Tax Loss Harvesting: The Secret Weapon Every Aussie Investor Should Know (But Probably Doesn’t)

Tax Loss Harvesting: The Secret Weapon Every Aussie Investor Should Know (But Probably Doesn’t) In 2022, Australian investors collectively reported over $60 billion in capital losses, according to the Australian Taxation Office (ATO)—a staggering figure that underscores the volatility of modern markets. Yet, hidden within these losses lies a powerful, often underutilized strategy: tax loss harvesting. Far from being a mere accounting trick, this approach transforms financial setbacks into opportunities, allowing investors to offset taxable gains and reduce their overall tax burden. The mechanics of tax loss harvesting are deceptively simple but require precision. By strategically selling underperforming assets, investors can realise losses that directly counterbalance capital gains. However, as Dr. Adrian Raftery, Associate Professor of Taxation at Deakin University, notes, “The timing and intent behind these transactions are critical—missteps can lead to disallowed claims under the ATO’s stringent wash sale rules.” This strategy is particularly potent in Australia’s tax environment, where short-term capital gains are taxed at higher rates than long-term ones. For high-income earners, the difference can mean thousands of dollars saved annually. As markets continue to recover unevenly, tax loss harvesting offers a rare blend of tactical foresight and financial prudence—turning market downturns into a calculated advantage. Image source: milkroad.com Defining Capital Gains and Losses Capital gains and losses are more than just numerical outcomes; they are the financial echoes of strategic decisions. A capital gain occurs when an asset, such as shares or property, is sold for more than its purchase price, while a capital loss arises when the sale price falls short of the original cost. However, the practical application of these definitions in tax loss harvesting reveals a deeper complexity. Timing plays a pivotal role in determining the effectiveness of this strategy. For instance, the Australian Taxation Office (ATO) enforces strict wash sale rules, disallowing losses if an asset is repurchased within a short timeframe. This regulation underscores the importance of aligning tax strategies with portfolio management. As financial analyst Irene Tan explains, “The key is not just identifying losses but ensuring compliance with timing rules to avoid disqualification.” A comparative analysis of asset classes highlights another layer of nuance. While equities often dominate tax loss harvesting discussions, cryptocurrencies present unique challenges due to their volatility and evolving regulatory landscape. For example, during the 2022 market downturn, many Australian investors offset crypto losses against gains in other asset classes, showcasing the strategy’s adaptability. Ultimately, understanding capital gains and losses requires a blend of technical knowledge and strategic foresight, ensuring both immediate tax benefits and long-term portfolio health. Mechanics of Tax Loss Harvesting One of the most intricate aspects of tax loss harvesting lies in maintaining portfolio integrity while adhering to the Australian Taxation Office’s (ATO) stringent wash sale rules. The challenge is not merely in selling underperforming assets but in ensuring that the portfolio’s risk and return profile remains intact during the process. This requires a nuanced understanding of asset substitution and timing. To avoid triggering a wash sale, investors must refrain from repurchasing the same or substantially identical assets within 30 days of the sale. Instead, a common technique involves reinvesting in alternative assets with similar market exposure. For instance, selling shares in a domestic technology ETF at a loss and reinvesting in a global technology ETF can preserve sector exposure while complying with ATO regulations. This approach ensures that the portfolio remains aligned with its strategic objectives without forfeiting the tax benefit. “The key to effective tax loss harvesting is precision—not just in timing but in selecting replacements that align with the investor’s broader financial goals.” — Irene Tan, Financial Analyst However, this strategy is not without its limitations. Market volatility can complicate the timing of trades, and the cost of switching to alternative assets may erode the tax savings. Thus, successful implementation demands a balance between tax efficiency and investment discipline. Australian Taxation Office Regulations The Australian Taxation Office (ATO) enforces a precise framework for tax loss harvesting, designed to prevent exploitation while enabling legitimate tax relief. Central to this framework is the prohibition of wash sales, a practice where investors sell assets at a loss solely to repurchase them shortly after. According to ATO Tax Ruling TR 2008/1, such transactions are disallowed if they fail to create a meaningful change in the investor’s economic exposure. This regulation ensures that tax loss harvesting remains a tool for genuine portfolio management rather than a loophole for tax avoidance. A critical misconception is that capital losses can offset all forms of income. In Australia, capital losses can only be applied against capital gains, not against other income sources like salaries or dividends. However, unused losses can be carried forward indefinitely, offering long-term tax planning opportunities. For instance, an investor who incurred a $15,000 capital loss in 2024 could offset it against a $20,000 capital gain in 2025, reducing their taxable gain to $5,000. The ATO’s rules also emphasize timing. Investors must align their asset sales with the financial year to maximize tax benefits. For example, selling underperforming shares in June rather than July could mean the difference between immediate tax relief and waiting another year. This highlights the importance of strategic planning in tax loss harvesting. By adhering to these regulations, investors can optimize their tax outcomes while maintaining compliance, transforming losses into a calculated advantage. Image source: dubaikhalifas.com ATO Rules on Capital Losses The ATO’s restriction of capital losses to offset only capital gains, while seemingly straightforward, introduces a layer of complexity that demands strategic foresight. This limitation means that losses cannot reduce taxable income from wages or dividends, a common misconception among investors. However, the indefinite carryforward of unused losses offers a unique planning opportunity, particularly for those with fluctuating investment returns. A critical nuance lies in the ATO’s interpretation of intent, especially concerning wash sales. For example, an investor who sells shares at a loss and repurchases them within a short timeframe risks disqualification of the loss if the transaction lacks a genuine economic purpose. The ATO’s sophisticated data

Tax Deductions 101: How to Make the ATO Your New BFF (Spoiler: It’s Not What You Think)

