First Home Buyers’ Guide to 2025: Because ‘Avocado Toast’ Isn’t the Real Villain

In 2024, the average age of first-time homebuyers in the United States reached 38—a historic high, according to the National Association of Realtors. This milestone reflects a seismic shift in the financial and social dynamics of homeownership, where rising home prices, stagnant wage growth, and record-high mortgage rates have redefined what it means to enter the housing market. The Federal Reserve’s aggressive rate hikes over the past two years, aimed at curbing inflation, have left mortgage rates hovering near 7%, locking many would-be buyers out of the market entirely.

Yet, the challenges extend beyond interest rates. According to a January 2025 report from the Department of Housing and Urban Development, the U.S. faces a shortfall of over 5 million homes, exacerbated by supply chain disruptions and labor shortages in the construction industry. Doug Bauer, CEO of Tri Pointe Homes, notes that while builders are optimistic about a strong spring season, the industry’s ability to meet demand remains constrained.

This confluence of factors has forced many buyers to adopt unconventional strategies, such as pooling resources with family or friends to secure a home. As intergenerational households grow more common, the housing market of 2025 is poised to test not just financial resilience but also the adaptability of those seeking to navigate its complexities.

Image source: blockchangere.com

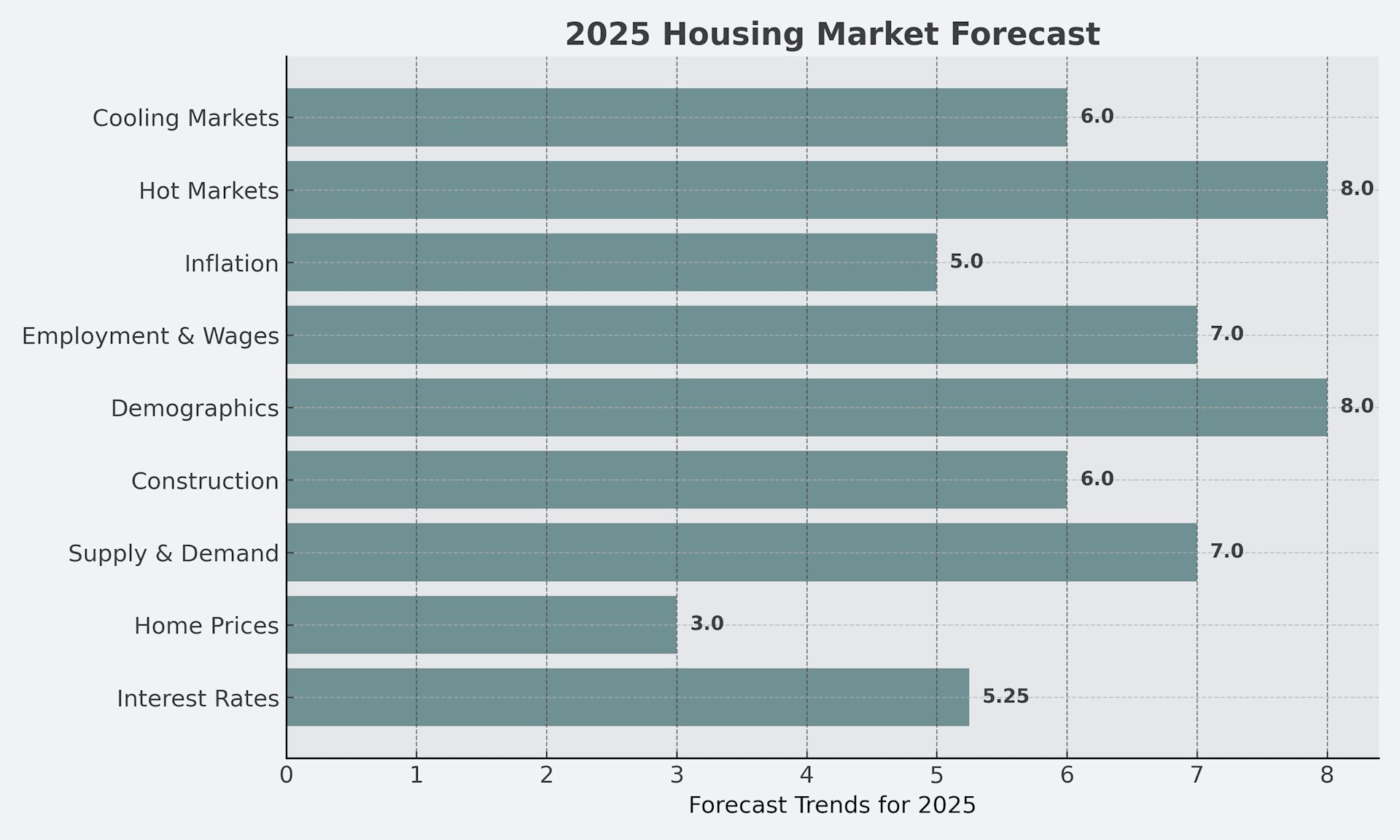

Key Market Trends and Predictions

The 2025 housing market is increasingly shaped by the interplay between remote work dynamics and the rise of energy-efficient housing. These trends are not merely reactions to economic pressures but represent a deeper shift in buyer priorities and market behavior. Remote work, for instance, has redefined the concept of “prime locations,” with suburban and exurban areas experiencing a surge in demand due to their affordability and quality of life. This shift has created opportunities for buyers to capitalize on emerging neighborhoods with long-term growth potential.

Energy-efficient homes, once a niche preference, are now a critical factor in property valuation. According to a 2025 report by the National Association of Realtors, homes with energy certifications sell 25% faster on average, reflecting growing consumer awareness of sustainability and cost savings. Builders are responding by integrating smart technologies and green materials, though this has introduced challenges in balancing upfront costs with market competitiveness.

“Sustainability is no longer optional—it’s a market expectation,” notes Sarah Chen, Chief Sustainability Officer at GreenBuild Solutions.

Understanding these trends requires a nuanced approach. Buyers must evaluate not just current amenities but also future-proofing factors like infrastructure upgrades and climate resilience. This strategic foresight transforms market data into actionable insights, empowering informed decisions.

