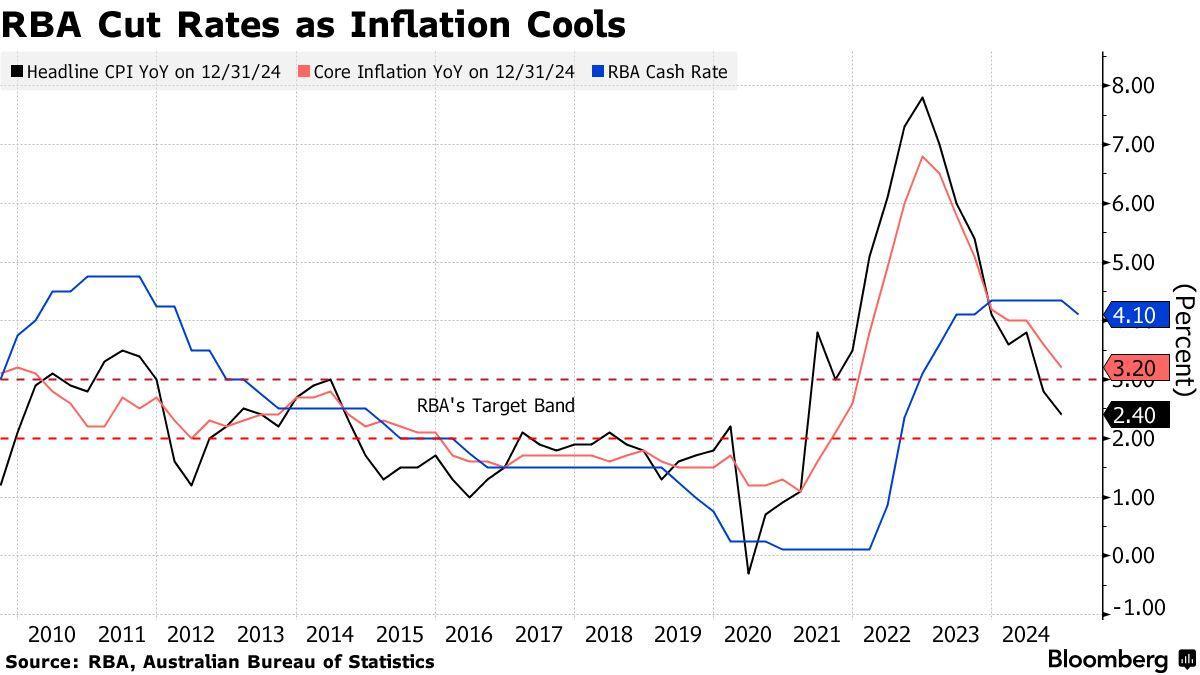

In February 2025, the Reserve Bank of Australia (RBA) executed its first interest rate cut in over four years, reducing the cash rate to 4.10%. While the move might seem routine, it arrives against a backdrop of unexpected resilience in the labor market—unemployment remains at a historic low of 4.0%, defying traditional economic models that link rate cuts to weak employment conditions. Governor Michele Bullock described the decision as a response to “subdued growth in private demand” and inflation easing to 3.2%, a level not seen since mid-2022.

This rate cut, however, is far from a straightforward stimulus. Economists like Dr. Shane Oliver, Head of Investment Strategy at AMP, emphasize its “hawkish” undertone, signaling caution rather than aggressive easing. The RBA’s approach reflects a delicate balancing act: supporting growth without reigniting inflationary pressures, particularly as global central banks adopt divergent monetary policies.

The implications extend beyond macroeconomics. With Australian mortgage holders set to save approximately $108 monthly on a $660,000 loan, the decision offers immediate relief to households. Yet, the broader economic impact remains uncertain, as sluggish GDP growth—just 0.3% in the last quarter—raises questions about the effectiveness of monetary policy in a post-pandemic landscape.

Image source: bloomberg.com

The Function of the Cash Rate

The cash rate operates as the cornerstone of Australia’s monetary policy, directly influencing the cost of borrowing and the availability of credit. Its primary function lies in setting the benchmark for overnight interbank loans, which cascades into broader financial markets, shaping interest rates on mortgages, business loans, and savings accounts. This mechanism ensures that liquidity flows align with the Reserve Bank of Australia’s (RBA) economic objectives.