Tax Deductions 101: How to Make the ATO Your New BFF (Spoiler: It’s Not What You Think) In 2023, the Australian Taxation Office (ATO) flagged over $1.5 billion in questionable tax deduction claims, a staggering 20% increase from the previous year. This surge wasn’t driven by corporate giants but by everyday taxpayers misinterpreting the rules. According to Dr. Adrian Sawyer, a taxation law professor at the University of Canterbury, “The complexity of Australia’s tax code often leads individuals to overestimate what they can claim, particularly in areas like home office expenses and travel.” The ATO’s scrutiny has intensified, leveraging AI systems to cross-check deductions against industry benchmarks. For instance, a 2024 audit revealed that 35% of flagged claims for work-related car expenses exceeded allowable thresholds. This shift underscores a critical reality: tax deductions are less about loopholes and more about precision. Understanding these nuances isn’t just compliance—it’s strategy. Image source: adfconsumer.gov.au The Structure of the Australian Tax System Australia’s progressive tax system operates on a deceptively simple principle: the more you earn, the higher your tax rate. But here’s the catch—this structure isn’t just about taxing income; it’s about defining what counts as taxable income after deductions. This distinction is where the real complexity lies. At its core, the system hinges on the relationship between assessable income and allowable deductions. For a deduction to qualify, it must meet strict criteria: the expense must be directly related to earning income, not reimbursed, and substantiated with records. For instance, while a self-employed graphic designer can claim software subscriptions, claiming a portion of their Netflix account for “creative inspiration” would likely fail the ATO’s scrutiny. “The ATO’s focus isn’t on volume but on the integrity of claims. A single, well-documented deduction carries more weight than a dozen vague ones.” — Sarah Chen, Chartered Tax Advisor This precision-driven approach underscores the importance of understanding the system’s nuances. Missteps, even unintentional ones, can lead to audits or penalties, making meticulous record-keeping and professional advice indispensable. How Tax Deductions Work Claiming tax deductions isn’t just about listing expenses—it’s about aligning them with income generation in a way that withstands scrutiny. The ATO’s framework demands that every deduction meet three critical criteria: the expense must directly relate to earning income, not be reimbursed, and be substantiated with records. This triad forms the backbone of compliance, yet its application often reveals hidden complexities. Consider the principle of apportioning expenses. For mixed-use items like a home internet plan, only the business-related portion is deductible. Misjudging this split can lead to over-claims, triggering audits. A 2024 case involving a Melbourne-based consultant highlighted this: their claim for 80% of internet costs was reduced to 40% after the ATO reviewed usage logs. “Precision in apportioning expenses is non-negotiable. It’s not just about compliance—it’s about credibility.” — Dr. Emily Hart, Tax Policy Analyst Ultimately, mastering deductions requires not just adherence to rules but strategic foresight in documentation and justification. Exploring Key Categories of Deductions Work-related expenses, investment deductions, and personal claims form the backbone of tax strategies, yet their nuances often elude even seasoned taxpayers. For instance, while union fees and professional memberships are deductible, claiming them without proper documentation can lead to ATO scrutiny. A 2023 ATO report revealed that 18% of flagged deductions stemmed from insufficient evidence, underscoring the importance of meticulous record-keeping. Investment-related deductions, such as those for rental properties, demand a strategic approach. Did you know that pest control costs and garden maintenance for rental properties are deductible? Yet, many landlords overlook these, leaving potential savings untapped. The ATO estimates that 25% of eligible property owners fail to claim such expenses annually. Misconceptions also abound. A common error is assuming cash expenses without receipts are claimable. The ATO’s data-matching systems, however, can easily flag discrepancies, making accurate documentation non-negotiable. By mastering these categories, taxpayers can transform compliance into a strategic advantage. Image source: patriotsoftware.com Work-Related Expenses Here’s a little-known nuance: the ATO’s focus on work-related expenses isn’t just about receipts—it’s about the narrative your claims tell. Take apportioning expenses, for example. If you use your personal vehicle for work, the ATO allows claims based on a cents-per-kilometre method or actual costs. But here’s the catch: without a detailed logbook, even legitimate claims can fall apart under scrutiny. Consider a case where a marketing consultant claimed 70% of their car expenses. The ATO reduced it to 30% after reviewing their incomplete logbook. Why? The consultant failed to document the purpose of each trip. This highlights the importance of precision in substantiating claims. “The ATO values transparency over assumptions. A well-maintained logbook can be your strongest ally in defending vehicle-related deductions.” — Alex McFarlane, Chartered Tax Advisor To simplify, treat your logbook like a journal: record dates, destinations, and purposes. This approach not only ensures compliance but also strengthens your credibility, turning tax time into an opportunity rather than a challenge. Investment and Personal Deductions Let’s talk about a hidden gem in tax deductions: depreciation on investment property assets. Many landlords overlook this, but it’s a game-changer. Depreciation allows you to claim the wear and tear on items like carpets, appliances, and even the building structure itself. Here’s the kicker: you don’t need to have spent money recently to claim it—these deductions are based on the asset’s original value and lifespan. Why does this matter? Because it’s one of the few deductions that doesn’t require an out-of-pocket expense during the tax year. A detailed depreciation schedule, prepared by a qualified quantity surveyor, can unlock thousands in deductions annually. For example, a Sydney-based property investor reduced their taxable income by $8,000 in one year simply by leveraging a comprehensive schedule. “Depreciation is often misunderstood, but it’s one of the most powerful tools for property investors to maximize returns.” — Sarah Blake, Certified Property Tax Specialist The takeaway? Don’t underestimate the value of professional advice and meticulous documentation. It’s the difference between leaving money on the table and optimizing your tax strategy. Common Misconceptions About Deductions Here’s a surprising truth: not all