Impact of Economic Policies on Home Buying

Economic policies directly influence your ability to navigate the housing market, often in ways that are less obvious but profoundly impactful. One critical mechanism is how Federal Reserve rate adjustments ripple through lending practices, reshaping affordability and access. When interest rates rise, as they have in recent years, the immediate effect is higher borrowing costs. However, this also prompts lenders to innovate, introducing adjustable-rate mortgages (ARMs) or hybrid loan products that cater to buyers seeking flexibility.

A comparative analysis reveals that while fixed-rate mortgages offer stability, ARMs can provide lower initial payments, making them attractive during periods of elevated rates. Yet, these products come with risks, particularly in volatile economic climates. The effectiveness of such options often depends on regional market conditions and individual financial profiles, underscoring the importance of tailored financial planning.

Contextual factors, such as state-level initiatives, further shape outcomes. For example, California’s MyHome Assistance Program has enabled thousands of first-time buyers to offset down payment challenges, demonstrating how localized policies can mitigate federal tightening.

“Economic policies are not just barriers; they’re catalysts for innovation,” notes Danielle Hale, Chief Economist at Realtor.com.

The key takeaway? Treat policy shifts as opportunities to explore adaptive strategies, leveraging both public programs and innovative lending tools to secure your place in the market.

Financial Readiness for First-Time Buyers

Achieving financial readiness as a first-time homebuyer in 2025 requires more than saving for a down payment—it demands a strategic approach to understanding and optimizing your financial profile. A recent study by the Urban Institute revealed that 53% of first-time buyers underestimate the total costs of homeownership, including property taxes, insurance, and maintenance. This oversight often leads to financial strain post-purchase, underscoring the importance of comprehensive financial planning.

Your credit score, a critical determinant of mortgage terms, functions as both a gatekeeper and a negotiator. According to FICO, a score of 760 or higher can reduce your mortgage interest rate by up to 1.5%, potentially saving tens of thousands over the loan’s lifespan. To achieve this, focus on reducing your credit utilization ratio below 30% and addressing any inaccuracies in your credit report.

Think of financial readiness as constructing a foundation for a house: solid preparation ensures stability, while shortcuts risk collapse. By aligning your financial health with market demands, you position yourself not just to buy a home, but to sustain it.

