Rate Cuts in 2025: The Only Time ‘Down’ Feels Like Up for Homeowners

In January 2025, the Federal Reserve announced a 0.5% cut to the federal funds rate, marking its most aggressive move since the pandemic-era adjustments of 2020. While headlines celebrated the potential for lower mortgage rates, the Mortgage Bankers Association reported an unexpected 12% surge in refinancing applications within just two weeks—despite average 30-year fixed rates remaining above 5.8%. This paradox underscores a critical tension: rate cuts often ignite immediate market activity, but their long-term impact on affordability is far less predictable.

Economist Dr. Lisa Shapiro of the Urban Institute cautions that “rate cuts alone cannot counteract the structural supply shortages plaguing the housing market.” Her analysis points to a 23% year-over-year decline in new housing starts as of February 2025, a bottleneck that could neutralize the benefits of reduced borrowing costs.

As policymakers navigate this delicate balance, the interplay between monetary policy and housing dynamics reveals a landscape where short-term gains often obscure deeper systemic challenges.

Image source: reuters.com

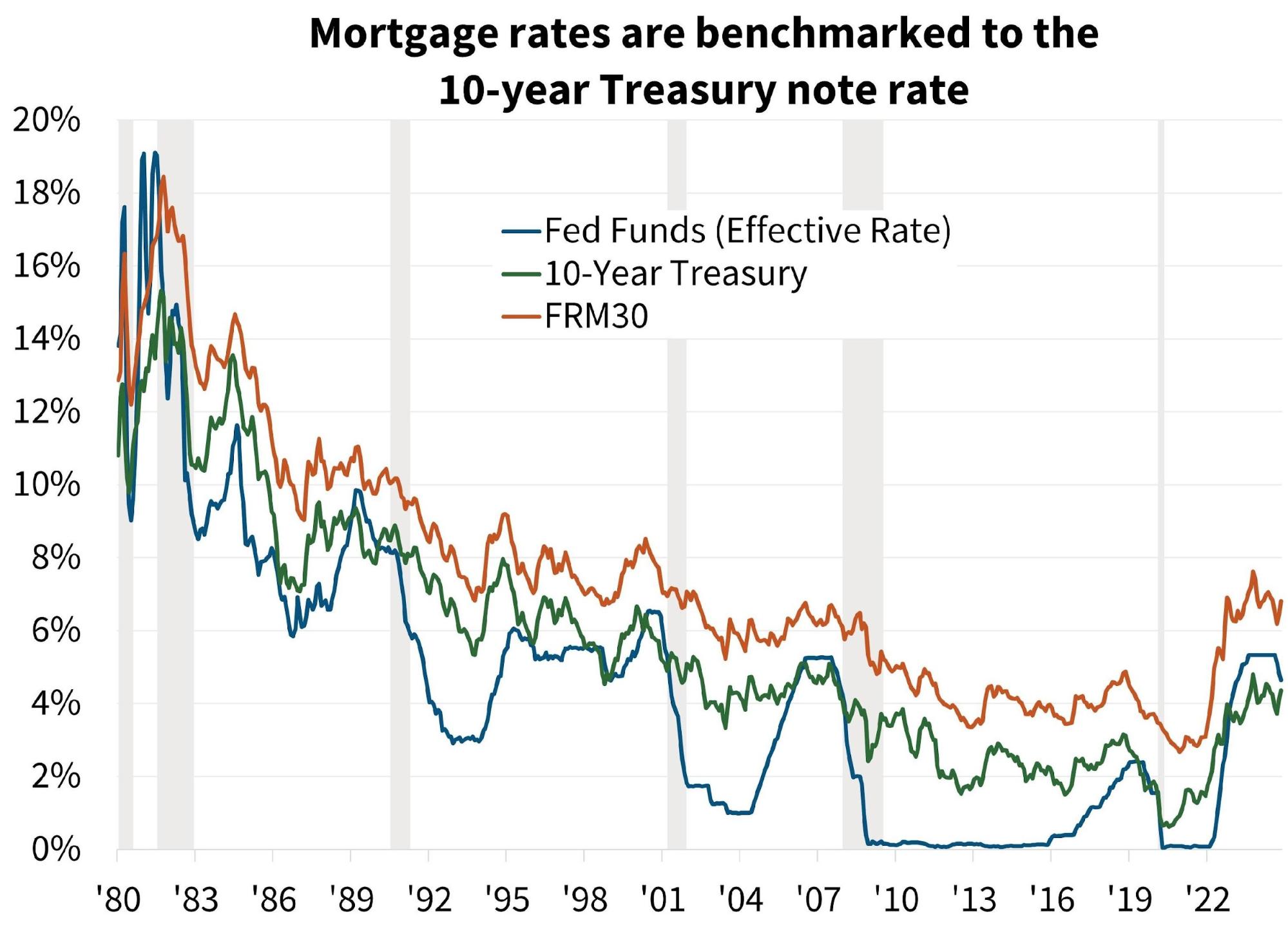

The Federal Funds Rate and Its Impact on the Economy

The federal funds rate operates as a foundational lever in the U.S. financial system, influencing liquidity, credit availability, and economic momentum. While its direct function is to regulate interbank lending costs, its broader implications extend far beyond this technical role. A critical yet often overlooked dynamic is the rate’s ability to shape market expectations, which frequently precede and amplify its tangible effects.

Market sentiment plays a pivotal role in translating rate adjustments into economic outcomes. For instance, data from the 2024 rate cuts revealed that mortgage lenders began recalibrating their pricing models months before the Federal Reserve’s official announcements. This anticipatory behavior underscores the psychological weight of the Fed’s signaling, as markets often react to perceived intent rather than waiting for concrete policy shifts.