5 Australian Property Tax Loopholes That Could Save You Thousands

5 Australian Property Tax Loopholes That Could Save You Thousands In a nation where property is as much a cultural obsession as it is an investment strategy, the tax system holds secrets that could transform your financial landscape. Surprisingly, while many Australians grapple with rising costs, a handful of overlooked property tax loopholes quietly offer substantial savings. Why do these opportunities remain underutilized? Are they hidden in plain sight, or simply misunderstood? As we unravel these strategies, the broader question emerges: how can you turn the tax code into your greatest ally? Foundations of Capital Gains Tax (CGT) in Australia The true complexity of CGT lies in its interplay with ownership structures. For instance, holding property through a discretionary trust can redistribute gains to beneficiaries in lower tax brackets, significantly reducing liabilities. Yet, this strategy demands precision—missteps in trust deeds or timing can nullify benefits. Additionally, the 50% CGT discount for assets held over 12 months rewards long-term planning, but few consider how offsetting capital losses amplifies this advantage. These nuances redefine CGT as a tool, not a burden. The Importance of Minimizing Property Tax Liabilities Strategic use of negative gearing not only offsets rental property losses against taxable income but can also push investors into lower tax brackets, compounding savings. However, timing is critical—aligning deductions with high-income years maximises impact. Beyond this, leveraging state-specific exemptions, such as principal place of residence concessions, can significantly reduce liabilities. These approaches, when paired with meticulous record-keeping and proactive planning, highlight how property tax minimisation is less about avoidance and more about optimising financial outcomes for long-term growth. The Main Residence Exemption The main residence exemption offers a powerful shield against capital gains tax, but its nuances often go unnoticed. For instance, the six-year rule allows homeowners to rent out their property without forfeiting the exemption, provided they don’t claim another main residence. A case study revealed one investor saved over $50,000 by leveraging this rule strategically. Misconceptions, such as needing continuous occupancy, persist. By understanding these subtleties, homeowners can unlock significant savings while maintaining compliance with ATO regulations. Qualifying Criteria and Key Benefits A lesser-known factor influencing eligibility is the land size limit of 2 hectares. Properties exceeding this threshold may still qualify for a partial exemption, calculated proportionally. For example, a rural homeowner reduced their CGT liability by isolating the exempt portion of their land. Additionally, the exemption’s flexibility extends to properties used for income generation, such as Airbnb, provided meticulous records delineate personal and business use. These nuances underscore the importance of tailored strategies to maximise benefits while ensuring compliance. Exploring the Extended Six-Year Rule The six-year rule’s flexibility allows homeowners to reset the exemption clock by reoccupying their property, even briefly. For instance, an investor who rented out their home for five years returned for six months before relocating again, effectively restarting the six-year exemption period. This approach, while entirely legal, requires precise timing and documentation to avoid disputes with the ATO. By leveraging this strategy, property owners can extend tax benefits indefinitely, offering a dynamic tool for long-term financial planning. The 12-Month Ownership Discount The 12-month ownership discount rewards long-term property investment by halving CGT liability for assets held over a year. Misunderstanding the timing—measured from contract dates, not settlement—can disqualify investors. For example, selling a property just days shy of the 12-month mark cost one investor $20,000 in additional tax. This rule also intersects with estate planning; inherited properties may qualify based on the deceased’s ownership period. Strategic timing and expert advice ensure maximum savings while avoiding costly errors. Image source: gotocourt.com.au Calculating Your Discounted CGT Accurate CGT calculations hinge on understanding the cost base. Beyond purchase price, include expenses like legal fees, stamp duty, and capital improvements. For instance, a $10,000 renovation can significantly reduce taxable gains. Missteps, such as omitting deductible costs, inflate liabilities unnecessarily. Additionally, offsetting capital losses against gains before applying the 50% discount amplifies savings. Leveraging digital tools for meticulous record-keeping ensures compliance and precision. As property values rise, proactive planning transforms CGT from a burden into a strategic advantage. Common Pitfalls and Best Practices A frequent pitfall is misjudging the CGT event date, which is tied to contract signing, not settlement. For example, rushing a sale to meet financial deadlines can inadvertently disqualify the 12-month discount. Best practices include aligning sales with tax planning cycles and leveraging professional advice to navigate timing complexities. Additionally, consider the impact of joint ownership structures, as splitting gains between co-owners in different tax brackets can optimise outcomes. Precision and foresight are key to avoiding costly errors and maximising benefits. Increasing the Cost Base Expanding the cost base beyond the purchase price is a powerful yet underutilized strategy. Costs like legal fees, stamp duty, and renovations directly reduce taxable gains. For instance, a $15,000 kitchen upgrade not only boosts property value but also offsets CGT. Misconceptions arise when investors overlook holding costs, such as council rates, which may qualify under specific conditions. Expert advice ensures compliance while maximising deductions, transforming overlooked expenses into strategic tools for long-term tax efficiency and financial growth. Image source: australiainstitute.org.au Eligible Expenses and Adjustments One overlooked adjustment is the inclusion of non-deductible ownership costs, such as council rates and loan interest during non-income-generating periods. For example, a property initially used as a main residence can have these costs added to its cost base when later rented. This nuanced approach reduces taxable gains significantly. Additionally, title defense costs, often ignored, can qualify if tied to ownership disputes. Leveraging these adjustments requires meticulous record-keeping, offering a proactive framework for optimising CGT outcomes while ensuring compliance. Practical Examples of Cost Base Enhancement Consider a property owner who added $20,000 in solar panels. While boosting market appeal, this expense also qualifies as a capital improvement, directly increasing the cost base and reducing CGT. Lesser-known factors, like reclassifying landscaping as a structural improvement, can further amplify benefits. Additionally, costs tied to rezoning applications—often dismissed—may qualify under title preservation. These strategies highlight the importance of expert

Don’t Miss Out: How to Prepare Your Tax Return as a Smart Rental Property Investor

How to Prepare Your Tax Return as a Rental Property Owner Owning a rental property can be a lucrative venture. However, it also comes with its fair share of responsibilities, one of which is tax preparation. Understanding rental property tax preparation is crucial for every property owner. It ensures compliance with tax laws and helps maximize your returns. This guide aims to simplify the process of preparing your tax return as a rental property owner. It will provide a step-by-step guide on how to handle rental income taxes, ATO tax returns, and more. We’ll delve into common rental property deductions and the ATO Depreciation Schedule. These are key aspects that can significantly reduce your taxable income. Whether you’re a seasoned landlord or just starting, this guide will equip you with the knowledge you need. So, let’s dive in and demystify rental property tax preparation. Understanding Rental Property Tax Basics Diving into rental property taxes can be daunting, but knowing the essentials makes it manageable. Rental income is taxable and must be reported to ensure compliance with tax laws. The foundation of rental property tax preparation lies in understanding what counts as taxable income. Rental income encompasses not only rent but also other payments like fees for services. Importantly, landlords can claim expenses incurred while maintaining their rental property. These deductible expenses can include mortgage interest, property taxes, and insurance premiums. Understanding the distinction between short-term and long-term rentals is crucial. Short-term rental income might incur additional scrutiny or tax implications in some jurisdictions. To manage your rental property taxes effectively, consider these key points: Taxable Income: Rent, services, and certain fees. Deductible Expenses: Maintenance, insurance, and mortgage interest. Rental Types: Differentiating between short-term and long-term rentals. Knowing and applying these basics can prevent costly mistakes and optimize your financial outcomes. For intricate cases like multiple properties or foreign holdings, deeper knowledge is invaluable. Being well-informed empowers property owners to enhance their tax strategies each year. Accessing professional advice can also optimize your understanding of complex rental income taxes. Organizing Your Documentation Properly organizing your documentation is key to successful rental property tax preparation. This not only simplifies the tax filing process but also ensures compliance. Start by maintaining clear and accurate records of all rental income. Having organized records helps in quickly verifying amounts and sources if needed later. It’s equally important to document expenses related to your rental property. Keep receipts and invoices for maintenance, utilities, and property management fees. You should also maintain a log of dates and activities for any repairs or improvements. Documenting these actions can support claims for deductions during tax filing. Consider organizing your documents using these categories: Income Records: Rent payments, fee collections. Expense Receipts: Maintenance, insurance, and management fees. Repair Logs: Date, description, and cost of repairs. Regularly updating your records helps you stay on top of tax obligations. This preparation prevents last-minute scrambles and enhances accuracy in your tax returns. Reporting Rental Income Accurately Accurate reporting of rental income is essential for compliance with tax laws. Misreporting could lead to penalties or audits. Begin by identifying all sources of rental income. This includes not only regular rent payments but also late fees, lease cancellation fees, and any services you charge for. Each type of income needs to be correctly categorized. Doing so ensures they are properly reported on your tax returns and not overlooked. Ensure you accurately report any advance rent payments in the tax year you received them. This includes payments for future rental periods. Consider the following when reporting your rental income: Regular Rent Payments: Monthly or weekly rent income. Late Fees: Additional charges for overdue payments. Lease Cancellation Fees: Income from terminated leases. Keep detailed records of all these payments and cross-check them with bank deposits. Using accounting software can simplify tracking and reconciliation. Maximizing Rental Property Deductions Effectively managing rental property deductions can greatly decrease your taxable income. It helps optimize financial returns on your investment. Understanding which deductions you’re eligible for is key. Common expenses include mortgage interest, property taxes, and insurance costs. Proper categorization of expenses is crucial. This ensures you claim the full range of available deductions come tax time. Keep detailed records of all maintenance and repair work. These can often be claimed as immediate deductions, saving you money in the short term. Additionally, understanding how capital improvements differ from repairs is beneficial. Only repairs can be deducted immediately. Consider maintaining a comprehensive log throughout the year. This might include receipts, bills, and any correspondence related to property expenses. Here’s a quick list of potential deductible expenses: Mortgage interest and property taxes Home office expenses (if applicable) Advertising for tenants Consistently reviewing and updating your records allows you to fully maximize your deductions. Consider using accounting software to streamline this process. It can ensure no expense is overlooked or misclassified. Common Deductible Expenses A broad range of expenses can be deducted. These deductions help lower your rental income taxes. Each expense category can contribute to significant tax savings. Some are deductible in the year incurred, while others are depreciated over time. Here’s a quick rundown of common deductible expenses: Maintenance and Repairs: Immediate fixes and upkeep tasks. Insurance: Policies covering rental properties, excluding personal coverage. Utilities: Costs the landlord pays (electricity, water). Keep proper documentation for each expense to justify your deductions to the tax authorities. This can include invoices, receipts, or bank statements. Understanding the ATO Depreciation Schedule The ATO Depreciation Schedule is vital for rental property tax preparation. It determines the depreciation you can claim on your property over time. Depreciation spreads out the deduction of significant expenses across several years. This applies to items like appliances or structural improvements. Each asset category has specific guidelines. Familiarize yourself with these to correctly categorize your assets. Review the ATO’s schedule to identify what assets and improvements qualify. For example, carpets or blinds can depreciate over a different period than kitchen appliances. Consider separating assets into two classes: capital works (structural additions)