Image source: keepingcurrentmatters.com

Assessing Your Financial Health

Understanding your debt-to-income ratio (DTI) is a cornerstone of financial health assessment, yet its nuanced implications often go unnoticed. DTI measures the percentage of your gross monthly income allocated to debt payments, serving as a critical indicator of your borrowing capacity. While a DTI below 36% is generally considered healthy, the ideal threshold can vary based on regional housing costs and lender-specific criteria.

The importance of DTI lies in its dual role: it not only determines mortgage eligibility but also signals your financial resilience. A lower DTI enhances your ability to manage unexpected expenses, such as emergency repairs or rising property taxes. Conversely, a high DTI can lead to mortgage stress, where monthly payments consume a disproportionate share of income, increasing the risk of default.

“A well-managed DTI isn’t just about qualifying for a loan; it’s about ensuring long-term financial stability,” notes Danielle Hale, Chief Economist at Realtor.com.

To optimize your DTI, prioritize paying down high-interest debts and avoid new credit obligations before applying for a mortgage. Simulating different scenarios—such as interest rate hikes or income fluctuations—can further refine your financial strategy. This proactive approach transforms DTI from a static metric into a dynamic tool for sustainable homeownership.

Understanding Credit Scores and Their Impact

Your credit score is more than a static number; it’s a dynamic indicator of your financial behavior and a decisive factor in mortgage approval. One often-overlooked aspect is the interplay between credit utilization and credit mix. While many focus solely on timely payments, lenders scrutinize how much of your available credit you use and the diversity of your credit accounts. These factors can significantly influence your score and, by extension, your mortgage terms.

Consider the case of a prospective buyer with a 710 credit score. Despite consistent on-time payments, her high credit utilization—hovering at 65%—flagged her as a higher risk. By strategically reducing her balances to below 30% and adding a small installment loan to diversify her credit mix, her score improved by 40 points within six months. This adjustment secured her a lower interest rate, saving her over $15,000 across the loan’s lifespan.

“Credit scores are not just about repayment history; they reflect your overall financial management,”

— Sarah Johnson, Senior Credit Analyst at Equifax.

To leverage your credit score effectively, focus on maintaining low utilization, diversifying account types, and regularly reviewing your credit report for inaccuracies. These targeted actions transform your score into a powerful tool for financial advantage.

Navigating the Mortgage Process

Securing a mortgage is not merely a financial transaction; it’s a strategic exercise in aligning your resources with long-term goals. A critical yet often misunderstood step is understanding how loan structures impact your financial trajectory. For instance, a 30-year fixed-rate mortgage offers predictability, but opting for a 15-year term could save you over $100,000 in interest on a $300,000 loan, according to data from Freddie Mac. This trade-off, however, requires balancing higher monthly payments against future financial freedom.

Misconceptions about pre-approval also persist. Many buyers assume it guarantees a loan, but it’s a conditional commitment. Lenders evaluate your debt-to-income (DTI) ratio, which ideally should remain below 36%. A higher DTI can lead to rejection or less favorable terms, even after pre-approval. This underscores the importance of maintaining financial stability throughout the process.

Think of the mortgage process as constructing a bridge: each decision—loan type, term, and pre-approval—acts as a support beam. Missteps weaken the structure, while informed choices ensure a secure path to homeownership.

Image source: keepingcurrentmatters.com

Types of Mortgages and Their Long-Term Costs

Choosing the right mortgage type is not just about affordability today—it’s about managing financial resilience over decades. A critical yet underexplored factor is the interplay between loan term length and cumulative interest costs. While a 30-year fixed-rate mortgage offers lower monthly payments, the extended term significantly amplifies total interest paid. For instance, on a $300,000 loan at 6%, the 30-year term accrues over $347,000 in interest, compared to $155,000 for a 15-year term—a stark $192,000 difference.

Adjustable-rate mortgages (ARMs) introduce another layer of complexity. Their initial low rates can be enticing, but rate adjustments tied to market indices often lead to unpredictable payment increases. This volatility disproportionately impacts borrowers in high-rate environments, as seen during the Federal Reserve’s recent tightening cycle. The risk-reward balance of ARMs demands careful evaluation of future rate trends and personal financial stability.