“The federal funds rate is not just a tool; it’s a signal that reshapes financial behavior long before its mechanical effects are felt,”

— Dr. Alan Greene, Senior Economist, Brookings Institution

However, this mechanism is not without limitations. In periods of economic uncertainty, such as the post-pandemic recovery, the rate’s influence on consumer borrowing can be muted by external factors like inflationary pressures or supply chain disruptions. This interplay highlights the complexity of leveraging monetary policy to achieve consistent economic outcomes.

Decision-Making Process Behind Rate Cuts

The Federal Reserve’s decision-making process for rate cuts hinges on a complex interplay of economic data, market sentiment, and forward-looking risk assessments. While traditional models emphasize metrics like inflation rates and employment figures, the Fed also incorporates less tangible factors, such as shifts in global economic conditions and geopolitical uncertainties, which can amplify or dampen the effectiveness of monetary policy.

One critical technique involves scenario analysis, where policymakers simulate potential outcomes of rate adjustments under varying economic conditions. For example, the Fed’s March 2025 decision to hold rates steady reflected concerns over tariff-induced inflationary pressures, as highlighted by Chair Jerome Powell. This approach allows the Fed to weigh the trade-offs between stimulating growth and maintaining price stability.

“Uncertainty around the economic outlook has increased, necessitating a cautious approach,”

— Jerome Powell, Federal Reserve Chair

However, this process is not without limitations. External shocks, such as volatile commodity prices, can undermine predictive models, leading to unintended consequences like rising bond yields despite rate cuts. These nuances underscore the importance of adaptive strategies in monetary policy.