A critical yet underappreciated aspect of the cash rate’s function is its role in managing Exchange Settlement (ES) balances. These balances, held by banks at the RBA, are pivotal for maintaining liquidity equilibrium. By adjusting the cash rate, the RBA indirectly influences the demand and supply of these balances, ensuring stability in the overnight money market. This technical precision minimizes volatility and supports predictable financial conditions.

“The cash rate is not merely a cost metric; it’s a signal of economic direction and intent,” explains Dr. Shane Oliver, Head of Investment Strategy at AMP.

This dual role—practical and perceptual—underscores the cash rate’s complexity, requiring both quantitative expertise and strategic foresight.

Historical Context of RBA Rate Decisions

The Reserve Bank of Australia’s (RBA) historical rate decisions reveal a nuanced interplay between monetary policy tools and broader economic dynamics. One critical yet often overlooked aspect is the role of Exchange Settlement (ES) balances in shaping these decisions. While public discourse frequently centers on inflation or employment metrics, the RBA’s adjustments to ES balances have historically served as a subtle yet powerful mechanism for liquidity management.

This approach reflects a deliberate calibration rather than reactive policymaking. For instance, during the 2016–2019 period, the RBA maintained higher interest rates compared to other advanced economies, prioritizing financial stability over immediate economic stimulus. This decision was informed by concerns over household debt and dwelling prices, as highlighted in research published in Economic Record. However, critics argue that this strategy contributed to inflation undershooting its target, underscoring the trade-offs inherent in such decisions.

“The art of monetary policy lies in balancing competing objectives without destabilizing market confidence,” notes Dr. Shane Oliver, Head of Investment Strategy at AMP.

By integrating ES balance adjustments with broader policy goals, the RBA has demonstrated a capacity to influence market liquidity and credit conditions. This historical context underscores the complexity of rate decisions, where technical precision often outweighs headline metrics.