Property Investors Ultimate Guide to Lodging Tax Returns Like a Pro

Complete Guide to Lodging Tax Returns for Property Investors Navigating the tax landscape can be daunting, especially for property investors. Understanding how to properly lodge your tax returns is essential to ensuring compliance and maximizing your financial benefits. The complexity of tax laws and regulations can create confusion, leading to potential errors or missed opportunities for savings. In this guide, we’ll break down everything you need to know about rental property taxes and how to successfully lodge your tax returns, providing you with clarity and confidence in managing your investments. Understanding the intricacies of tax obligations not only keeps you compliant but also uncovers opportunities to optimize your returns. By delving into the specifics of rental property taxes, you can strategically plan your investments and manage your finances effectively. Whether you’re a seasoned investor or new to property ownership, this comprehensive guide will help you navigate the complexities of tax returns with ease and precision. Understanding Rental Property Taxes Rental property taxes can vary based on location, type of property, and income generated. Familiarizing yourself with the basics will help you manage your investment effectively. Each jurisdiction may have different tax rates and rules, making it crucial to understand the specific regulations that apply to your properties. Knowledge of these nuances ensures that you remain compliant and avoid unnecessary penalties. Understanding the tax landscape of your rental properties also allows you to plan financially and strategically. By knowing what taxes you are liable for, you can budget more accurately and make informed decisions about potential property investments. This foresight can significantly impact your investment strategy and overall financial health. Types of Rental Property Income Rental property income typically includes several streams, each of which needs to be accurately reported for tax purposes: Rental payments: The primary source of income from tenants. This includes all regular rental payments made by tenants, which form the bulk of your property income. Security deposits: Any deposits kept for damages or unpaid rent. While typically not considered income, any portion retained for damages or breaches must be reported. Other income: Fees for services like laundry or parking spaces. Additional services provided to tenants can generate income, which must be included in your tax calculations. Understanding these income streams is critical for accurate tax reporting. Each category may have different tax implications, and misreporting can lead to audits or penalties. Maintaining detailed records of all income sources ensures transparency and accuracy in your tax returns. Tax Deductions for Property Investors Property investors can benefit from various tax deductions, which can significantly reduce taxable income. Some common deductions include: Mortgage interest: Interest paid on loans taken to purchase the property. This can often be one of the largest deductions available to property investors. Property taxes: Taxes paid to local governments. These are typically deductible, reducing the overall tax burden on your investment. Operating expenses: Costs like repairs, maintenance, and utilities. Regularly incurred expenses necessary for the upkeep of the property are deductible. Depreciation: A non-cash deduction reflecting the property’s wear and tear over time. This powerful deduction accounts for the gradual decline in property value due to usage and aging. Maximizing these deductions requires diligent record-keeping and awareness of applicable laws. Staying informed about changes in tax legislation can enhance your ability to claim all eligible deductions. This proactive approach not only reduces your tax liability but also enhances the profitability of your property investments. Lodging Your Tax Return Lodging a tax return involves several steps. Here’s a streamlined process to guide you: Step 1: Gather Your Documents Organize all relevant documents before starting the process. These may include: Rental income statements: Detailed records of all rental income received during the tax year. Mortgage and loan statements: Documents showing interest payments and outstanding loan amounts. Receipts for property expenses: Proof of payments for repairs, maintenance, and other deductibles. Property tax statements: Official documents from local authorities detailing property tax payments. Previous tax returns: Past filings can provide a reference and help ensure consistency and accuracy in your current return. Having these documents ready will make the process smoother. Proper organization reduces the likelihood of errors and ensures you claim all eligible deductions. This preparation also saves time and effort when filing your return. Step 2: Calculate Your Income and Deductions Accurate calculation is crucial. Sum up all rental income and subtract allowable deductions to determine your net rental income. This figure will form the basis of your tax return. Ensuring precision in these calculations is vital to avoid overpaying or underpaying your taxes. Utilizing spreadsheets or accounting software can facilitate this process, providing clarity and precision. By accurately calculating your net rental income, you can better anticipate your tax liabilities and plan your finances accordingly. Step 3: Use Tax Software or Hire a Professional Depending on your comfort level, you can either use tax software or hire a professional tax preparer. Software can be cost-effective and user-friendly, providing step-by-step guidance to complete your return accurately. However, tax professionals offer personalized advice and can handle complex situations, ensuring compliance and optimizing your tax strategy. Choosing the right method depends on the complexity of your tax situation and your personal preference. While software provides convenience, professionals offer expertise that can be invaluable, especially for complex or large-scale property portfolios. Step 4: Lodge Your Return Once your calculations are complete, lodge your tax return through the appropriate channels. This might be through an online tax portal or via a paper return, depending on your jurisdiction. Ensure that all information is complete and accurate before submission to avoid delays or penalties. Timely filing is essential to avoid late fees and interest charges. Understanding the deadlines and requirements specific to your jurisdiction ensures compliance and minimizes stress during tax season. Common Mistakes to Avoid Even seasoned investors can make mistakes. Here are a few common pitfalls: Overlooking Deductions Missing out on available deductions can lead to higher tax liabilities. Ensure you account for all eligible expenses. Regularly reviewing your expenses and