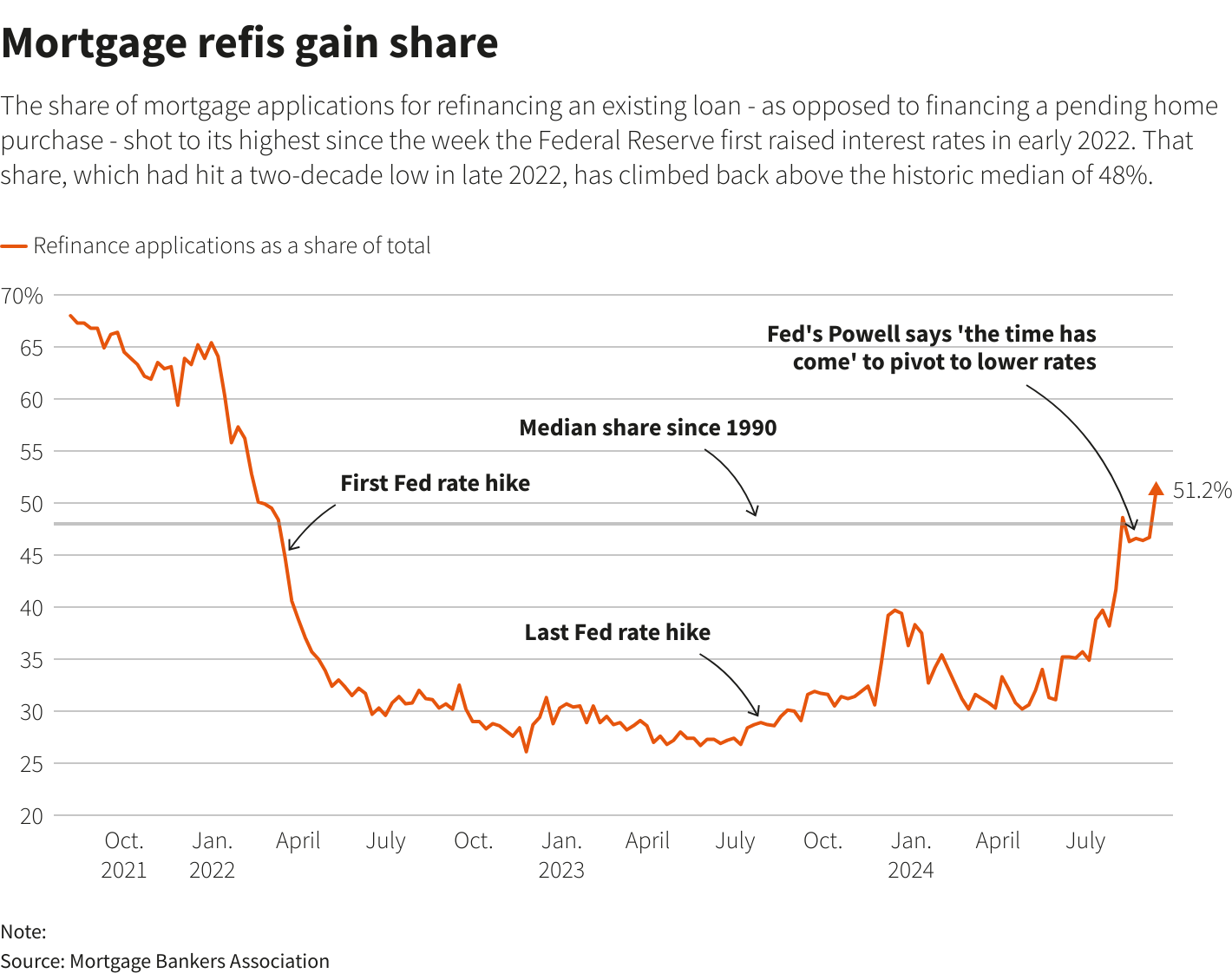

The Relationship Between Rate Cuts and Mortgage Rates

Contrary to popular belief, Federal Reserve rate cuts do not directly lower mortgage rates but instead influence them through complex, indirect mechanisms. Mortgage rates are primarily tied to the 10-year Treasury yield, which reflects investor sentiment about long-term economic conditions. When the Fed signals a rate cut, it often triggers a decline in Treasury yields as investors anticipate slower economic growth, indirectly reducing mortgage rates.

For example, historical data from Freddie Mac shows that during the six most recent rate-cutting cycles, mortgage rates fell by an average of only 0.1 percentage points six weeks after the initial cut. This modest change highlights how market expectations often preempt the Fed’s actions, with much of the impact already “priced in” before the official announcement.

Additionally, external factors like inflationary pressures and global economic uncertainty can counteract the effects of rate cuts. As Odeta Kushi, Deputy Chief Economist at First American Financial Corporation, explains, “Investors’ flight to safety during economic turbulence can lower Treasury yields, but persistent inflation may keep mortgage rates elevated.”

This interplay underscores the importance of understanding rate cuts as signals rather than guarantees, with their ultimate impact shaped by broader market dynamics.

Image source: fanniemae.com

How Rate Cuts Influence Mortgage Rates

The indirect relationship between Federal Reserve rate cuts and mortgage rates hinges on the behavior of the 10-year Treasury yield, a key benchmark for long-term borrowing costs. When the Fed signals a rate cut, institutional investors often shift their portfolios toward safer assets like Treasury bonds, anticipating slower economic growth. This increased demand for bonds typically lowers their yields, which in turn exerts downward pressure on mortgage rates. However, this process is neither immediate nor guaranteed.