Factors Leading to the Recent Rate Cut

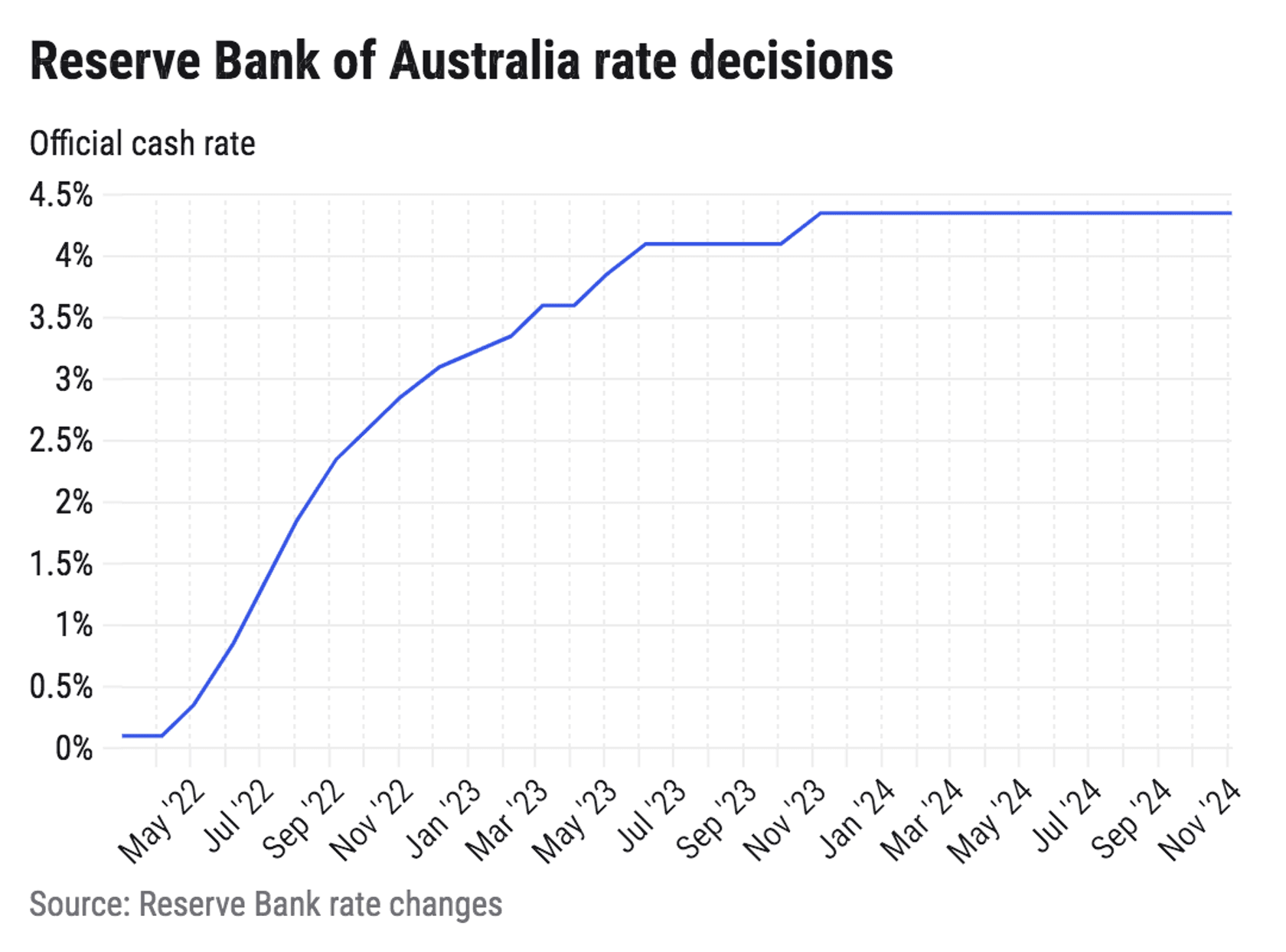

The Reserve Bank of Australia’s (RBA) decision to lower the cash rate to 4.10% reflects a confluence of domestic and international pressures, each revealing critical shifts in Australia’s economic landscape. Central to this move was the December 2024 inflation data, which showed underlying inflation easing to 3.2%, a level not seen since mid-2022. This decline, coupled with subdued private demand, signaled that inflationary pressures were receding faster than anticipated, creating room for monetary easing.

A less obvious but equally significant factor was the labor market’s resilience. Despite unemployment stabilizing at 4.0%, wage growth has decelerated, reducing the risk of a wage-price spiral. This counterintuitive dynamic—strong employment coexisting with weaker wage pressures—challenged traditional economic models and underscored the need for nuanced policy adjustments.

Globally, the RBA faced mounting uncertainties, including volatile commodity prices and divergent monetary policies among major central banks. These external forces amplified the importance of maintaining a competitive exchange rate, as the Australian dollar’s depreciation post-cut could bolster export competitiveness but also raise import costs.

By integrating these factors, the RBA demonstrated a strategic pivot, balancing domestic recovery with global economic realities.

Image source: capitalbrief.com

Economic Indicators Influencing the Decision

The Reserve Bank of Australia (RBA) relied on nuanced economic indicators to inform its recent rate cut, emphasizing metrics that extend beyond headline figures like inflation and GDP growth. One critical yet underappreciated measure was the analysis of Exchange Settlement (ES) balances, which provided real-time insights into liquidity conditions. These balances, held by financial institutions at the RBA, act as a barometer for interbank lending activity and broader credit availability. A sustained decline in ES balances often signals tightening liquidity, prompting preemptive monetary easing to stabilize financial conditions.

Another pivotal factor was the deceleration in wage growth despite historically low unemployment. This anomaly, indicative of subdued private sector demand, challenged traditional models that link tight labor markets to inflationary pressures. By integrating granular data, such as sector-specific employment trends and retail transaction volumes, the RBA identified early signs of economic softening that broader metrics failed to capture.

“Policy decisions hinge on understanding the interplay of microeconomic signals within macroeconomic frameworks,” explains Dr. Luci Ellis, Assistant Governor at the RBA.

This approach underscores the importance of blending technical precision with strategic foresight, enabling the RBA to navigate complex economic dynamics while maintaining its dual mandate of price stability and full employment.