Save Big in 2025: How to Accurately Calculate Depreciation for Your Properties

Calculate Depreciation for Investment Properties in 2025 Understanding how to calculate depreciation for investment properties is crucial for any real estate investor. It’s a key aspect of maximizing your tax benefits and making informed decisions about your property investments. Depreciation can offset taxable income from your properties. But how does it work? And how can you calculate it accurately? This guide will provide a comprehensive overview of investment property depreciation. We’ll delve into the ATO Depreciation Schedule and the nuances of real estate depreciation. We’ll also explore the impact of the 2025 tax laws on property depreciation. This information will be particularly relevant for Australian property investors. By the end of this guide, you’ll have a clear understanding of how to calculate depreciation for your investment properties. You’ll be equipped with the knowledge to maximize your tax benefits and make smarter investment decisions. Understanding Investment Property Depreciation Investment property depreciation is a tax deduction available to property investors. It accounts for the gradual loss of value of your property’s structure and its contents. The importance of real estate depreciation lies in its ability to reduce taxable income. This allows investors to save money on taxes and improve overall cash flow. Depreciation is divided into two main categories: capital works deductions and plant and equipment depreciation. Each has specific eligible items and methods for calculation. The Australian Tax Office (ATO) establishes guidelines for property depreciation. This includes defining the life span of assets and outlining eligible deductions. Understanding the nuances of these categories is essential. It ensures you claim the maximum allowable deductions without errors. Depreciation must be calculated accurately to fully benefit from it. This often involves detailed knowledge of tax laws and property evaluations. The Importance of ATO Depreciation Schedules The Australian Tax Office (ATO) provides a comprehensive Depreciation Schedule. It serves as a vital tool for investment property owners in navigating complex tax deductions. This schedule outlines the eligible assets and their effective life. It determines how much you can deduct from your taxable income each year. Using the ATO Depreciation Schedule ensures compliance with Australian tax laws. It helps avoid penalties and maximizes your depreciation claims accurately. Investors often rely on this schedule to plan long-term financial strategies. It provides clarity on what depreciation benefits to expect over time. Understanding and using the ATO schedule can lead to substantial tax savings. It ultimately enhances the profitability of your investment property portfolio. Capital Works vs. Plant and Equipment Depreciation Depreciation for investment properties involves two main categories. These are capital works deductions and plant and equipment depreciation. Understanding the difference between them is crucial. Capital works deductions relate to the building structure and permanent assets. These include elements like walls, floors, and fixed installations. They are subject to a specific set of rules for claiming depreciation. On the other hand, plant and equipment refer to removable or mechanical items. This category covers things like appliances, carpets, and fixtures. Each item has its own effective life for depreciation purposes. The depreciation rate for capital works is generally fixed. Typically, it applies at 2.5% per year over 40 years. This rate covers construction expenses after a certain date. For plant and equipment, depreciation depends on the asset’s effective life. Owners can choose between methods such as diminishing value or prime cost. Each approach yields different outcomes for deductions. Differentiating between these categories can greatly affect your tax strategy. It allows investors to maximize benefits by claiming all available deductions. Using expert help may simplify complex scenarios and ensure full compliance. Methods of Calculating Depreciation The Diminishing Value Method The diminishing value method calculates depreciation by assuming an asset loses value more rapidly in the early years. This method can be beneficial for properties with items that depreciate quickly. Investors can claim higher deductions in the initial years of the asset’s life. Under this method, the depreciation expense is calculated annually. It is determined by applying a fixed percentage to the asset’s depreciated value. This percentage is based on the asset’s effective life and is typically higher than that for the prime cost method. The advantage of this approach is that it allows for larger tax deductions upfront. This can improve cash flow in the early years of property ownership. However, deductions will decrease over time as the asset depreciates. The diminishing value method is often suitable for technology or equipment that quickly becomes obsolete. Always ensure that the selected method aligns with your overall financial strategy. The Prime Cost Method The prime cost method spreads depreciation evenly over the asset’s useful life. It calculates the depreciation expense based on the original cost of the asset. This results in a consistent deduction amount each year. This method is straightforward and provides predictable yearly deductions. For assets like buildings with longer effective lives, the prime cost method can offer stability. It suits investors who prefer steady, equal deductions over variable amounts. With this method, the rate of depreciation is determined by the asset’s effective life. The calculation remains constant, ensuring systematic financial planning. It often aligns well with long-term property investment strategies. Choosing the prime cost method simplifies budgeting and projections. This stability can be appealing, especially for managing longer-term investments. As with any method, evaluate it in the context of your tax situation. Understanding each method’s nuances helps in making an informed choice. The decision can significantly impact cash flow and long-term financial benefits. Consulting with a tax professional can provide valuable insight tailored to your needs. Step-by-Step Guide to Calculate Depreciation for Investment Properties Calculating depreciation on investment properties requires understanding several key steps. This process can maximize your tax benefits significantly. Here’s a step-by-step guide to help you navigate through it. Start by identifying what items are eligible for depreciation. These typically include buildings and equipment within your property. Eligibility will vary, so it’s crucial to verify with the latest tax guidelines. Next, determine the construction date of the property or improvements. This date is essential because it

Maximise Your Investment: The Ultimate Guide to Property Depreciation Schedules in Australia