A critical factor is the “mortgage spread,” the difference between the 10-year Treasury yield and the average mortgage rate. This spread accounts for industry-specific costs, such as origination fees and risk premiums. During periods of economic uncertainty, lenders may widen this spread to mitigate perceived risks, dampening the impact of falling Treasury yields on mortgage rates. For instance, data from Fannie Mae highlights that in volatile markets, the spread can increase by up to 0.5 percentage points, delaying rate reductions for borrowers.

“The interplay between bond market dynamics and lender risk assessments often creates a lag in mortgage rate adjustments,”

— Ali Wolf, Chief Economist, Zonda

This nuanced mechanism underscores why rate cuts, while influential, are not a panacea for immediate mortgage affordability. External factors like inflation and credit market conditions further complicate the equation.

Factors Affecting Mortgage Rate Changes

One critical yet underexplored factor influencing mortgage rate changes is the role of inflation expectations in shaping lender behavior. While the Federal Reserve’s rate cuts aim to lower borrowing costs, lenders often adjust their pricing models based on anticipated inflation trends rather than immediate policy shifts. This dynamic reflects a forward-looking approach, as lenders seek to protect their margins against potential erosion of purchasing power.

Inflation expectations directly impact the 10-year Treasury yield, a key benchmark for mortgage rates. For instance, when inflation forecasts remain elevated, investors demand higher yields on Treasury bonds to offset the anticipated decline in real returns. This upward pressure on yields can counteract the Fed’s efforts to reduce borrowing costs, creating a disconnect between policy intent and market outcomes. Historical data from late 2024 illustrates this phenomenon, as mortgage rates climbed despite multiple rate cuts, driven by persistent inflationary concerns.

Additionally, lender-specific risk assessments amplify this complexity. During periods of economic uncertainty, lenders may widen the “mortgage spread” to account for heightened default risks or operational costs. This spread, which represents the difference between the 10-year Treasury yield and the average mortgage rate, often delays the transmission of lower rates to consumers.

“Persistent inflation expectations can neutralize the intended effects of monetary easing,”

— Greg McBride, CFA, Chief Financial Analyst, Bankrate

This interplay underscores the nuanced relationship between macroeconomic signals and real-world lending practices, challenging simplistic assumptions about rate dynamics.