Contextual factors, such as regional housing costs and local assistance programs, further influence mortgage suitability. For example, USDA loans, which require no down payment, are invaluable in rural areas but irrelevant in urban markets. Similarly, state-level grants can offset upfront costs, altering the calculus for first-time buyers.

“The true cost of a mortgage lies in its structure, not just its rate,”

— Lisa View, Mortgage Strategist

Ultimately, aligning loan type with long-term goals transforms mortgages from mere financial tools into strategic assets.

The Pre-Approval Process Explained

Pre-approval is more than a procedural step; it’s a diagnostic tool that uncovers your financial readiness and positions you strategically in the housing market. At its core, pre-approval involves a lender’s detailed evaluation of your income, assets, credit history, and debt obligations to determine your borrowing capacity. However, the nuances of this process reveal its true value.

One critical yet often overlooked aspect is the role of underwriting during pre-approval. Unlike pre-qualification, which offers a surface-level estimate, pre-approval involves a preliminary underwriting review. This step identifies potential red flags, such as inconsistent income documentation or high credit utilization, that could jeopardize final loan approval. Addressing these issues early not only strengthens your financial profile but also prevents delays during the closing process.

Comparatively, lenders offering expedited pre-approvals, such as Rate’s Same Day Mortgage, provide speed but may sacrifice depth in their analysis. While this can be advantageous in competitive markets, it underscores the importance of balancing efficiency with thoroughness.

“Pre-approval isn’t just a financial checkpoint; it’s a strategic advantage that ensures you’re prepared for every stage of the homebuying journey.”

— Sarah Chen, Chief Sustainability Officer at GreenBuild Solutions

By treating pre-approval as a comprehensive financial audit, you gain clarity, confidence, and a competitive edge in negotiations.

Effective House Hunting Strategies

Success in house hunting hinges on precision, adaptability, and leveraging technology to outpace competition. A 2025 study by the National Association of Realtors revealed that 97% of buyers used online tools to search for homes, yet only 42% felt confident in their decision-making. This gap underscores the need for a strategic approach.

Start by utilizing AI-powered real estate platforms that analyze market trends and predict property value trajectories. For instance, tools like Zillow’s AI-driven search can identify undervalued properties in emerging neighborhoods, offering a competitive edge. Pair this with augmented reality (AR) apps to visualize renovations or furniture placement, ensuring the property aligns with your vision.

Misconceptions about timing often derail buyers. Contrary to popular belief, off-peak seasons can yield better deals. Data from Realtor.com shows homes listed in January sell for 3% less on average, saving buyers thousands.

Think of house hunting as a chess game: every move—timing, technology, and negotiation—must align with your endgame.

Image source: theownteam.com

Leveraging Assistance Programs

Assistance programs are not merely financial stopgaps; they are strategic tools that can redefine your house-hunting approach. By bridging the gap between affordability and opportunity, these programs empower buyers to compete in high-demand markets without overextending their resources.

One critical mechanism is the structure of down payment assistance (DPA) programs. These initiatives often combine grants, forgivable loans, and deferred-payment options, each tailored to specific buyer needs. For instance, forgivable loans, such as those offered by the Florida Assist Program, eliminate repayment obligations if the homeowner meets residency requirements. This flexibility transforms what might seem like a financial hurdle into a manageable pathway to ownership.

Comparatively, state-level programs like the Texas State Affordable Housing Corporation (TSAHC) provide additional layers of support, including fixed-rate loans and benefits for specific professions. While these programs excel in reducing upfront costs, their effectiveness depends on regional housing prices and eligibility criteria, which can vary significantly.

“Assistance programs aren’t a fallback—they’re a strategic asset,”

— Lisa View, Mortgage Strategist

To maximize these opportunities, buyers must evaluate program compatibility with their financial profiles and local market conditions. This proactive approach not only enhances affordability but also positions buyers to secure properties that align with their long-term goals.

Bidding Wars and Negotiation Tactics

In high-stakes bidding wars, the most effective strategy often lies in uncovering and addressing the seller’s underlying priorities. While many buyers focus solely on escalating their offers, a nuanced approach that emphasizes non-monetary value can decisively tip the scales in your favor.