Global Economic Conditions and Their Impact

The Reserve Bank of Australia’s (RBA) recent rate cut reflects the intricate influence of global economic conditions, particularly the divergence in monetary policies among major economies. This divergence creates a complex environment where synchronized global downturns amplify the challenges of domestic policy-making. For instance, while the U.S. Federal Reserve and the European Central Bank have pursued aggressive rate cuts, the RBA must navigate the resulting capital flow shifts, which can destabilize the Australian dollar.

One critical mechanism at play is the impact of exchange rate volatility on trade competitiveness. A depreciating Australian dollar, while beneficial for exporters, raises the cost of imports, potentially fueling inflationary pressures. This duality forces the RBA to weigh the benefits of supporting domestic industries against the risks of eroding purchasing power.

“Global monetary policy divergence often acts as a magnifier for domestic vulnerabilities, requiring central banks to adopt a more adaptive stance,” explains Dr. Nerida Conisbee, Chief Economist at Ray White.

Additionally, volatile commodity prices, particularly in energy and minerals, further complicate the RBA’s strategy. Fluctuations in these markets not only affect export revenues but also influence inflation expectations, making precise policy calibration essential. These dynamics underscore the necessity for a forward-looking approach that integrates global trends with domestic realities, ensuring economic stability amidst uncertainty.

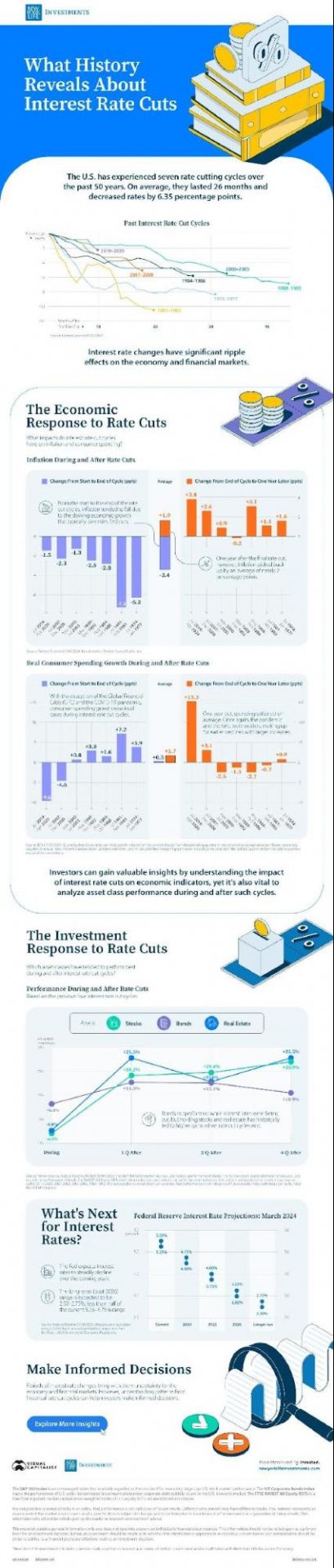

Implications of the Rate Cut on the Economy

The Reserve Bank of Australia’s (RBA) recent rate cut to 4.10% has initiated a cascade of economic adjustments, with effects that extend far beyond immediate borrowing costs. One critical outcome is the recalibration of consumer spending patterns. According to data from the Australian Bureau of Statistics, household savings rates have declined to 3.6%, their lowest since 2008, suggesting that lower interest rates may further incentivize spending over saving. This shift could stimulate retail and service sectors but risks reigniting inflationary pressures if demand outpaces supply.

In the business sector, reduced borrowing costs are expected to spur investment, particularly in capital-intensive industries like manufacturing and technology. For example, Deloitte Access Economics projects a 2.4% increase in private capital expenditure by mid-2025, driven by cheaper credit. However, this optimism is tempered by concerns over global supply chain disruptions, which could limit the effectiveness of such investments.

A less visible but equally significant impact lies in the banking sector. Lower rates compress net interest margins, compelling banks to innovate revenue streams. This dynamic underscores the dual-edged nature of rate cuts: while they aim to stimulate growth, they also challenge financial institutions to adapt strategically.