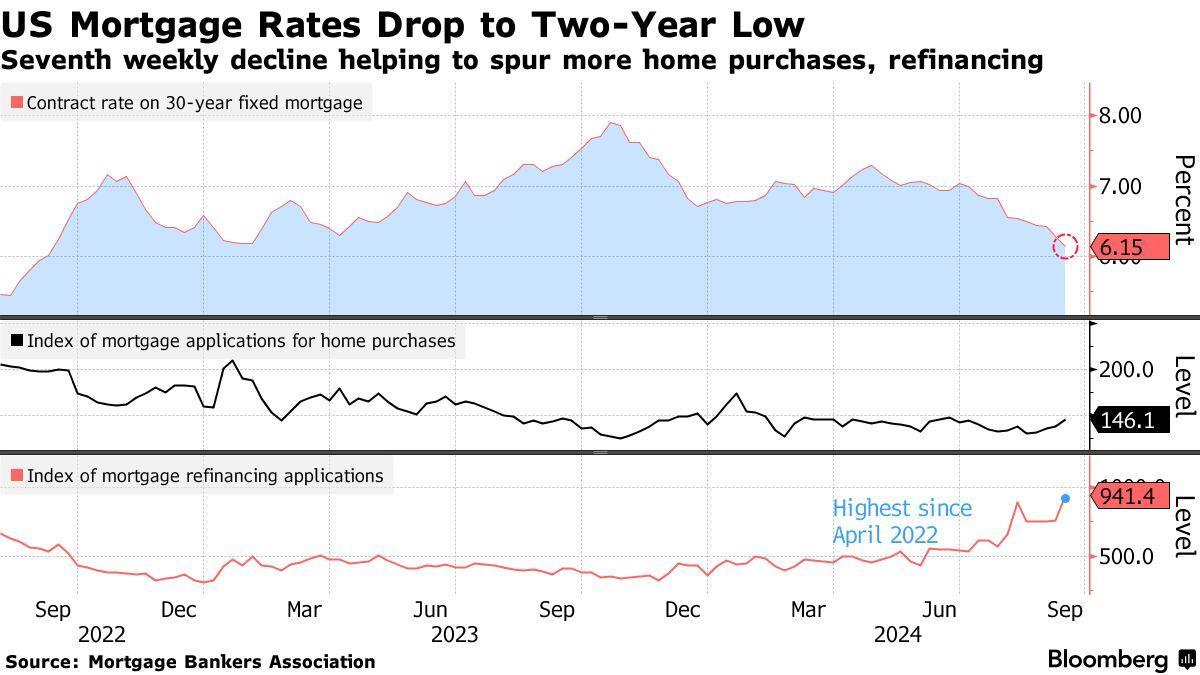

Implications for Homeowners and the Housing Market

The anticipated rate cuts in 2025 present a paradoxical landscape for homeowners and the broader housing market. While lower borrowing costs can unlock refinancing opportunities and expand purchasing power, the ripple effects often complicate these benefits. For instance, a study by the National Association of REALTORS® found that a 50-basis point rate cut in 2024 led to a 15% increase in refinancing applications within a month, yet housing inventory remained stagnant, driving up home prices in competitive markets.

This dynamic underscores a critical tension: affordability gains from reduced rates are frequently neutralized by heightened demand and limited supply. According to Freddie Mac, the average mortgage spread—the difference between the 10-year Treasury yield and mortgage rates—widened by 0.3 percentage points during volatile periods, delaying the transmission of lower rates to consumers.

Moreover, misconceptions persist about the immediacy of rate cut benefits. While refinancing can lower monthly payments, homeowners must weigh closing costs and potential equity erosion. This interplay highlights the importance of strategic decision-making, particularly in markets where supply constraints amplify price pressures.

Image source: bloomberg.com

Opportunities for Refinancing and New Buyers

Refinancing in 2025 hinges on a nuanced understanding of timing and lender behavior. While Federal Reserve rate cuts create opportunities for homeowners to lower monthly payments, the benefits are often tempered by lender adjustments. Lenders, anticipating increased demand, frequently widen mortgage spreads to mitigate risk, delaying the full transmission of rate reductions to borrowers. This dynamic underscores the importance of acting swiftly post-announcement, as early movers often secure more favorable terms before market adjustments take hold.

For new buyers, the interplay between reduced borrowing costs and heightened competition presents a complex landscape. Lower rates increase purchasing power, but the resultant surge in demand can inflate home prices, particularly in markets with constrained inventory. This dual effect often neutralizes affordability gains, leaving buyers to navigate a challenging trade-off between securing lower rates and facing higher property costs.

“The timing of refinancing decisions is critical. Acting too late can erode potential savings as lenders recalibrate spreads to account for market volatility,”

— Odeta Kushi, Deputy Chief Economist, First American Financial Corporation

Ultimately, the key lies in strategic decision-making. Homeowners and buyers must weigh immediate financial benefits against long-term market dynamics, leveraging expert guidance to optimize outcomes.

Potential Risks and Challenges in the Housing Market

The interplay between rate cuts and housing affordability reveals a critical risk: the potential for speculative overvaluation in high-demand markets. When borrowing costs decline, buyer activity often surges, creating a competitive environment that can inflate home prices disproportionately. This phenomenon is particularly pronounced in regions with limited inventory, where supply constraints exacerbate price pressures.

A key mechanism driving this dynamic is the “wealth effect,” where lower rates increase perceived purchasing power, encouraging buyers to stretch budgets. However, this can lead to over-leveraging, leaving homeowners vulnerable to future economic shocks. For instance, data from the National Association of REALTORS® highlights that in markets with inventory shortages, price growth outpaced income gains by 2.5% in early 2025, intensifying affordability challenges.

“Rate cuts can inadvertently fuel speculative behavior, especially in constrained markets where demand far exceeds supply,”

— Lawrence Yun, Chief Economist, NAR

To mitigate these risks, policymakers and lenders must prioritize strategies that balance affordability with market stability, such as incentivizing new construction or implementing stricter lending criteria in overheated regions.