Ultimate Guide to Property Depreciation Schedules in Australia Property investment in Australia can be a lucrative venture. However, to truly maximize your returns, understanding property depreciation is crucial. Property depreciation schedules are a key tool for investors. They provide a roadmap for claiming tax deductions over the life of your investment property. But what exactly is property depreciation? And how does it benefit Australian property investors? This guide will delve into these questions. It will provide a comprehensive overview of property depreciation schedules in Australia. From understanding the types of depreciation to creating your own schedule, this guide has you covered. Let’s unlock the potential of property depreciation together. Understanding Property Depreciation in Australia Property depreciation is the process of accounting for the wear and tear of a building and its assets over time. In Australia, property investors can claim depreciation as a tax deduction, reducing taxable income. There are two types of depreciation: capital works and plant and equipment. Each type offers unique benefits and is calculated differently. Capital works refer to the construction costs of the building itself. Plant and equipment cover the removable items within the property. Investors must understand depreciation to maximize tax returns. By doing so, they can significantly improve the cash flow from their investment property. Here’s how property depreciation can benefit you as an investor: Reduces taxable income Increases return on investment Provides long-term savings Properly utilizing depreciation schedules can transform your investment strategy. It can potentially turn a passive investment into a highly profitable one. What is Property Depreciation? Property depreciation refers to the decrease in value of a property’s assets over time. Buildings deteriorate, and items within them lose value. Australian tax law allows owners to claim this depreciation as a tax deduction. This can be a powerful tool to offset taxable income. The concept applies to both new and existing properties. However, the actual deductions will vary based on asset type and effective life. Why is Property Depreciation Important for Investors? For investors, property depreciation provides an opportunity to maximize tax savings. By reducing taxable income, investors can improve their cash flow. This increase in cash flow makes it easier to manage expenses associated with investment properties. It may even allow for reinvestment into additional properties. Moreover, depreciation deductions can also play a role in investment strategy. They contribute to a portfolio’s overall financial health, offering benefits beyond simple tax savings. Types of Property Depreciation Understanding the types of property depreciation is key for maximizing tax benefits. In Australia, there are two primary types: capital works deductions and plant and equipment depreciation. Capital Works Deductions cover the structural elements. This includes the building itself, walls, and fixed items like plumbing. Plant and Equipment Depreciation involves assets that are removable or mechanical. Examples include air conditioning units and furniture. Both types offer valuable deductions. However, the method of calculation differs. When planning your investment strategy, consider the potential deductions from both types. This can greatly affect cash flow and investment returns. Key elements to remember about depreciation: Capital works: structural, fixed Plant and equipment: removable, mechanical Different calculation methods Combining these elements effectively can unlock significant financial benefits. It enables investors to reduce tax liabilities and improve profitability. Capital Works Deductions Capital works deductions apply to the structural aspects of a property. This includes the bricks, mortar, and roof of the building. These deductions are available for properties built after a certain date. For residential properties, this date is typically July 1, 1985. Investors can claim these deductions at a rate of 2.5% per annum. The deduction period can last up to 40 years, depending on the property’s age. Plant and Equipment Depreciation Plant and equipment depreciation refers to the wear and tear of removable items. These can include appliances, carpets, and even blinds. These items are typically depreciated over a shorter period compared to capital works. The effective life of the asset determines its rate. For these deductions, items are categorized as either low-value or high-value. Low-value items can be written off more quickly, enhancing tax benefits immediately. Eligibility and Compliance Determining eligibility for property depreciation is crucial. Not everyone can claim these valuable deductions. Australian property owners must adhere to specific criteria to qualify. This ensures compliance with tax regulations and optimizes deductions. Eligibility depends on property type, construction date, and ownership status. These factors determine the deductions available to investors. Engaging a professional can aid in verifying eligibility and maximizing benefits. They ensure that all deductions are claimed and nothing is missed. Here’s a brief eligibility checklist: Ownership: Must be the property owner or responsible for wear and tear Construction date: Usually after July 1, 1985, for capital works Property type: Must produce income, like rental properties Who is Eligible for Property Depreciation? To claim property depreciation, the property must generate income. This usually means it’s an investment property. Another important factor is ownership. Only the property’s owner can claim depreciation deductions. For capital works, the property should have been built or refurbished after specific dates. This impacts the eligibility for such deductions. ATO Compliance and the Role of Quantity Surveyors Compliance with the Australian Taxation Office (ATO) is essential. Proper documentation and adherence to rules are mandatory. A qualified quantity surveyor plays a significant role. They provide the expertise needed to prepare accurate depreciation schedules. These professionals assess property assets. They help in producing a report that’s compliant with ATO standards. Consulting a quantity surveyor ensures no deductions are overlooked. Their input can be invaluable for maximizing tax returns. Creating Your Property Depreciation Schedule Creating a property depreciation schedule is a key step for any investor. The process can initially seem complex, but it’s manageable with the right approach. The first step is to organize a detailed property assessment. This typically involves a site inspection by a qualified quantity surveyor. After the inspection, all depreciable assets are identified. This includes both capital works and plant and equipment items. Next, a comprehensive report is prepared. This report

Stage 3 Tax Cuts: Transforming the Australian Housing Market – Opportunity or Risk for Property Investors?

Stage 3 Tax Cuts A Boon or a Bane for the Australian Housing Market The upcoming stage 3 tax cuts in Australia have sparked a lively debate. Will they be a boon or a bane for the Australian housing market? These tax cuts, scheduled for 2025, aim to reduce the tax burden for middle to high-income earners. The potential increase in disposable income could significantly impact consumer spending. One sector that could be heavily influenced is the housing market. Property prices, rental yields, and housing demand may all be affected. This article will delve into the potential impacts of these tax cuts on the Australian housing market. We’ll explore the arguments for and against, providing a balanced view on this hot topic. Stay tuned as we navigate the complex interplay between tax policy and the housing market. Understanding Stage 3 Tax Cuts in Australia The stage 3 tax cuts are a significant part of Australia’s tax reform agenda. Introduced as a plan to simplify the tax system, these cuts aim to benefit middle and high-income earners by reducing personal income tax rates. This change is designed to boost consumer spending, which can bolster the economy. Implementing these tax cuts involves changes to the existing tax brackets and rates. The journey to stage 3 didn’t happen overnight. It followed the earlier phases of tax reform, each with distinct goals and impacts. Let’s take a closer look at each phase. What Are Stage 3 Tax Cuts? Stage 3 tax cuts will be implemented in 2025, continuing a series of reforms to Australia’s tax system. They aim to simplify the income tax brackets and reduce tax rates for certain taxpayers. The idea is to incentivize work, increase take-home pay, and streamline the tax process for many Australians. By doing so, these cuts hope to spur economic activity and growth. The Timeline: From Stage 1 to Stage 3 The pathway to stage 3 began with stage 1, introduced in 2018, which offered immediate tax relief to low and middle-income earners. Stage 2 followed in 2020, accelerating planned cuts and adjusting thresholds. As stage 3 approaches, the focus shifts towards a flatter and simpler tax structure. The progression through these stages reflects evolving economic priorities and responses to changing fiscal conditions. The Proposed Changes to Tax Brackets and Rates Stage 3 proposes significant adjustments in tax brackets, mainly for upper-income thresholds. The highest tax bracket will start at $200,000, rather than the current $180,000. Taxpayers earning from $45,000 to $200,000 will be taxed at a flat rate of 30%. This change eliminates the 37% tax bracket entirely, aiming for a more streamlined system. The restructuring is expected to benefit around 95% of taxpayers. The Fiscal Impact and Economic Implications The introduction of stage 3 tax cuts is anticipated to have substantial fiscal consequences for the Australian government. As personal tax revenues decrease due to lower rates, the government must address the resultant budgetary shortfall. This potential loss in revenue invites discussions about how public services and infrastructure spending might be affected. Projected Government Budget Changes Implementing stage 3 tax cuts entails a significant reduction in government tax revenue. The potential revenue loss could reach billions annually. This decrease necessitates adjustments in federal budgeting to ensure fiscal balance. Policymakers might explore new revenue sources, or they may need to reallocate funds from existing projects. The potential effects on public service funding are a central concern in this discourse. Disposable Income and Consumer Spending With additional disposable income due to lower taxes, households may choose to increase their spending. This can invigorate the economy by boosting demand for goods and services. Yet, increased disposable income could also lead to higher consumer debt if not managed wisely. The resulting economic boost hinges on whether households decide to spend, save, or invest the surplus funds. Economic Growth vs. Income Inequality While tax cuts can spur growth, they might also widen the wealth gap. Higher earners disproportionately benefit from these tax reforms, potentially exacerbating income inequality. The debate centers on whether economic growth can offset these disparities. As incomes rise, it’s crucial to ensure that wealth distribution remains equitable. Critics argue that without additional measures, these cuts could deepen societal divides. Balancing growth with fairness is a critical challenge in evaluating stage 3’s broader impacts. The interplay between these elements highlights the complexity of the tax cuts’ influence on the economy. The intricate dynamics require a careful approach to maximize benefits while mitigating potential downsides. The Stage 3 Tax Cuts and the Australian Housing Market The stage 3 tax cuts are poised to affect the Australian housing market significantly. With more disposable income, individuals might consider investing in real estate. As such, understanding these tax cuts’ potential impacts on property values, demand, and rental markets is crucial. Potential Effects on Property Prices Property prices might rise as stage 3 tax cuts are introduced. Increased disposable income could lead to more Australians entering the housing market. This influx of buyers can drive competition, pushing property values higher. Additionally, with more capital available, existing homeowners might also upgrade, spurring further demand and price escalation. The tax cuts could thus spark a surge in housing transactions and valuations. Housing Demand and Investment A boost in disposable income can heighten housing demand and attract new investors. Many Australians could view property investment as a viable avenue to grow wealth. This trend might lead to a surge in housing purchases, not just for residential purposes but also as investment assets. As more investors jump in, the market could see both diversification and specialization. Such dynamics might drive regional housing projects and boost construction activity. Rental Market and Yields The rental market might experience fluctuations due to these tax cuts. With more buyers entering the homeownership realm, rental demand could decline slightly. However, if property prices surge, some might stay renters longer, supporting rental demand. This dual effect could influence rental yields positively or negatively. Investors will need to gauge how these elements balance out