Economic Indicators Influencing the Decision

The Reserve Bank of Australia (RBA) relied on nuanced economic indicators to inform its recent rate cut, emphasizing metrics that extend beyond headline figures like inflation and GDP growth. One critical yet underappreciated measure was the analysis of Exchange Settlement (ES) balances, which provided real-time insights into liquidity conditions. These balances, held by financial institutions at the RBA, act as a barometer for interbank lending activity and broader credit availability. A sustained decline in ES balances often signals tightening liquidity, prompting preemptive monetary easing to stabilize financial conditions.

Another pivotal factor was the deceleration in wage growth despite historically low unemployment. This anomaly, indicative of subdued private sector demand, challenged traditional models that link tight labor markets to inflationary pressures. By integrating granular data, such as sector-specific employment trends and retail transaction volumes, the RBA identified early signs of economic softening that broader metrics failed to capture.

“Policy decisions hinge on understanding the interplay of microeconomic signals within macroeconomic frameworks,” explains Dr. Luci Ellis, Assistant Governor at the RBA.

This approach underscores the importance of blending technical precision with strategic foresight, enabling the RBA to navigate complex economic dynamics while maintaining its dual mandate of price stability and full employment.

Global Economic Conditions and Their Impact

The Reserve Bank of Australia’s (RBA) recent rate cut reflects the intricate influence of global economic conditions, particularly the divergence in monetary policies among major economies. This divergence creates a complex environment where synchronized global downturns amplify the challenges of domestic policy-making. For instance, while the U.S. Federal Reserve and the European Central Bank have pursued aggressive rate cuts, the RBA must navigate the resulting capital flow shifts, which can destabilize the Australian dollar.

One critical mechanism at play is the impact of exchange rate volatility on trade competitiveness. A depreciating Australian dollar, while beneficial for exporters, raises the cost of imports, potentially fueling inflationary pressures. This duality forces the RBA to weigh the benefits of supporting domestic industries against the risks of eroding purchasing power.

“Global monetary policy divergence often acts as a magnifier for domestic vulnerabilities, requiring central banks to adopt a more adaptive stance,” explains Dr. Nerida Conisbee, Chief Economist at Ray White.

Additionally, volatile commodity prices, particularly in energy and minerals, further complicate the RBA’s strategy. Fluctuations in these markets not only affect export revenues but also influence inflation expectations, making precise policy calibration essential. These dynamics underscore the necessity for a forward-looking approach that integrates global trends with domestic realities, ensuring economic stability amidst uncertainty.

Implications of the Rate Cut on the Economy

The Reserve Bank of Australia’s (RBA) recent rate cut to 4.10% has initiated a cascade of economic adjustments, with effects that extend far beyond immediate borrowing costs. One critical outcome is the recalibration of consumer spending patterns. According to data from the Australian Bureau of Statistics, household savings rates have declined to 3.6%, their lowest since 2008, suggesting that lower interest rates may further incentivize spending over saving. This shift could stimulate retail and service sectors but risks reigniting inflationary pressures if demand outpaces supply.

In the business sector, reduced borrowing costs are expected to spur investment, particularly in capital-intensive industries like manufacturing and technology. For example, Deloitte Access Economics projects a 2.4% increase in private capital expenditure by mid-2025, driven by cheaper credit. However, this optimism is tempered by concerns over global supply chain disruptions, which could limit the effectiveness of such investments.

A less visible but equally significant impact lies in the banking sector. Lower rates compress net interest margins, compelling banks to innovate revenue streams. This dynamic underscores the dual-edged nature of rate cuts: while they aim to stimulate growth, they also challenge financial institutions to adapt strategically.

Image source: visualcapitalist.com

Effects on Consumer Spending and Business Investment

The RBA’s rate cut to 4.10% has nuanced implications for consumer spending, particularly in discretionary categories. While lower borrowing costs reduce mortgage repayments, freeing up disposable income, the response is uneven across demographics. High-income households often channel these savings into durable goods or investments, whereas lower-income groups may prioritize debt reduction. This divergence highlights the importance of consumer confidence as a mediating factor. Recent data from the ANZ-Roy Morgan Consumer Confidence Index, which fell to 86.7 points in February 2025, underscores lingering caution among households despite improved financial conditions.

For businesses, the reduction in financing costs creates opportunities for capital-intensive investments, particularly in sectors like technology and manufacturing. However, the effectiveness of this stimulus is tempered by external constraints. Supply chain disruptions and volatile commodity prices limit the ability of firms to fully capitalize on cheaper credit. For instance, the NAB Monthly Business Survey reported a decline in capacity utilization from 82.7% to 82% in January 2025, reflecting underutilized resources despite improved borrowing conditions.