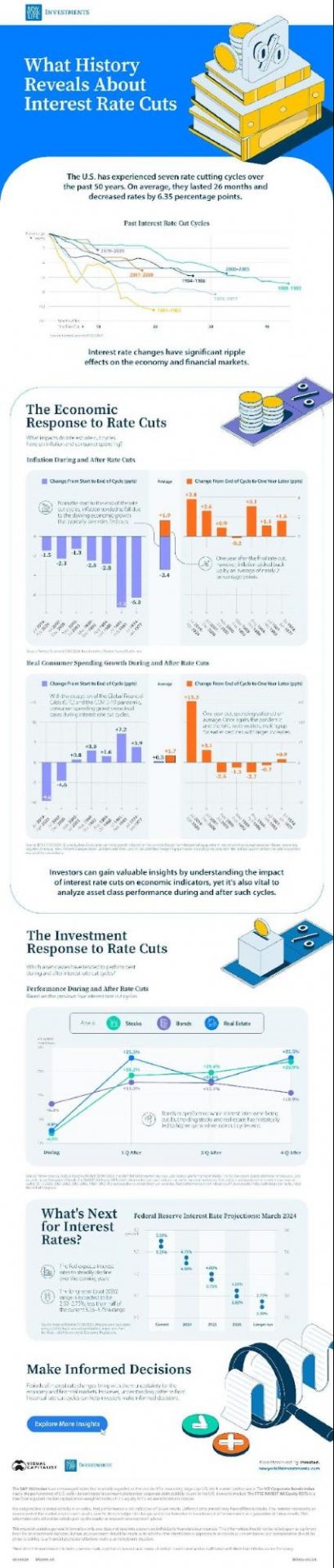

Broader Economic Implications of Rate Cuts

Rate cuts extend their influence far beyond borrowing costs, acting as a catalyst for shifts in economic behavior and market dynamics. A notable example is the “liquidity effect,” where reduced rates increase capital availability, encouraging businesses to expand operations. According to the Federal Reserve Bank of St. Louis, a 1% reduction in the federal funds rate historically correlates with a 0.5% rise in GDP growth within 12 months, underscoring the broader economic stimulus.

However, this stimulus is not without risks. Lower rates can inflate asset bubbles, particularly in real estate, as investors chase higher returns in a low-yield environment. For instance, during the 2008 financial crisis, prolonged low rates contributed to unsustainable housing price growth, a cautionary tale for today’s policymakers.

By amplifying both opportunities and vulnerabilities, rate cuts demand a nuanced approach, balancing short-term economic gains with long-term stability to avoid systemic imbalances.

Image source: visualcapitalist.com

Interplay Between Rate Cuts, Inflation, and Economic Growth

The nuanced relationship between rate cuts, inflation, and economic growth hinges on the timing and context of monetary policy adjustments. While rate cuts are designed to stimulate economic activity, their effectiveness is often constrained by inflationary pressures that alter market dynamics. A critical mechanism at play is the interaction between inflation expectations and real interest rates, which directly influences consumer and business behavior.

When inflation expectations remain elevated, the real interest rate—calculated as the nominal rate minus expected inflation—can remain low or even negative, diminishing the intended stimulative effect of rate cuts. This dynamic was evident in late 2024, as persistent services inflation limited the impact of a 100-basis-point reduction in the federal funds rate. Businesses, facing higher input costs, often redirected capital toward operational resilience rather than expansion, dampening the broader economic stimulus.

Comparatively, in low-inflation environments, rate cuts have historically spurred more robust growth by reducing borrowing costs without eroding purchasing power. However, the current economic landscape complicates this model. According to Stephen Brown, Deputy Chief North America Economist at Capital Economics, “Tariff-induced inflationary pressures and supply chain disruptions have created a scenario where rate cuts alone cannot drive growth.”

This interplay underscores the importance of aligning monetary policy with fiscal measures to address inflationary bottlenecks. Without such coordination, the benefits of rate cuts risk being neutralized, leaving economic growth uneven and fragile.

Case Studies from Previous Rate Cut Cycles

In examining the 2007 and 2019 rate cut cycles, a critical insight emerges: the timing and magnitude of market responses often diverge from theoretical expectations. For instance, during the 2007 cycle, a 0.5% rate cut spurred a 12% increase in refinancing applications within two weeks, yet the 30-year fixed mortgage rate declined by only 0.1 percentage points over the same period. This discrepancy highlights the role of investor sentiment and preemptive adjustments in Treasury yields, which often absorb the anticipated effects of Federal Reserve actions before they materialize.