Get Rich or Taxed Trying? A Fun Guide to Capital Gains on Investment Property

Understanding Capital Gains on Investment Property: A Game of Profit or Penalty? Capital gains on investment property can be the ultimate reward—or a surprising cost—depending on how well you play the game. Imagine selling a property at the peak of the market and reaping a handsome profit. But beware, every dollar you make in profit could mean an extra dollar owed in taxes. The stakes are high, but with the right strategy, your gains can far outweigh the tax bite. So, what exactly are capital gains on investment property, and why should investors care? Capital gains represent the profit you pocket when selling a property for more than you paid. While it sounds straightforward, there’s a catch: those gains can come with a hefty tax bill. Knowing when and how capital gains tax kicks in is key to maximizing profit and staying ahead in the investment game. Timing your sale isn’t just luck—it’s strategy. The moment you sell your property, the tax clock starts ticking. Holding on for the long term might just be your ticket to lower tax rates, thanks to discounts on capital gains for properties held over 12 months. But short-term holds? They can trigger higher taxes, making it essential to consider timing in your investment approach. Luckily, there are clever ways to lighten your tax load. With the right mix of tax deductions and exemptions, you can reduce the impact of capital gains on investment property. From recording renovation expenses to utilizing tax-free thresholds, these strategies can help investors keep more of their hard-earned profits while staying tax compliant. In the game of capital gains, the goal is simple: maximize profit, minimize taxes. But getting there requires knowledge and strategy. Understanding the nuances of capital gains on investment property—when to sell, what to claim, and how to plan—puts you in control. So, are you ready to play the game wisely? With the right moves, you can make capital gains work for you, not against you. The Basics: What Exactly Are Capital Gains (And Why Should You Care)? Capital gains on investment property are a key element in the world of real estate profits, and they’re often the reason many investors jump into property. In the simplest terms, capital gains are the profits you earn from selling a property for more than you originally paid. But there’s more to it than just buying low and selling high. Understanding these gains can reveal ways to maximize your returns while managing your tax obligations. Why should you care about capital gains on investment property? Because these profits are the difference between a smart investment and a missed opportunity. Without the right insights, you might find your gains eroded by unexpected taxes. By getting a handle on how capital gains work, you can set yourself up to make informed choices and avoid costly surprises when it’s time to sell. Think of capital gains as a reward for your investment acumen, but with a catch: the government takes a share. The tax on capital gains can impact how much you keep from your sale, making it crucial to understand when and how these taxes apply. Knowing the basics helps you plan smarter, so your profits stay yours, not the taxman’s. There’s a strategy in timing, too. Capital gains on investment property may be taxed differently based on how long you hold the property. For assets held over a year, many investors are eligible for a reduced tax rate—a move that can save significant cash. So, the longer you hold, the better your potential tax break could be, making it worth the wait. In the end, capital gains on investment property are all about leveraging the right moves for maximum profit. With a clear understanding of the basics, you’ll be ready to play the property game with skill, keeping more of your hard-earned gains where they belong—in your pocket. So, why care? Because these gains could be your ticket to wealth if you manage them wisely. Timing is Everything: When Does Capital Gains Tax Apply? When it comes to capital gains on investment property, timing is everything. The moment you decide to sell can have a big impact on how much you owe in capital gains tax. Sell too soon, and you might find yourself hit with a higher tax rate. But wait for the right moment, and you could keep more of your profits. Knowing when capital gains tax applies is the first step in mastering the timing game. Capital gains tax kicks in the instant your investment property sells for more than you paid. This “gain” is what the tax authorities are interested in, and they’ll take their share based on when the sale happens. If you’re in a rush to sell, you might pay more. But with a little patience, you could unlock discounts that reward long-term investment. Holding onto your property for over a year? You’re in luck! Many investors enjoy a reduced tax rate on capital gains for properties held longer than 12 months. This is known as the “long-term capital gains discount,” and it’s a game-changer. By simply holding off on selling, you could save a significant chunk in taxes—making timing your secret weapon. However, short-term holds can be tempting, especially in a hot market. But selling in less than a year means paying full capital gains tax without any discounts. If you’re looking to maximize your profits, it’s worth weighing the cost of a quick sale against the savings of a well-timed exit. Sometimes, the best move is to play the waiting game. Ultimately, capital gains on investment property come down to timing your sale for the best tax outcome. The right timing can make or break your profit potential, so knowing when capital gains tax applies empowers you to plan smarter. After all, in the world of property investment, a little patience can go a long way toward keeping more of your hard-earned gains in your own pocket. Deductions and Discounts: How to