“Monetary easing provides a foundation for growth, but its success depends on resolving structural bottlenecks,”

— Dr. Nerida Conisbee, Chief Economist, Ray White

This dynamic interplay between reduced costs and external challenges underscores the complexity of translating rate cuts into sustained economic momentum.

Impact on the Real Estate and Banking Sectors

The RBA’s rate cut to 4.10% has introduced a dual-edged dynamic for the real estate and banking sectors, with each responding to distinct pressures and opportunities. In real estate, the immediate effect is an increase in borrowing capacity, which enhances affordability for buyers and investors. However, this does not uniformly translate into market acceleration. Persistent supply constraints, particularly in urban centers, limit the ability of increased demand to drive transaction volumes. This underscores the importance of aligning monetary policy with structural reforms in housing supply.

For the banking sector, the rate cut compresses net interest margins, a critical profitability metric. To mitigate this, banks are increasingly pivoting toward fee-based revenue models, such as wealth management services and transaction fees. This shift, while necessary, introduces operational complexities, including heightened regulatory scrutiny and the need for advanced risk management frameworks.

“Banks must innovate to sustain profitability, but this innovation must not come at the expense of financial stability,”

— Dr. Shane Oliver, Head of Investment Strategy, AMP

The interplay between these sectors highlights a broader challenge: while rate cuts aim to stimulate economic activity, their effectiveness is contingent on addressing underlying structural inefficiencies, such as housing shortages and banking sector adaptability.