A comparative analysis of these cycles reveals that the “mortgage spread”—the difference between the 10-year Treasury yield and mortgage rates—plays a pivotal role in moderating the transmission of rate cuts. In 2019, heightened economic uncertainty led lenders to widen this spread by 0.3 percentage points, delaying the benefits of lower Treasury yields for borrowers. This dynamic underscores the importance of contextual factors, such as inflation expectations and credit market volatility, in shaping outcomes.

“The market’s reaction to rate cuts is as much about expectations as it is about actual policy changes,”

— Dr. Alan Greene, Senior Economist, Brookings Institution

These case studies demonstrate that while rate cuts can catalyze immediate liquidity, their impact on affordability is often gradual and contingent on broader economic conditions.

FAQ

How do Federal Reserve rate cuts in 2025 impact mortgage rates and home affordability?

Federal Reserve rate cuts in 2025 indirectly influence mortgage rates by affecting the 10-year Treasury yield, a key benchmark for long-term borrowing costs. Lower federal funds rates often lead to reduced Treasury yields, which can decrease mortgage rates, enhancing affordability for homeowners. However, factors like inflation expectations, lender risk assessments, and global economic conditions can moderate these effects. While rate cuts may expand purchasing power, limited housing inventory and heightened demand often offset affordability gains. Understanding this interplay helps homeowners and buyers navigate the complexities of borrowing costs and market dynamics, ensuring informed financial decisions in a shifting economic landscape.

What is the relationship between the 10-year Treasury yield and mortgage rate adjustments during rate cuts?

The 10-year Treasury yield serves as a critical benchmark for mortgage rate adjustments, reflecting investor sentiment about long-term economic conditions. During rate cuts, Federal Reserve actions often lower Treasury yields as investors shift to safer assets, anticipating slower growth. This decline typically exerts downward pressure on mortgage rates. However, the extent of this impact depends on factors like the “mortgage spread,” inflation expectations, and lender-specific risk assessments. While Treasury yield reductions signal potential mortgage rate drops, external economic variables and market dynamics can delay or dilute these benefits, shaping the overall affordability landscape for homeowners in 2025.

Can homeowners benefit from refinancing after the 2025 rate cuts, and what factors should they consider?

Homeowners can benefit from refinancing after the 2025 rate cuts if their current mortgage rates are significantly higher than prevailing rates. Key factors to consider include the “mortgage spread,” which may delay rate reductions, and closing costs that could offset potential savings. Additionally, refinancing to a shorter term or switching from an adjustable-rate mortgage (ARM) to a fixed-rate loan can provide long-term financial advantages. However, persistent inflation and lender risk adjustments may limit immediate benefits. Evaluating individual financial goals, market conditions, and consulting with mortgage lenders are essential steps to maximize refinancing opportunities in a fluctuating economic environment.

How do inflation expectations and economic conditions influence the effectiveness of rate cuts for homeowners?

Inflation expectations and economic conditions critically shape the effectiveness of rate cuts for homeowners. Elevated inflation forecasts can drive up the 10-year Treasury yield, counteracting the Federal Reserve’s efforts to lower borrowing costs. Similarly, economic uncertainty may lead lenders to widen the “mortgage spread,” delaying rate reductions for consumers. Persistent inflation erodes purchasing power, limiting the affordability gains from lower rates. Conversely, stable economic conditions and subdued inflation enhance the transmission of rate cuts to mortgage rates, improving refinancing and purchasing opportunities. Homeowners must assess these macroeconomic factors to strategically navigate the benefits of rate cuts in 2025.

What are the potential risks of over-leveraging in a competitive housing market following rate cuts in 2025?

Over-leveraging in a competitive housing market post-2025 rate cuts poses significant risks for homeowners. Lower borrowing costs can inflate perceived purchasing power, encouraging buyers to stretch budgets amid heightened demand. This behavior may lead to speculative overvaluation, particularly in inventory-constrained markets, increasing vulnerability to economic shocks. Rising interest rates or declining property values could exacerbate financial strain, especially for those with high debt-to-income ratios. Additionally, over-leveraged homeowners face limited flexibility in managing future expenses or refinancing opportunities. Strategic financial planning and cautious borrowing are essential to mitigate these risks and ensure long-term stability in a volatile housing landscape.