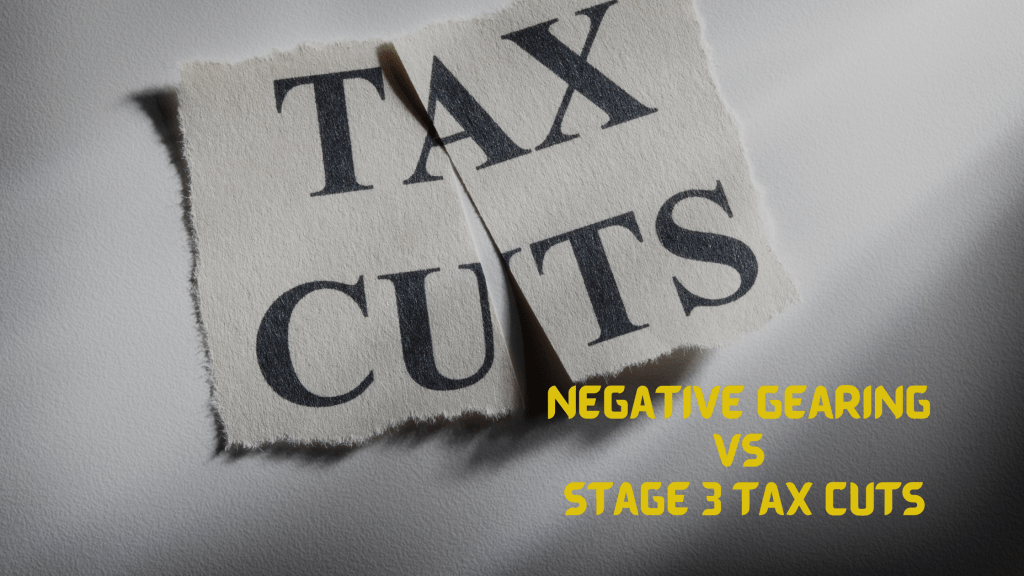

Tax Breaks That Matter: Are Stage 3 Tax Cuts Better Than Negative Gearing for Investors?

Stage 3 Tax Cuts vs. Negative Gearing: What’s More Beneficial for Property Investors? Navigating the world of property investment can be complex. Especially when it comes to understanding the financial implications of different tax strategies. In Australia, two key considerations are Stage 3 tax cuts and negative gearing. Both have potential benefits for property investors, but which is more advantageous? Negative gearing allows investors to deduct property investment losses from their taxable income. It’s a strategy that’s been part of the Australian property market for decades. On the other hand, Stage 3 tax cuts aim to reduce personal income tax rates. This could increase disposable income, potentially stimulating economic growth and affecting the property market. In this article, we’ll delve into the details of both strategies. We’ll compare their benefits, helping you make informed decisions about your investment strategies. Understanding Negative Gearing Negative gearing occurs when the expenses on a property surpass the rental income it generates. This loss can then be subtracted from the investor’s total taxable income, effectively reducing tax liabilities. Australia’s property market has long been influenced by negative gearing. In the 1980s, it was adopted to encourage property investment and has since remained a popular strategy. Many investors use it to offset income from high tax brackets. The tax deductions from negative gearing can be significant. Investors can claim expenses such as interest on loans, property management fees, and maintenance costs. These deductions can make costly properties more affordable. However, negative gearing is a contentious topic. Critics argue it inflates property prices, reducing housing affordability. As a result, there’s an ongoing debate about its role in the current housing crisis. In practice, negative gearing strategies vary. Some investors choose high-growth locations with higher potential losses, banking on long-term capital gains. Others focus on cash flow-positive properties, integrating negative gearing selectively. These real-life scenarios highlight its diverse applications. Exploring Stage 3 Tax Cuts in Australia Stage 3 tax cuts in Australia are scheduled to commence in the near future. These cuts aim to simplify the tax system by reducing the number of tax brackets. The top marginal tax rate will decrease, providing more Australians with a lower, uniform tax percentage. The Stage 3 tax cuts will noticeably affect personal income tax rates and the amount of money people have to spend. With reduced taxation on higher income, more funds will be available for consumption and investment. This is particularly beneficial for property investors looking to reallocate funds. By easing the tax burden, these cuts have the potential to boost economic growth. Increased disposable income may result in higher consumer spending, which could invigorate multiple sectors, including housing. As property demand rises, so might property values, impacting investment returns. For investors, these cuts could necessitate a rethink of strategies. Tax cuts often make other investments more appealing, prompting property investors to diversify portfolios. Additionally, the changes might modify risk assessments and willingness to invest in properties with negative gearing. However, the future of Stage 3 tax cuts holds uncertainty. Shifting political climates and economic variables can influence policies, thereby affecting their longevity and extent. Investors must stay updated and adapt strategies accordingly to navigate these potential changes. Comparing the Benefits: Negative Gearing vs. Stage 3 Tax Cuts Understanding the financial benefits of negative gearing versus Stage 3 tax cuts requires examining both short-term and long-term perspectives. In the short run, negative gearing offers immediate tax deductions on losses, reducing taxable income. Over time, however, Stage 3 tax cuts promise broader savings through reduced marginal tax rates, affecting overall financial positioning. Capital gains tax plays a significant role in property investments. For negatively geared properties, capital gains tax can offset long-term gains, impacting net returns. Stage 3 tax cuts, by lessening income tax burdens, indirectly allow for more strategic planning around capital gains. Investors’ marginal tax rate significantly affects the choice between negative gearing and tax cuts. Investors in higher tax brackets can achieve considerable tax savings through negative gearing. Conversely, Stage 3 tax cuts aim to flatten tax burdens, potentially leveling the playing field for lower and middle-income investors. Evaluating risks and rewards is crucial for financial planning. Negative gearing often results in short-term cash flow challenges yet offers potential for long-term portfolio growth. Meanwhile, tax cuts may boost immediate cash flow, influencing the balance of portfolio diversification and risk-taking. Current market conditions also affect these strategies. In high-demand property markets, negative gearing might offer advantageous returns due to property appreciation. In contrast, Stage 3 tax cuts could encourage broader economic participation, shifting the investment focus from solely property to include other asset classes. Navigating these complex decisions often requires professional advice. Financial advisors can provide guidance tailored to specific tax circumstances and investment goals. They help investors weigh the benefits and drawbacks of each strategy, ensuring financial plans align with individual needs and market realities. Financial Planning and Tax Considerations for Property Investors Understanding marginal tax rates is fundamental for investors utilizing negative gearing or considering Stage 3 tax cuts. Marginal tax rates determine how much tax is paid on additional income, influencing the effectiveness of tax strategies. Tax deductions can further enhance these strategies, reducing the overall taxable income. Capital gains tax significantly impacts property investment decisions. When selling a property, understanding potential capital gains tax is crucial in evaluating investment profitability. Ensuring an informed approach to timing sales can mitigate tax liabilities, enhancing net returns. Interest rates play a pivotal role in the cost of borrowing for property investments. Lower rates can increase the appeal of negative gearing by reducing borrowing costs and boosting potential returns. Monitoring fluctuations helps investors adapt strategies to maximize profit. A structured investment plan is vital for aligning property investments with financial goals. This plan should consider both short-term cash flow and long-term capital growth strategies. Including tax considerations ensures a holistic approach to investment planning. Effective record-keeping and documentation are essential for property investors using tax strategies. Detailed records ensure accuracy in tax filings and the ability to