One advanced tactic is leveraging escalation clauses strategically. These clauses automatically increase your bid incrementally up to a set limit, ensuring competitiveness without overcommitting. However, their success hinges on precise calibration. For instance, setting too low a cap risks losing the property, while an excessively high cap may inflate the final price unnecessarily. This balance requires a deep understanding of local market dynamics and the seller’s motivations.

Contextual factors, such as the seller’s timeline, can also redefine negotiation dynamics. A seller relocating for work may prioritize a quick, seamless closing over marginally higher offers. In one notable case, a buyer secured a property by offering a 14-day close, bypassing higher bids that involved complex contingencies. This underscores the importance of tailoring your offer to the seller’s unique circumstances.

“Winning a bidding war isn’t about the highest bid—it’s about the smartest bid,”

— Sarah Chen, Real Estate Negotiation Expert

By aligning your strategy with the seller’s needs and leveraging tools like escalation clauses judiciously, you transform negotiation from a financial contest into a value-driven collaboration.

FAQ

What are the key financial steps first-time homebuyers should take in 2025 to prepare for the housing market?

First-time homebuyers in 2025 should prioritize building a strong financial foundation by improving their credit score, reducing their debt-to-income ratio, and saving for a down payment. Exploring government-backed programs like FHA loans or state-level down payment assistance can provide additional support. Budgeting for hidden costs, such as property taxes, insurance, and maintenance, ensures long-term affordability. Pre-approval for a mortgage not only clarifies borrowing capacity but also strengthens negotiating power. Leveraging digital tools for financial planning and consulting with HUD-approved housing counselors can further optimize readiness, aligning financial health with the demands of a competitive housing market.

How do rising mortgage rates and housing inventory shortages impact first-time buyers in 2025?

Rising mortgage rates in 2025 elevate monthly payments, reducing affordability for first-time buyers, while inventory shortages limit housing options, intensifying competition. The “lock-in effect,” where existing homeowners retain low-rate mortgages, further constrains supply. This imbalance drives up home prices, forcing buyers to either compromise on property features or explore emerging markets. Leveraging adjustable-rate mortgages (ARMs) or government programs like FHA loans can mitigate affordability challenges. Additionally, understanding regional inventory trends and timing purchases during off-peak seasons can provide strategic advantages. These dynamics underscore the importance of financial preparedness and adaptability in navigating the 2025 housing market.

What government programs and incentives are available for first-time homebuyers in 2025?

Government programs in 2025 offer first-time homebuyers critical support through initiatives like FHA loans, which feature low down payment requirements and flexible credit criteria. USDA loans provide zero-down options for rural buyers, while VA loans cater to veterans with competitive terms. State-level programs, such as California’s CalHFA, offer down payment assistance and forgivable second mortgages. Additionally, federal tax incentives like Mortgage Credit Certificates (MCCs) reduce tax liabilities for eligible buyers. Nonprofit initiatives, including Habitat for Humanity, further enhance affordability. Exploring these programs ensures access to tailored financial benefits, empowering buyers to overcome barriers in a competitive housing market.

How can first-time buyers evaluate energy-efficient homes and their long-term cost benefits in 2025?

Evaluating energy-efficient homes in 2025 involves analyzing features like solar panels, smart thermostats, and high-performance insulation, which reduce utility costs and enhance sustainability. Buyers should request energy audits or certifications, such as ENERGY STAR ratings, to verify efficiency standards. Calculating potential savings through tools like energy cost calculators helps assess long-term benefits. Additionally, understanding local incentives, such as tax credits or rebates for green upgrades, can offset initial costs. Collaborating with real estate agents knowledgeable in sustainable housing ensures informed decisions, aligning environmental priorities with financial goals while boosting resale value in an increasingly eco-conscious market.

What role does remote work play in shaping the best locations for first-time homebuyers in 2025?

Remote work in 2025 redefines prime locations for first-time homebuyers by prioritizing affordability, space, and quality of life over proximity to urban job centers. Suburban and exurban areas, offering lower costs and larger properties, attract remote workers seeking flexible lifestyles. Emerging neighborhoods with robust internet infrastructure and community amenities gain prominence. Buyers should evaluate regional job markets, future growth potential, and commute times for hybrid roles. Tools like location analytics platforms provide insights into property value trends and livability factors. This shift empowers buyers to explore diverse markets, aligning housing choices with evolving work-life dynamics and long-term investment potential.