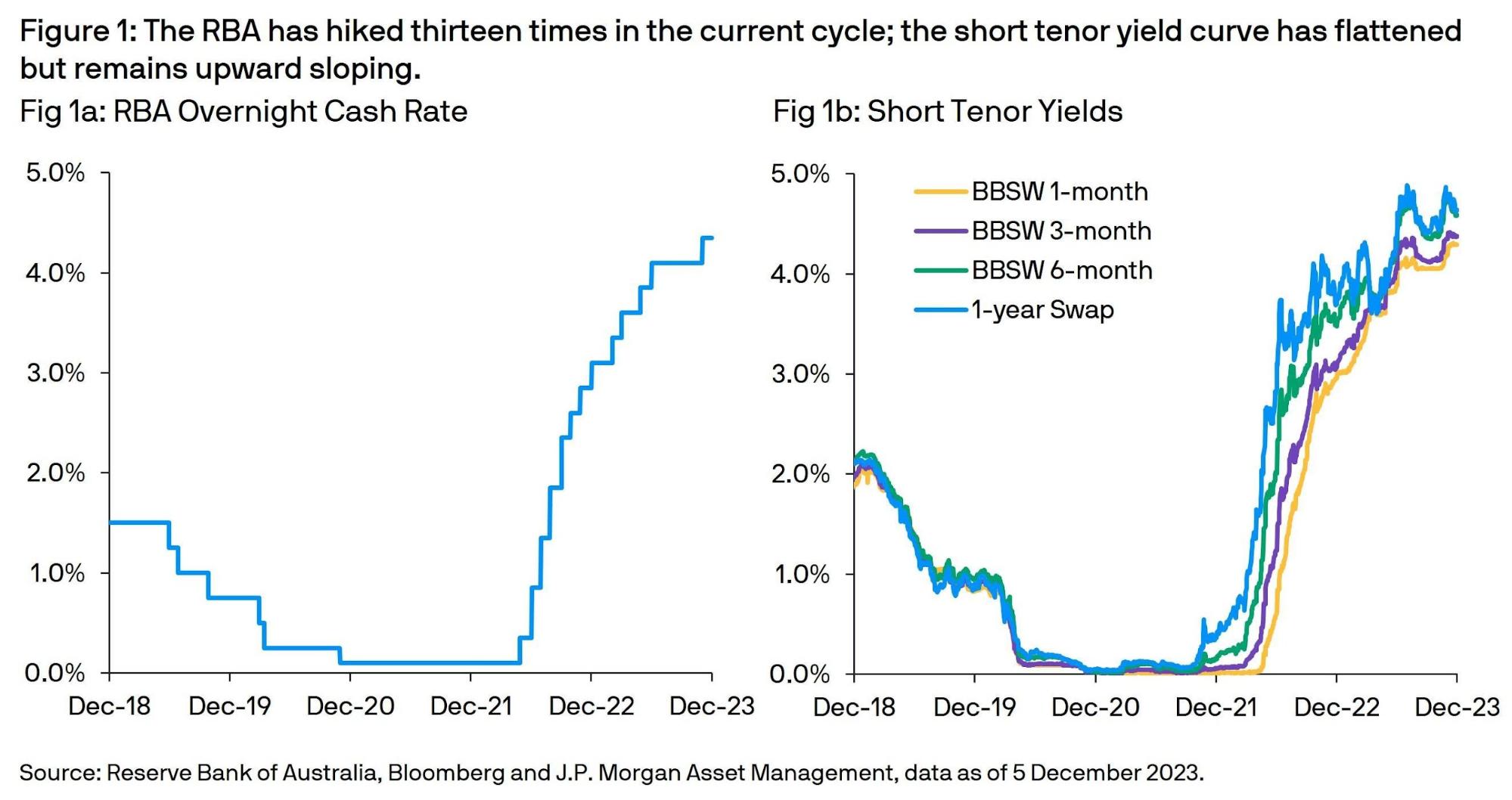

Future Projections and Potential Challenges

The Reserve Bank of Australia’s (RBA) cautious approach to rate cuts underscores a critical challenge: navigating the lagged effects of monetary policy in an increasingly volatile global economy. According to the Review of the Reserve Bank of Australia, monetary policy operates with significant delays, often taking 12 to 18 months to fully influence inflation and employment. This delay complicates forward guidance, as premature easing risks reigniting inflation, while delayed action could stifle recovery.

Emerging global risks further amplify these challenges. For instance, China’s economic slowdown—marked by a projected GDP growth dip to 4.5% in 2025—threatens Australia’s export-driven sectors, particularly minerals and education. Simultaneously, volatile commodity prices and geopolitical tensions could destabilize trade flows, forcing the RBA to recalibrate its strategies.

To mitigate these risks, experts like Dr. Warwick McKibbin advocate for integrating fiscal policy with monetary measures, emphasizing targeted infrastructure investments to counteract weak productivity growth. This dual approach could enhance resilience while addressing structural inefficiencies.

Image source: am.jpmorgan.com

RBA’s Forward Guidance and Market Expectations

Forward guidance by the Reserve Bank of Australia (RBA) operates as a strategic tool to shape market expectations, but its effectiveness hinges on the precision of its communication. A critical aspect often overlooked is the role of conditionality in these statements. By embedding caveats tied to inflation and employment metrics, the RBA ensures flexibility, allowing it to adapt to evolving economic conditions without committing to rigid policy paths. This approach minimizes market volatility but introduces interpretative challenges for stakeholders.

One notable limitation arises when market participants misinterpret conditionality as certainty. For instance, during the February 2025 rate cut, the RBA’s reference to “subdued private demand” was perceived as a definitive signal of prolonged easing, leading to unexpected shifts in bond yields. This underscores the importance of clarity in forward guidance to prevent overreactions.

“Forward guidance is not a promise but a framework for navigating uncertainty,”

— Dr. Nerida Conisbee, Chief Economist, Ray White

Ultimately, the interplay between nuanced language and real-time data highlights the complexity of aligning policy intentions with market interpretations, demanding both precision and adaptability.

Exploring Unconventional Monetary Policy Tools

One of the most intricate yet underexplored unconventional monetary policy tools is the strategic management of Exchange Settlement (ES) balances. These balances, held by financial institutions at the Reserve Bank of Australia (RBA), serve as a critical lever for maintaining liquidity equilibrium in the financial system. By adjusting the supply of ES balances, the RBA can influence interbank lending rates without altering the headline cash rate, offering a more targeted approach to stabilizing financial markets.

This mechanism operates through precise liquidity injections or withdrawals, often via open market operations. For instance, during periods of heightened market stress, the RBA can increase ES balances to ensure banks have sufficient liquidity to meet their obligations, thereby preventing credit market disruptions. Conversely, reducing these balances can tighten liquidity, curbing excessive risk-taking. Such interventions are particularly effective in volatile environments where traditional rate cuts might exacerbate instability.

A notable example of this approach was observed during the COVID-19 pandemic, when the RBA utilized its Term Funding Facility to complement ES balance adjustments. This dual strategy ensured credit availability while maintaining market confidence. However, as Dr. Philip Lowe, RBA Governor, has noted, these tools require careful calibration to avoid unintended consequences, such as distorting asset prices or encouraging moral hazard.

“Unconventional tools demand precision and restraint, as their misuse can undermine financial stability,”

— Dr. Philip Lowe, Governor, RBA

Ultimately, the nuanced application of ES balance management underscores its value as a surgical instrument in the central bank’s toolkit, bridging gaps where conventional policies fall short.

FAQ

What are the primary economic indicators influencing the Reserve Bank of Australia’s rate cut decisions?

The Reserve Bank of Australia evaluates a range of economic indicators when determining rate cuts. Key metrics include inflation trends, particularly the trimmed mean CPI, which reflects core price stability. Labor market conditions, such as unemployment rates and wage growth, are analyzed for their impact on demand-driven inflation. Additionally, GDP growth rates and private sector demand signal broader economic momentum. Exchange Settlement (ES) balances provide insights into liquidity conditions, while global factors like commodity prices and monetary policy divergence influence external pressures. These interconnected indicators guide the RBA’s strategy, ensuring alignment with its dual mandate of price stability and full employment.

How do RBA rate cuts impact Australian mortgage holders and the broader housing market?

RBA rate cuts directly lower borrowing costs for Australian mortgage holders, reducing monthly repayments and increasing disposable income. This enhanced affordability often boosts buyer confidence, driving demand in the housing market. Additionally, rate cuts expand borrowing capacity, enabling buyers to secure larger loans, which can elevate property prices, particularly in high-demand areas. For the broader housing market, increased investor activity and construction sector growth are common outcomes, as lower rates stimulate new developments. However, persistent supply constraints and regional disparities may temper these effects, highlighting the complex interplay between monetary policy, housing affordability, and market dynamics.

What role do global monetary policies play in shaping the RBA’s interest rate strategies?

Global monetary policies significantly influence the RBA’s interest rate strategies by shaping capital flows, exchange rate dynamics, and trade competitiveness. When major central banks, such as the U.S. Federal Reserve or European Central Bank, adopt expansionary policies, lower global interest rates can attract capital to Australia, appreciating the Australian dollar. This impacts export competitiveness and inflation. Conversely, divergent policies may create external pressures, requiring the RBA to adjust its stance to maintain economic stability. Additionally, global factors like commodity price volatility and geopolitical risks further intertwine with domestic considerations, underscoring the interconnected nature of monetary policy in a globalized economy.

How does the management of Exchange Settlement (ES) balances complement traditional rate cuts in Australia?

The management of Exchange Settlement (ES) balances complements traditional rate cuts by stabilizing interbank liquidity and ensuring the cash rate aligns with the RBA’s target. By adjusting the supply of ES balances through open market operations, the RBA influences overnight lending rates, indirectly affecting broader financial conditions. High ES balances reduce funding pressures, amplifying the impact of rate cuts on credit availability. This mechanism also mitigates market volatility during economic stress, ensuring smooth payment settlements. Together, ES balance management and rate adjustments form a cohesive strategy, enhancing monetary policy effectiveness while maintaining financial system stability in Australia’s dynamic economic landscape.

What are the potential long-term economic implications of the RBA’s recent rate cut cycle?

The RBA’s recent rate cut cycle may yield nuanced long-term economic implications. Lower borrowing costs could stimulate sustained consumer spending and business investment, fostering GDP growth. However, prolonged low rates risk inflating asset bubbles, particularly in housing, exacerbating affordability issues. Compressed bank margins may drive financial institutions toward riskier revenue streams, potentially impacting systemic stability. Additionally, a depreciated Australian dollar could enhance export competitiveness but elevate import costs, influencing trade balances. Over time, the effectiveness of monetary policy may diminish if structural challenges, such as productivity stagnation and supply constraints, remain unaddressed, underscoring the need for complementary fiscal strategies.